India Macro Daily(Beta Mode)

RBI Eases NRI Deposit Rules to Attract Flows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,989.15 | +0.57% |

| Sensex | 76,808.48 | +0.71% |

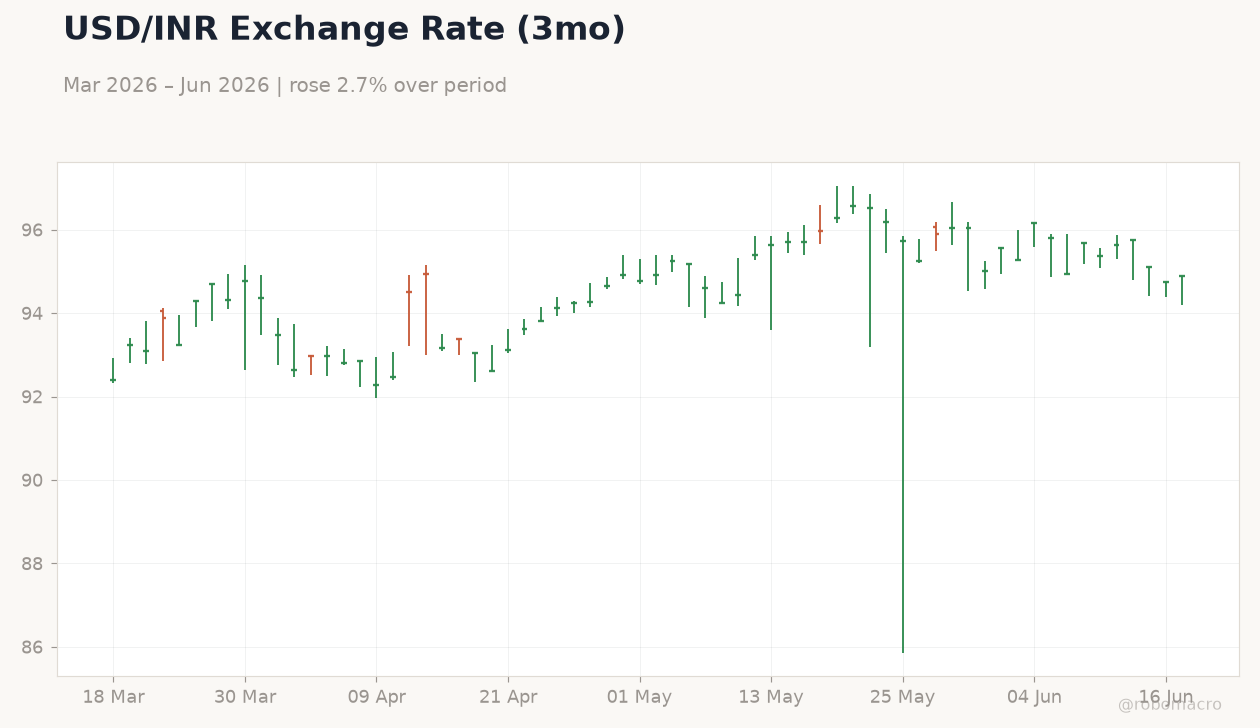

| USD/INR | 94.89 | +0.16% |

| EUR/INR | 109.74 | +0.02% |

| Reliance | 1,332.70 | +0.29% |

| HDFC Bank | 787.10 | +0.28% |

| Brent Crude | 78.81 | -0.19% |

| Gold | 4,315.90 | -0.35% |

| Bitcoin | 64,538.59 | -1.62% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | -28,380m | -27,000m | -28,210m |

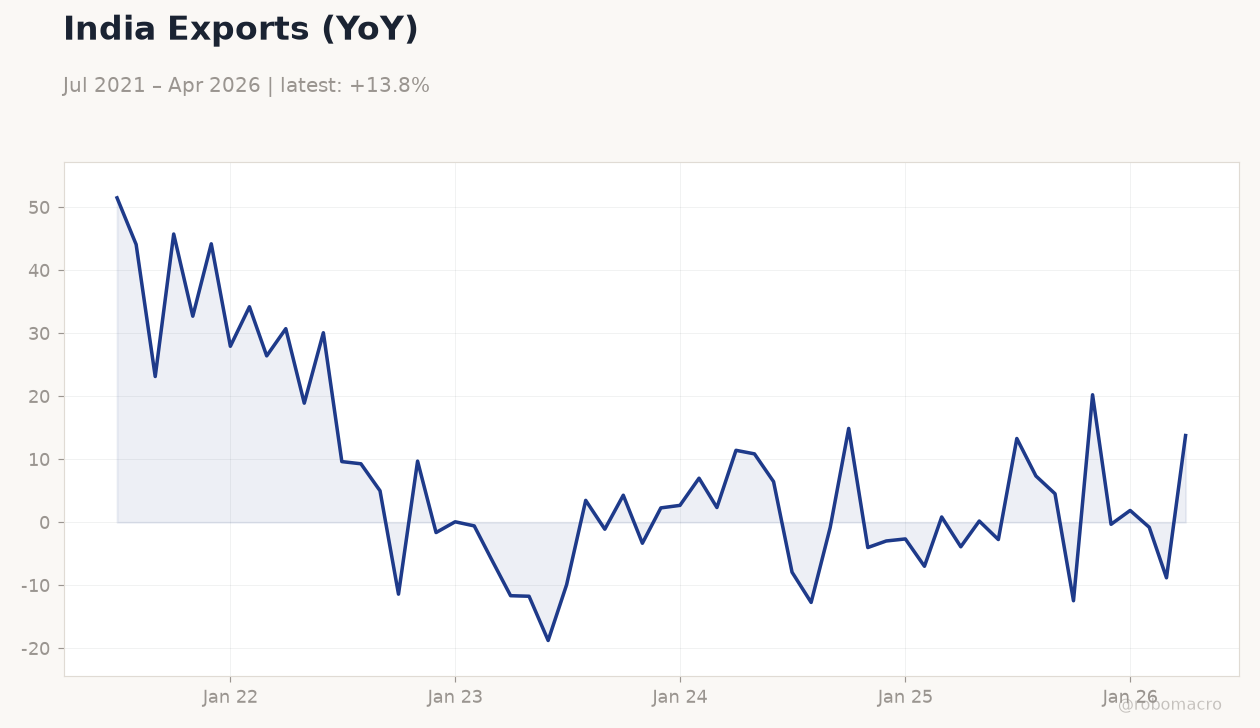

India Exports (YoY) | Type: macro_line | Exports (YoY %): 13.77 (2026-04-01) | Range: -18.76–51.49 | Trend(6pt): 51.49,5.001,-3.326,-2.644,-8.812,13.77

India Exports (YoY) | Type: macro_line | Exports (YoY %): 13.77 (2026-04-01) | Range: -18.76–51.49 | Trend(6pt): 51.49,5.001,-3.326,-2.644,-8.812,13.77

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-19) | |||

| Monetary Policy Meeting Minutes | - | - | 03:30 |

- Trade balance printed at -28.21 billion dollars, wider than the -27 billion consensus

- Nifty rose 0.57 percent to 23,989 while Sensex gained 0.71 percent

- RBI removed interest rate ceilings on select NRI deposits to support rupee

Yesterday's Recap

India's May trade balance came in at -28.21 billion dollars, wider than the -27 billion consensus though narrower than the prior -28.38 billion print. Equity markets advanced with Nifty 50 closing at 23,989.15 and Sensex at 76,808.48 as foreign investor flows showed tentative signs of return. USD/INR edged 0.16 percent higher to 94.89 while EUR/INR held nearly flat at 109.74.

Brent crude slipped 0.19 percent to 78.81 dollars per barrel, easing imported inflation risks. Gold declined 0.35 percent amid softer global prices. Short-term rates stayed anchored at 5.50 percent with no change in the policy corridor.

News flow centered on RBI steps to mobilize foreign currency deposits from non-resident Indians.

The Day Ahead

Markets will focus on the release of the latest Monetary Policy Committee meeting minutes scheduled for Friday at 03:30 ET. No major data prints are due today, leaving room for follow-through on yesterday's RBI regulatory changes. Traders will monitor any commentary on liquidity management and foreign exchange reserve deployment.

Equity sentiment may hinge on continued foreign institutional investor buying after recent RBI measures. Bond markets are expected to stay range-bound ahead of the minutes.

Other Economic Notes

Remittance inflows remained resilient despite regional tensions in West Asia, providing steady current account support. Forex reserves stand near 700 billion dollars, offering a substantial buffer against external shocks. India and Sri Lanka advanced talks on local-currency trade settlement to reduce dollar dependence.

Goldman Sachs estimates the RBI's recent actions could attract up to 60 billion dollars in inflows and restore balance-of-payments surplus. These steps align with efforts to stabilize the rupee without direct intervention.

Global Macro News

A potential US-Iran agreement points to lower oil prices, which would cut India's import bill and support the current account. <i>↓ p.2</i>