India Macro Daily(Beta Mode)

Rupee Rises as Oil Slump Offsets Trade Gap

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,989.15 | +0.57% |

| Sensex | 76,808.48 | +0.71% |

| USD/INR | 94.74 | -0.39% |

| EUR/INR | 109.71 | -0.21% |

| Reliance | 1,328.80 | +1.67% |

| HDFC Bank | 784.90 | +0.97% |

| Brent Crude | 79.39 | -4.54% |

| Gold | 4,359.60 | +0.73% |

| Bitcoin | 65,512.91 | -1.17% |

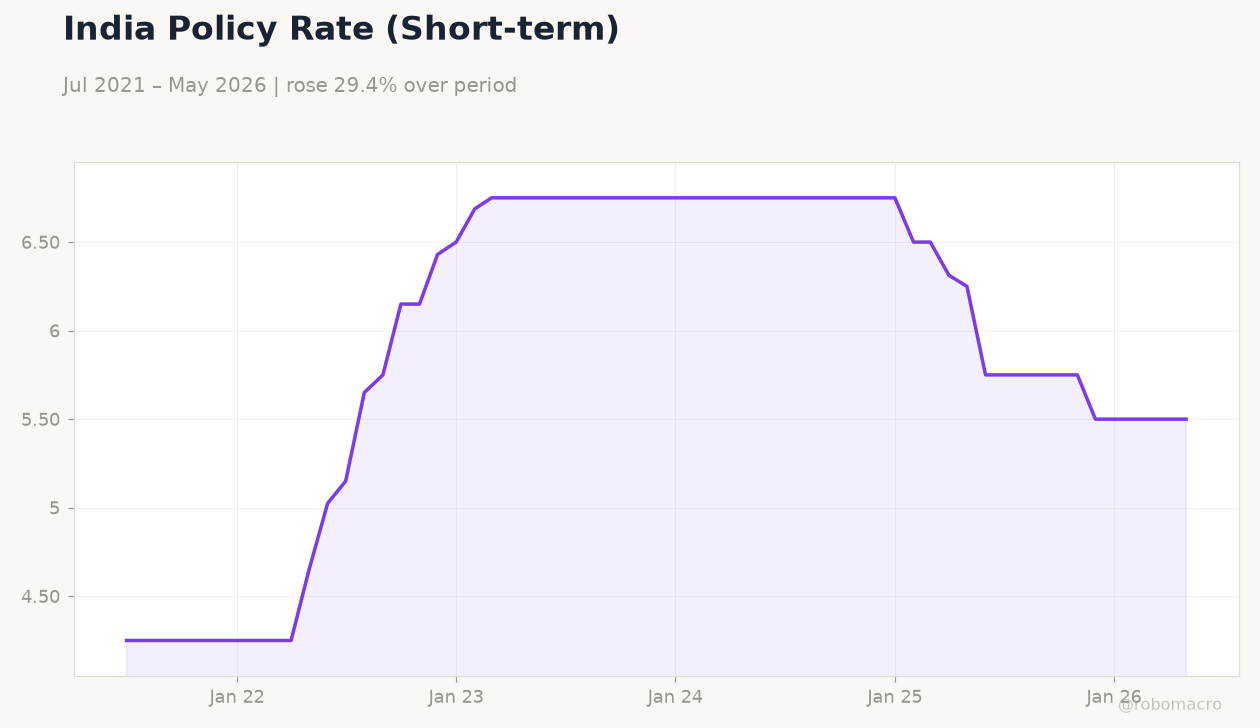

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | -28,380m | -27,000m | -28,210m |

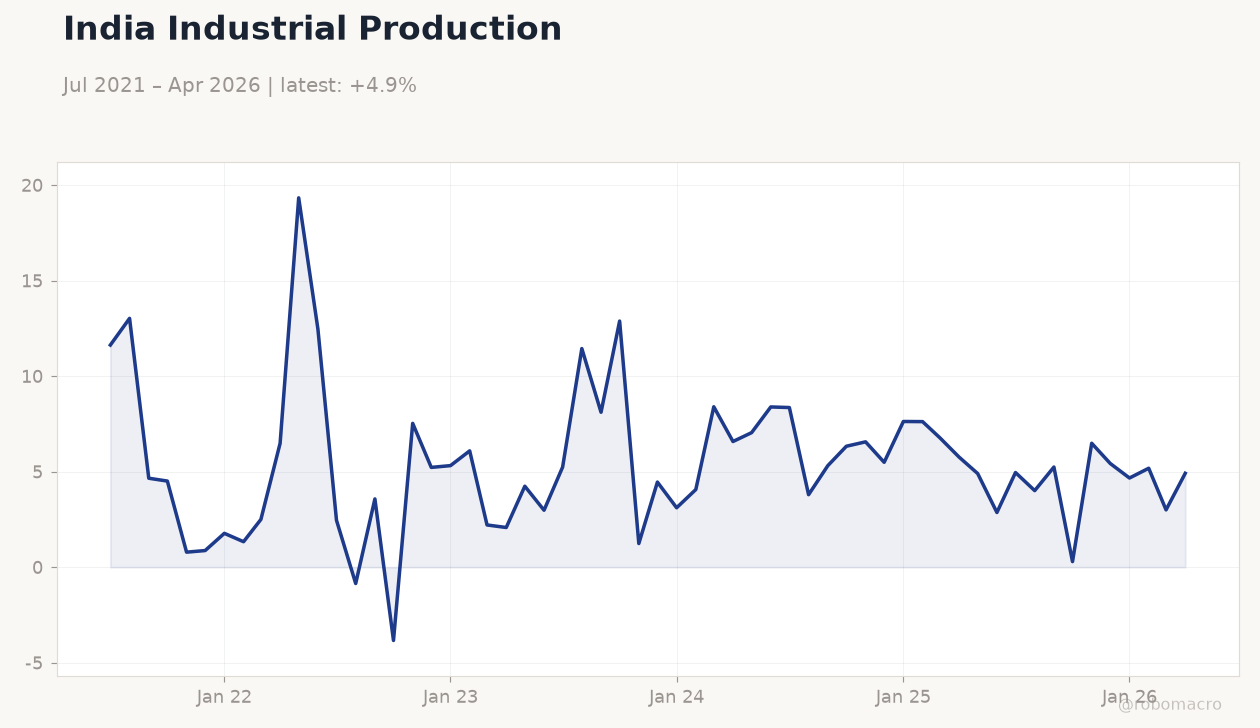

India Industrial Production | Type: macro_line | Industrial Production YoY %: 4.916 (2026-04-01) | Range: -3.835–19.33 | Trend(6pt): 11.63,3.575,1.239,7.628,3.003,4.916

India Industrial Production | Type: macro_line | Industrial Production YoY %: 4.916 (2026-04-01) | Range: -3.835–19.33 | Trend(6pt): 11.63,3.575,1.239,7.628,3.003,4.916

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-19) | |||

| Monetary Policy Meeting Minutes | - | - | 03:30 |

- Trade balance printed at -$28.21 bn in May, slightly wider than consensus but supported by services-led current account surplus of $4.7 bn in April.

- Nifty 50 rose 0.57% to 23,989.15 and Sensex gained 0.71% while USD/INR fell 0.39% to 94.74 on Brent crude’s 4.54% drop.

- RBI kept repo rate at 5.50% and expanded FCNR(B) and swap facilities to attract up to ₹6.2 lakh crore in inflows.

Yesterday's Recap

India’s May trade balance came in at -$28.21 bn versus consensus of -$27.0 bn, reflecting steady import demand despite softer oil prices. Equity benchmarks advanced with Nifty 50 closing at 23,989.15 (+0.57%) and Sensex at 76,808.48 (+0.71%), led by Reliance Industries (+1.67%) and HDFC Bank (+0.97%). The rupee strengthened to 94.74 against the dollar as Brent crude fell sharply to $79.39/bbl.

Gold rose 0.73% to 4,359.60 while short-term rates stayed anchored at 5.50%. News of a $4.7 bn April current account surplus and RBI’s fresh FCNR(B) measures reinforced positive sentiment toward the currency. Foreign investor flows showed tentative signs of return, capping USD/INR upside.

The Day Ahead

Markets await the RBI’s Monetary Policy Meeting Minutes due 19 June at 03:30 ET for fresh signals on liquidity operations and rupee support. No major data releases are scheduled for 16-17 June, leaving focus on global oil supply developments and any follow-up comments from RBI officials. Traders will monitor UPI expansion news and progress on rupee-settlement talks with Sri Lanka for any incremental capital-flow implications.

Other Economic Notes

The government formed an expert panel to modernise labour market statistics, aiming to improve data reliability for policy calibration. India and Sri Lanka advanced rupee-denominated trade settlement mechanisms targeting $6 bn in annual bilateral flows, reducing dollar dependence. Sitharaman highlighted risks from tariff shocks and crude import reliance while noting that RBI liquidity tools could lift FY27 balance-of-payments despite a modest current account deficit.

Monsoon progress remains slightly above average, supporting rural consumption expectations.

Global Macro News

Oil prices plunged after reports of a US-Iran peace deal brokered by Pakistan, with a signing ceremony slated for 19 June. Lower crude directly benefits India’s import bill and inflation trajectory. Global equity sentiment improved on the de-escalation, supporting risk assets including Indian benchmarks.

<i>↓ p.2</i>