India Macro Daily(Beta Mode)

India PMI Eases as Equities Hold Gains

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,102.90 | +0.37% |

| Sensex | 77,094.07 | +0.38% |

| USD/INR | 94.72 | +0.03% |

| EUR/INR | 107.81 | -0.28% |

| Reliance | 1,329.10 | +0.08% |

| HDFC Bank | 780.65 | -2.30% |

| Brent Crude | 76.66 | -1.59% |

| Gold | 4,114.50 | -1.61% |

| Bitcoin | 62,942.00 | -1.58% |

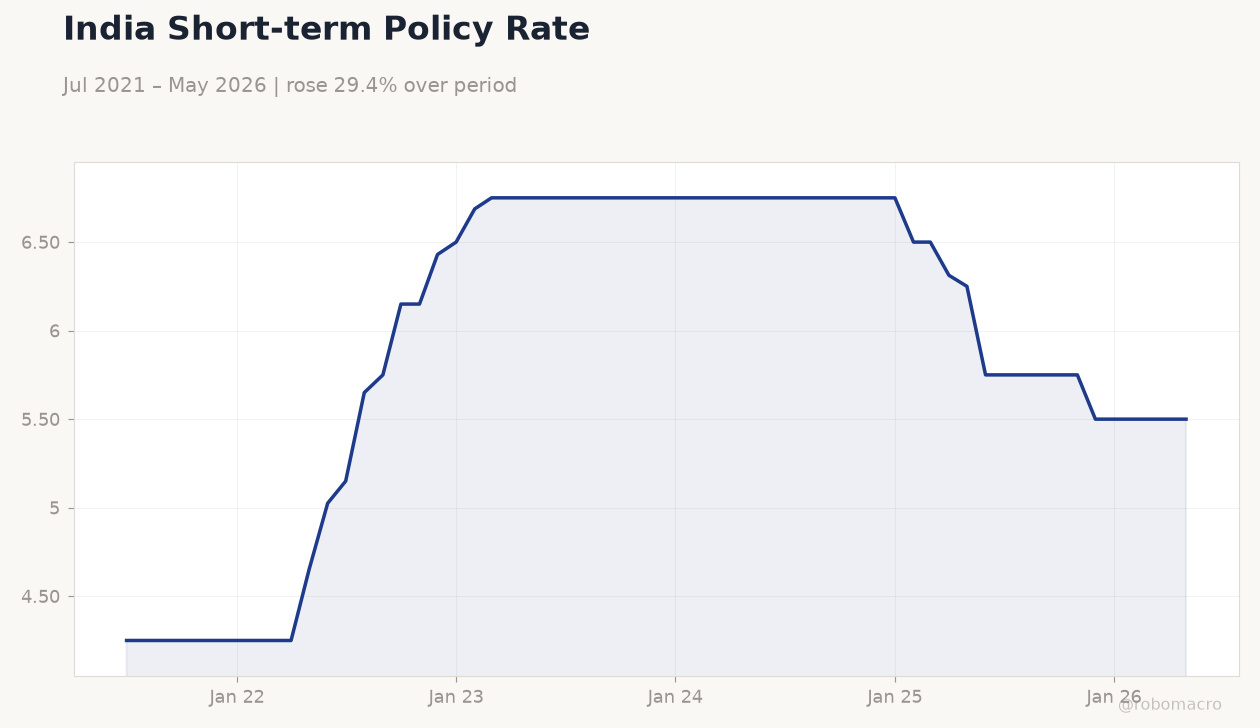

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| HSBC Composite PMI Flash | 59.30 | - | 57.40 |

| HSBC Manufacturing PMI Flash | 55 | - | 54.50 |

| HSBC Services PMI Flash | 59.80 | - | 57.30 |

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- HSBC Manufacturing PMI slips to 54.5 from 55.0 in June flash

- Nifty 50 rises 0.37% to 24,102.90 while Sensex gains 0.38%

- RBI repo rate remains at 5.50% with liquidity support ongoing

Yesterday's Recap

India's HSBC Manufacturing PMI eased to 54.5 in the June flash from 55.0 previously, while the Services PMI declined to 57.3 from 59.8 and the Composite PMI fell to 57.4 from 59.3. The moderation signals a slight cooling in private-sector momentum after strong prior readings. Nifty 50 advanced 0.37% to close at 24,102.90 and Sensex gained 0.38% to 77,094.07, supported by selective buying in IT names.

USD/INR edged 0.03% higher to 94.72 amid steady RBI intervention, while Brent crude dropped 1.59% to 76.66. HDFC Bank shares fell 2.30% to 780.65, offsetting modest gains elsewhere. Foreign inflows into debt reached $2.68 billion on tax relief and RBI liquidity measures.

The Day Ahead

No major Indian data releases are scheduled for today or tomorrow according to the calendar. Market focus will remain on global oil price trends and any updates on US-India trade talks. The 10-year G-Sec yield is expected to hold near 6.86% as inflows continue.

Equity participants will monitor FII flows and IT sector positioning after recent contrarian bets by large domestic funds. RBI liquidity operations will stay in view following the recent ₹1.41 lakh crore infusion.

Other Economic Notes

Core sector growth hit a seven-month low in May as external disruptions weighed on output. Weak monsoon progress raises risks to food prices and kharif sowing despite otherwise solid fundamentals. LPG imports from the US are on track for a record 1 million metric tons in June.

FDI equity inflows reached $7.1 billion in April-May, with IT and services capturing nearly one-third. The rupee faces ongoing pressure from RBI net forex sales of $8.9 billion in April.

Global Macro News

Brent crude declined 1.59% to 76.66 on softer demand signals from China. Gold fell 1.61% to 4,114.50 as risk appetite improved modestly. Bitcoin traded 1.58% lower at 62,942.00.

US trade officials are scheduled to visit India for interim deal discussions aimed at improving market access. Fed rate hike expectations continue to support the dollar and weigh on emerging-market currencies including the rupee. Global equity sell-offs have limited spillover into Indian benchmarks so far.

<i>↓ p.2</i>