India Macro Daily(Beta Mode)

PMIs Ease but Equities Rise on RBI Support

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,021.65 | +0.83% |

| Sensex | 76,991.22 | +1.04% |

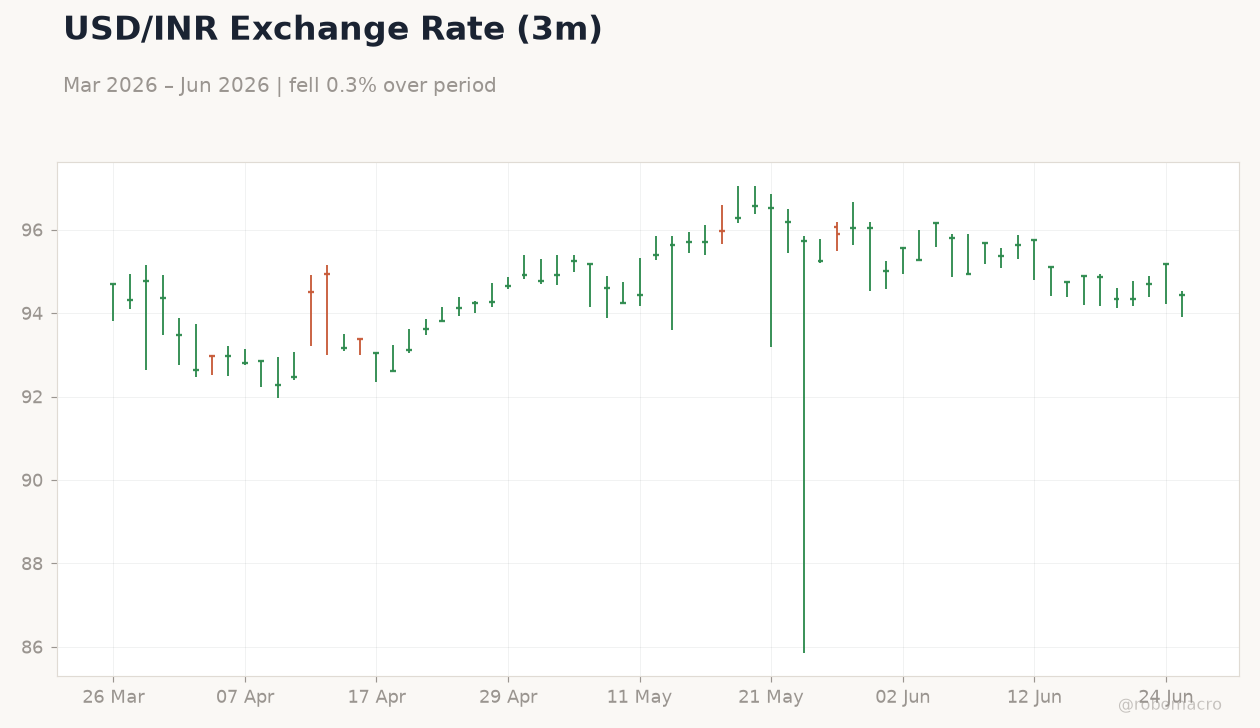

| USD/INR | 94.44 | -0.78% |

| EUR/INR | 107.40 | -0.30% |

| Reliance | 1,313.60 | +0.31% |

| HDFC Bank | 793.20 | +2.39% |

| Brent Crude | 75.23 | +2.02% |

| Gold | 4,036.10 | +1.15% |

| Bitcoin | 59,677.77 | -2.16% |

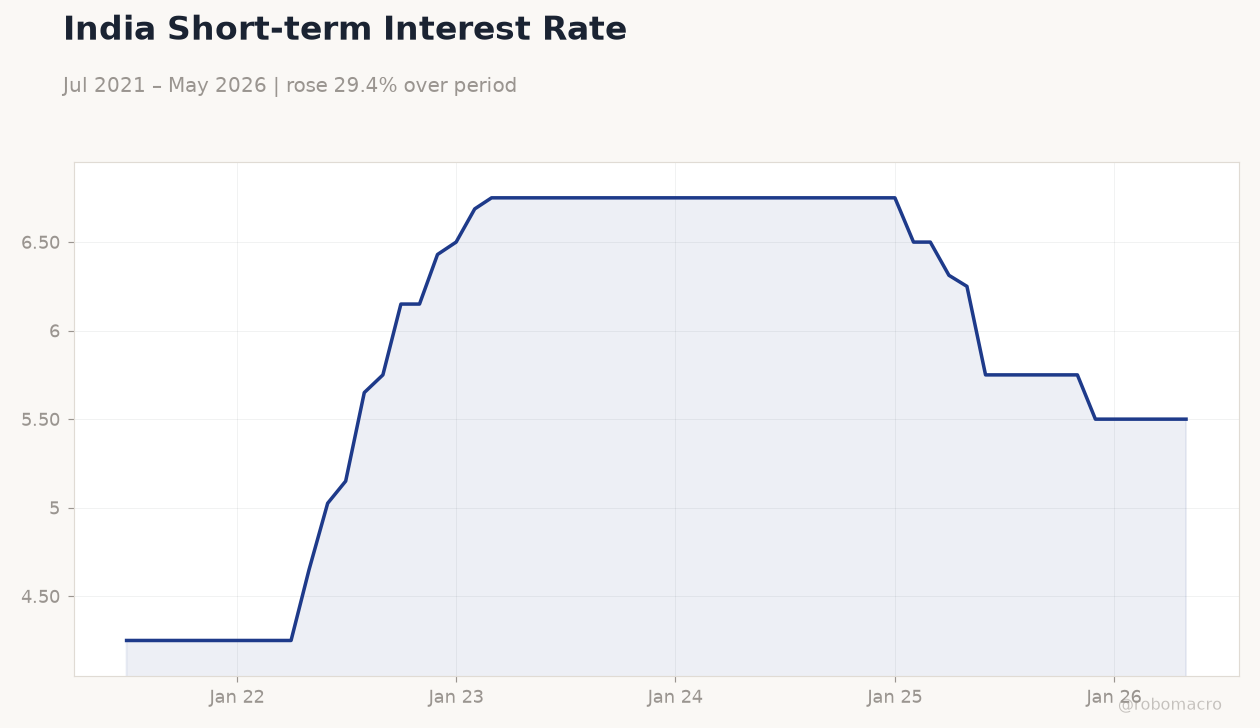

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| HSBC Composite PMI Flash | 59.30 | - | 57.40 |

| HSBC Manufacturing PMI Flash | 55 | - | 54.50 |

| HSBC Services PMI Flash | 59.80 | - | 57.30 |

India Short-term Interest Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

India Short-term Interest Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- HSBC flash PMIs fell sharply in June, with composite dropping to 57.4 from 59.3, signaling moderating momentum.

- Nifty 50 and Sensex rose 0.83% and 1.04% respectively, supported by lower oil prices and RBI liquidity measures.

- USD/INR eased 0.78% to 94.44 as markets priced limited near-term RBI tightening.

Yesterday's Recap

HSBC Composite PMI Flash printed at 57.4 versus 59.3 previously, while Manufacturing PMI eased to 54.5 from 55.0 and Services PMI declined to 57.3 from 59.8. Equity benchmarks closed higher, with Nifty 50 at 24,021.65 and Sensex at 76,991.22. The rupee strengthened notably against the dollar to 94.44.

Brent crude rose 2.02% to 75.23, while gold gained 1.15% to 4,036.10. Short-term rates held steady at 5.50%. Record SIP inflows and softer energy prices lifted sentiment across banking and IT stocks.

Reliance added 0.31% and HDFC Bank gained 2.39%. The moves occurred despite mixed global cues and ahead of any fresh policy signals.

The Day Ahead

No major data releases are scheduled for 25 June. Markets will monitor corporate tax collection prints and RBI’s weekly statistical supplement for deposit trends. Focus remains on Federal Reserve signals and any follow-through from recent RBI forex rule changes.

Equity and currency traders will watch oil price stability given its direct impact on the current account. Liquidity conditions and rupee volatility are expected to stay in focus ahead of the next policy meeting. Any surprise in tax data could shift near-term rate expectations priced by OIS markets.

Other Economic Notes

S&P Global projects FY27 GDP growth slowing to 6.6%, reflecting base effects and moderating domestic demand. Record SIP inflows continue to underpin capital market resilience according to JPMorgan. Amazon’s additional $13 billion AI commitment through 2030 highlights sustained foreign direct investment in high-value services.

Monsoon progress supports rural consumption outlook while infrastructure spending maintains double-digit growth. NRIs appear to be shifting toward dollar deposits under the revived FCNR scheme, mirroring patterns seen in 2013.

Global Macro News

The Federal Reserve’s policy path remains central for emerging-market flows, with rate talk pressuring the rupee open near 94.90. Easing geopolitical supply risks have pushed oil toward pre-conflict levels, aiding India’s terms of trade. <i>↓ p.2</i>