India Macro Daily(Beta Mode)

India PMI Eases as Rupee Weakens to 95.18

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,021.65 | +0.83% |

| Sensex | 76,991.22 | +1.04% |

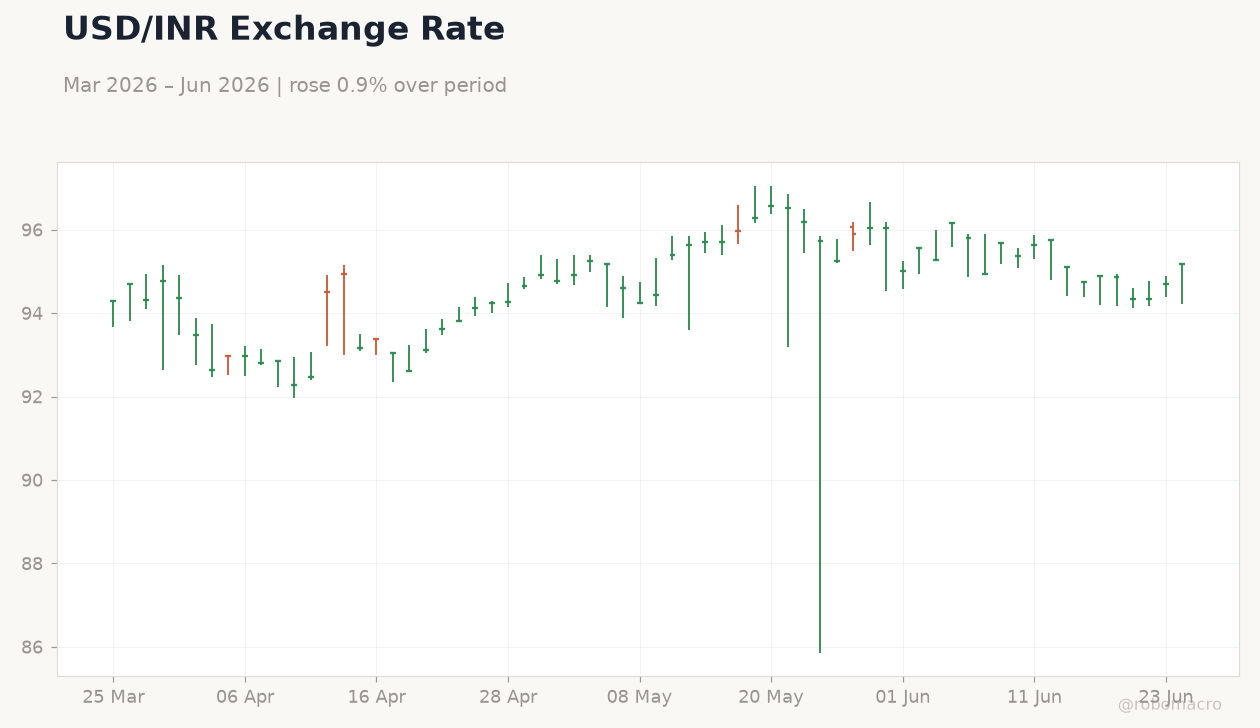

| USD/INR | 95.18 | +0.51% |

| EUR/INR | 107.73 | -0.36% |

| Reliance | 1,313.60 | +0.31% |

| HDFC Bank | 793.20 | +2.39% |

| Brent Crude | 72.33 | -6.16% |

| Gold | 4,002.70 | -3.08% |

| Bitcoin | 60,809.96 | -2.96% |

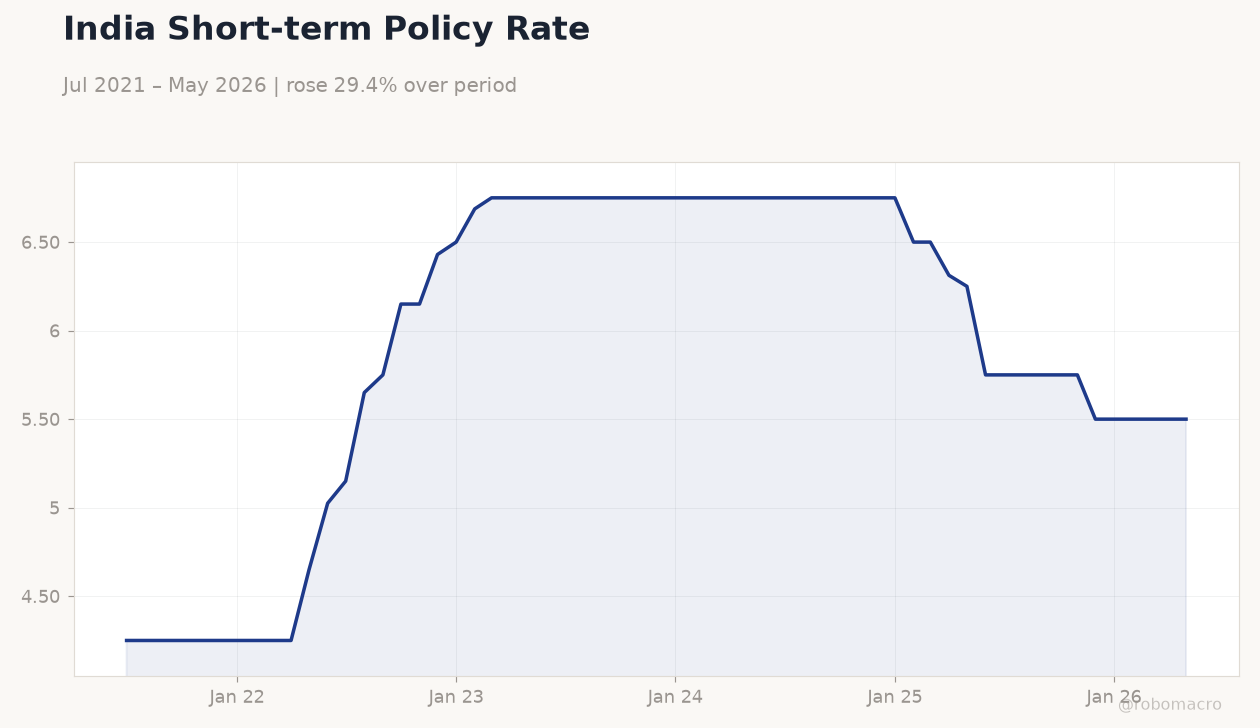

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| HSBC Composite PMI Flash | 59.30 | - | 57.40 |

| HSBC Manufacturing PMI Flash | 55 | - | 54.50 |

| HSBC Services PMI Flash | 59.80 | - | 57.30 |

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- HSBC Services PMI fell to 57.3 from 59.8, marking the steepest drop in three months

- Nifty 50 rose 0.83% to 24,021.65 while Sensex gained 1.04% to 76,991.22

- USD/INR climbed 0.51% to 95.18 as Brent crude plunged 6.16% to 72.33

Yesterday's Recap

HSBC Composite PMI Flash dropped to 57.4 from 59.3 while Manufacturing PMI eased to 54.5 from 55.0, confirming a broad-based moderation in private-sector activity. Equity markets advanced with Nifty and Sensex posting solid gains led by bank and IT names. The rupee weakened to 95.18 against the dollar despite RBI dollar purchases, as higher US yields supported the greenback.

Brent crude fell sharply to 72.33 on improved supply signals, easing imported inflation concerns for India. Gold declined 3.08% to 4,002.70 while Bitcoin slipped 2.96%. Short-term rates stayed at 5.50% with no change in the policy corridor.

Overall, the session reflected resilient equities offset by currency pressure.

The Day Ahead

No major Indian data releases are scheduled for 24 June, leaving markets to focus on global risk sentiment and US Fed signals. Traders will monitor rupee movements around the 95 handle amid ongoing RBI intervention. Equity flows may hinge on IT sector updates and any progress on global bond index inclusion.

Weekly forex reserve data, if released, could highlight RBI’s FX book management. Oil price stability remains key for near-term inflation and current-account outlook.

Other Economic Notes

India’s LPG imports from the US are projected to exceed 1 million metric tons in June, a record that underscores shifting energy sourcing. S&P Global lowered its India growth forecast by 110 basis points citing persistent inflation risks. The largest domestic equity fund has increased exposure to IT stocks on valuation support despite AI-related concerns.

Cabinet approvals for additional infrastructure spending continue to underpin medium-term demand. Cumulative monsoon rainfall running 7% above long-period average supports rural consumption prospects.

Global Macro News

Hawkish Fed pricing has intensified pressure on emerging-market currencies including the rupee. US rate expectations have capped oil-price relief for India despite Brent’s sharp decline. <i>↓ p.2</i>