India Macro Daily(Beta Mode)

Rupee Weakens Ahead of India PMI Prints

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,013.10 | -0.64% |

| Sensex | 76,802.90 | -0.78% |

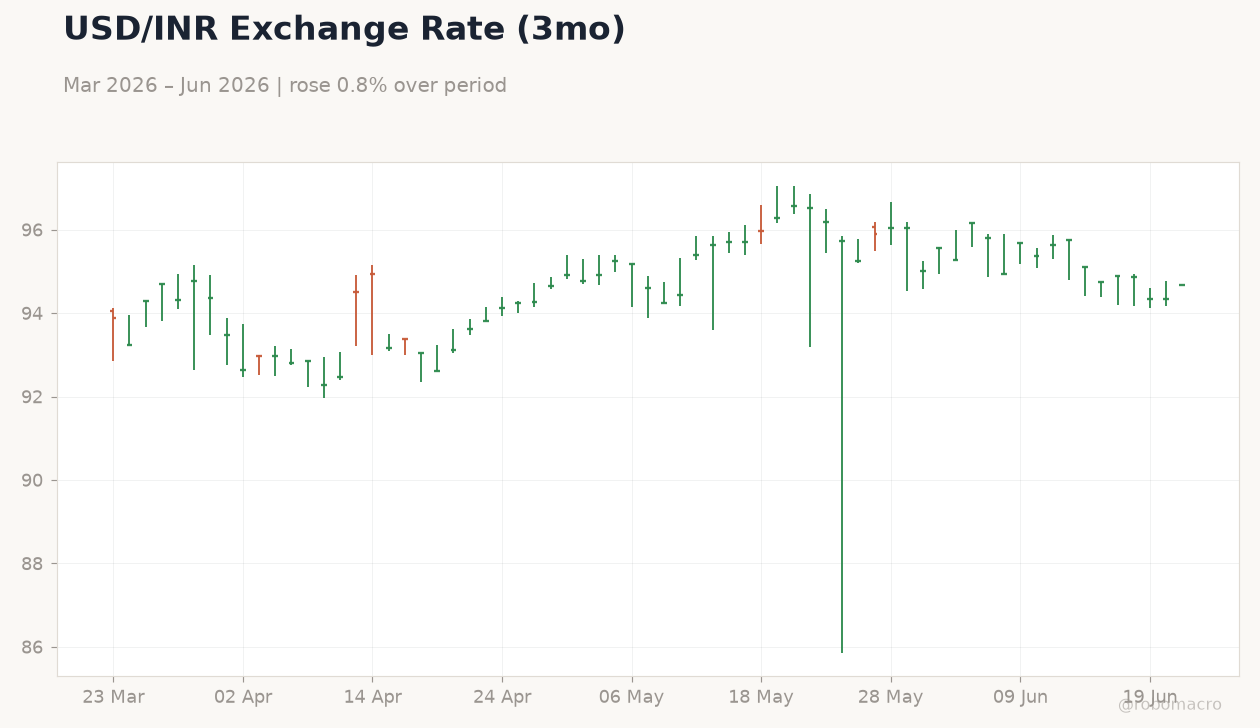

| USD/INR | 94.67 | +0.36% |

| EUR/INR | 108.17 | +3.22% |

| Reliance | 1,329.10 | +0.08% |

| HDFC Bank | 780.65 | -2.30% |

| Brent Crude | 78.09 | -2.20% |

| Gold | 4,199.80 | -0.58% |

| Bitcoin | 63,795.19 | +0.88% |

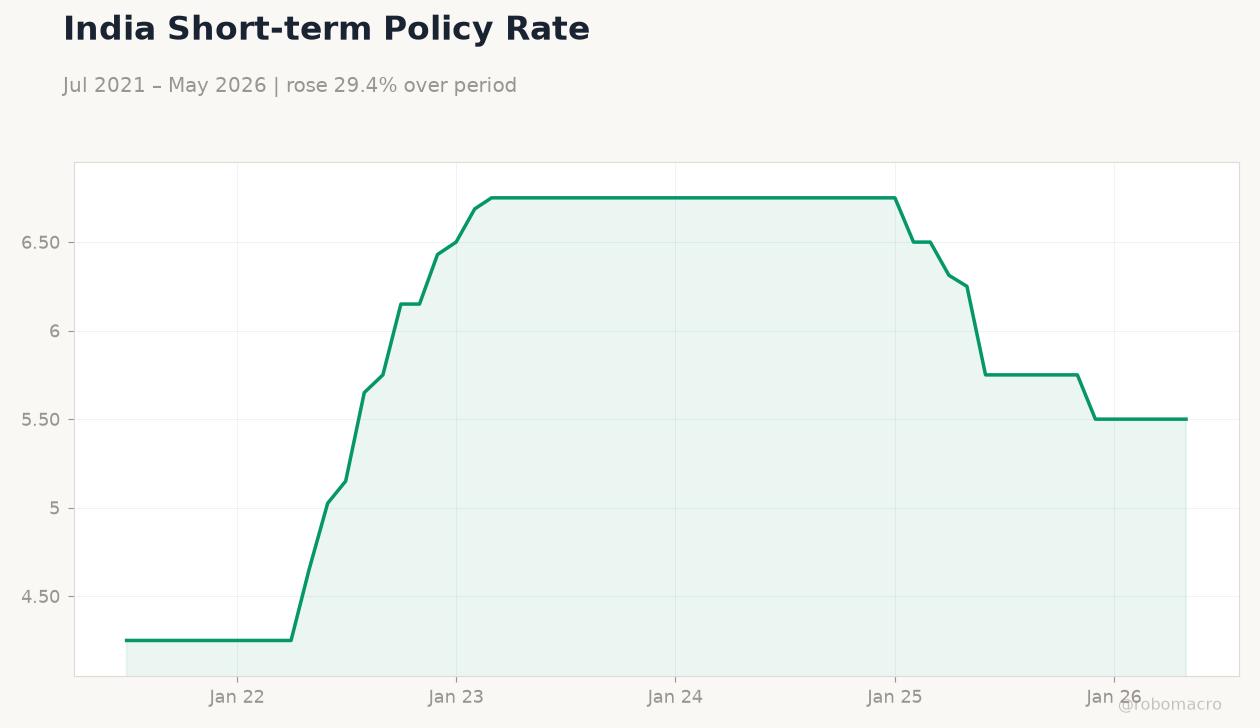

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

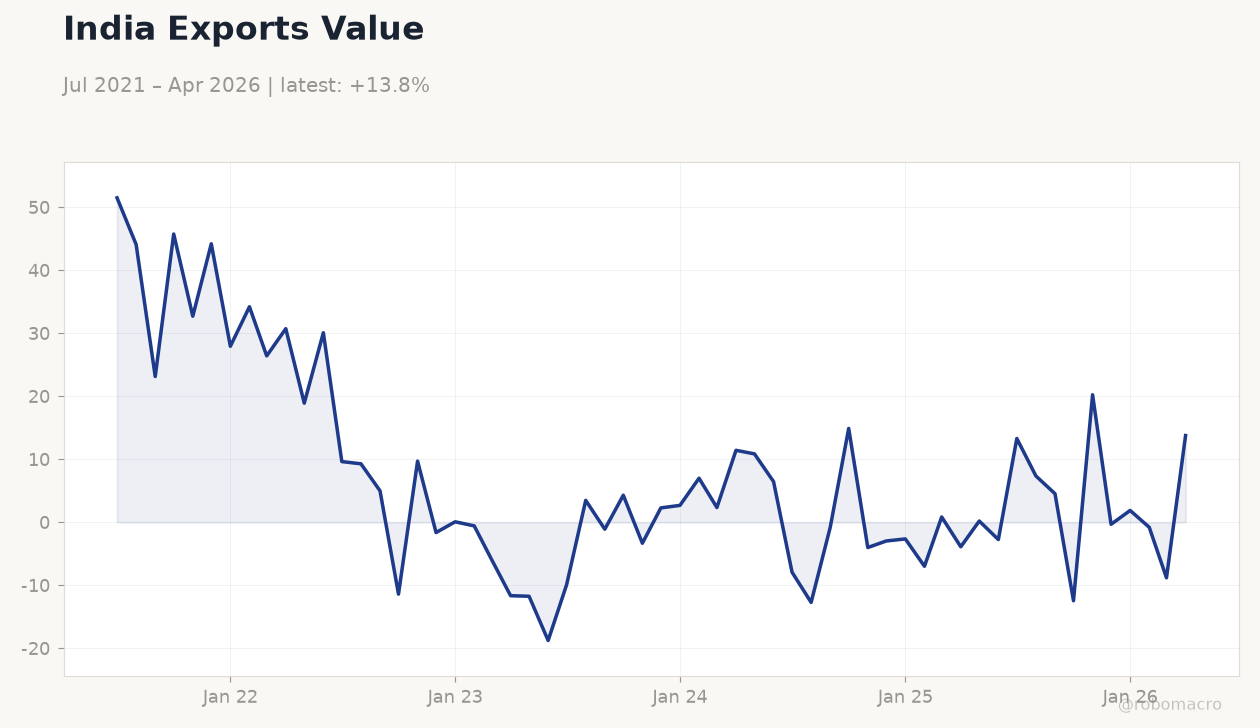

India Exports Value | Type: macro_line | USD mn: 13.77 (2026-04-01) | Range: -18.76–51.49 | Trend(6pt): 51.49,5.001,-3.326,-2.644,-8.812,13.77

India Exports Value | Type: macro_line | USD mn: 13.77 (2026-04-01) | Range: -18.76–51.49 | Trend(6pt): 51.49,5.001,-3.326,-2.644,-8.812,13.77

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-23) | |||

| HSBC Composite PMI Flash | 59.30 | - | 21:00 |

| HSBC Manufacturing PMI Flash | 55 | - | 21:00 |

| HSBC Services PMI Flash | 59.80 | - | 21:00 |

- Nifty 50 slips 0.64% to 24,013.10 as IT stocks weigh on sentiment

- USD/INR climbs 0.36% to 94.67 after RBI netsells $8.9bn forex in April

- HSBC Manufacturing and Services PMI flashes due at 21:00 ET tonight

Yesterday's Recap

Indian equities closed lower with Nifty 50 at 24,013.10, down 0.64%, and Sensex at 76,802.90, down 0.78%. The rupee depreciated to 94.67 against the dollar amid a hawkish Fed outlook that lifted the greenback. RBI data showed net sales of $8.94 billion in the spot forex market during April to ease rupee pressure.

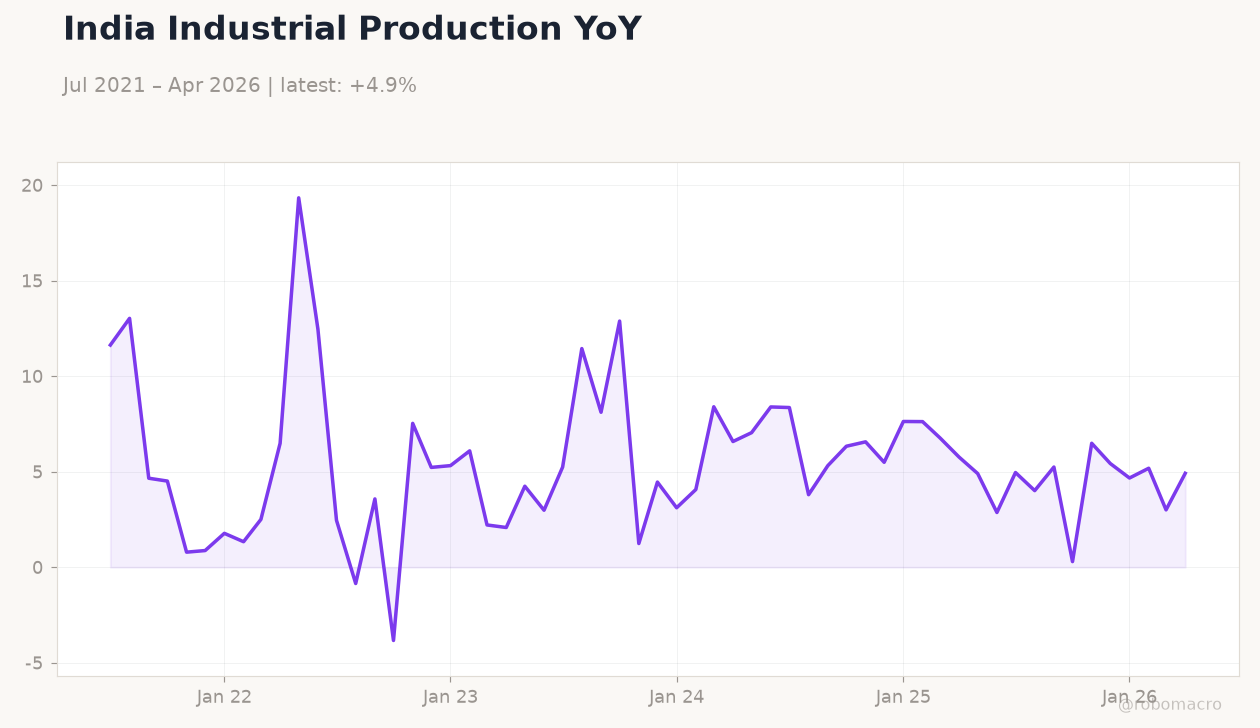

The 10-year bond yield remained steady at 6.86% as foreign inflows reached $2.68 billion following tax relief measures. Core sector output growth hit a seven-month low in May, pointing to weaker industrial production ahead. Three Indian-flagged oil tankers safely transited the Strait of Hormuz carrying over 860,000 metric tons.

Short-term rates held at 5.50% with no change in the RBI repo rate.

The Day Ahead

Markets will focus on the HSBC Composite, Manufacturing and Services PMI flashes scheduled for release at 21:00 ET. These prints will provide the first read on June activity after May’s soft core sector data. No RBI speeches or policy announcements are listed.

Traders will also monitor weekly forex reserve figures and any updates on US-India trade talks. A softer-than-expected PMI outcome could reinforce expectations for steady policy rates through the summer. Brent crude at $78.09 will remain a key watch item given its impact on inflation.

Other Economic Notes

Tax relief and RBI liquidity steps have drawn $2.68 billion into Indian debt markets in recent weeks. Strong fundamentals allowed India to navigate West Asia tensions without major disruption, according to RBI commentary. MSME lending continues to receive targeted support from the central bank to sustain credit flow.

Southwest monsoon progress supports rural demand while FDI inflows rose 12% year-on-year in April-May. Core sector weakness in May signals downside risk to May industrial production prints.

Global Macro News

The Fed’s hawkish tone lifted the dollar and pressured emerging-market currencies including the rupee. Brent crude fell 2.20% to $78.09 on expectations of higher OPEC+ supply. Gold eased 0.58% to 4,199.80 amid reduced safe-haven demand after Hormuz transit news.

Three Indian tankers cleared the strait without incident, easing immediate supply concerns. <i>↓ p.2</i>