India Macro Daily(Beta Mode)

India Services PMI Cools in Flash Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,056.00 | +0.14% |

| Sensex | 77,100.47 | +0.14% |

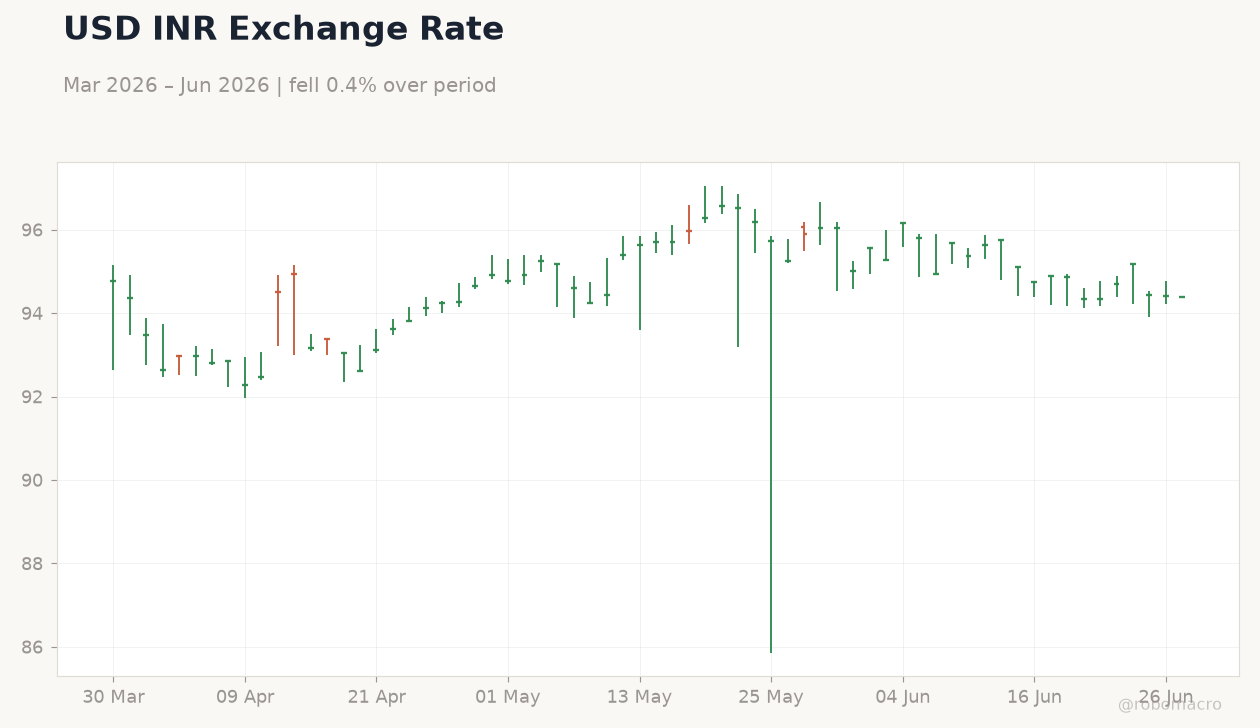

| USD/INR | 94.39 | -0.02% |

| EUR/INR | 107.49 | +0.31% |

| Reliance | 1,316.50 | +0.22% |

| HDFC Bank | 796.00 | +0.35% |

| Brent Crude | 72.80 | +1.13% |

| Gold | 4,072.40 | -0.15% |

| Bitcoin | 59,103.90 | -1.40% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| HSBC Composite PMI Flash | 59.30 | - | 57.40 |

| HSBC Manufacturing PMI Flash | 55 | - | 54.50 |

| HSBC Services PMI Flash | 59.80 | - | 57.30 |

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- HSBC Services PMI fell to 57.3 from 59.8, with composite dropping to 57.4

- Nifty 50 rose 0.14% to 24,056 while USD/INR eased 0.02% to 94.39

- Forex reserves increased $963 million to $672.59 billion

Yesterday's Recap

India’s HSBC flash PMI data showed clear moderation across sectors. Manufacturing PMI declined to 54.5 from 55.0 while services fell more sharply to 57.3. The composite index slipped to 57.4, its weakest reading in several months.

Equity markets posted modest gains, with Nifty 50 closing at 24,056 and Sensex at 77,100.47, both up 0.14%. The rupee strengthened slightly against the dollar to 94.39. Brent crude rose 1.13% to 72.80 while gold edged down 0.15%.

Short-term rates remained anchored at 5.50%.

The Day Ahead

No major data releases are scheduled for today or tomorrow. Attention will turn to weekly forex reserve updates and any follow-up commentary from RBI officials. Markets will monitor oil price movements given India’s high import dependence.

SEZ policy overhaul discussions may also draw focus after recent export weakness. Traders will watch global risk sentiment for cues on foreign portfolio flows.

Other Economic Notes

EY projects India’s FY27 growth at 6.6-6.8%, supported by lower oil prices and steady RBI policy. Oil import reliance has crossed 90%, raising energy security concerns flagged in the same report. India has lifted restrictions on commercial LPG supplies that were imposed during earlier Middle East supply disruptions.

Forex reserves reached 672.59 billion, providing a solid buffer. Deloitte notes structural gaps remain in scaling the debt market toward the 7.3 trillion target.

Global Macro News

Lower global oil prices are providing relief to India’s current account and inflation outlook. Iranian developments around the Strait of Hormuz continue to pose potential supply risks for Indian refiners. Russian investment flows into India remain active across energy and defense sectors.

Sri Lanka’s rupee depreciation of 8% against the dollar in the first half of 2026 may affect regional trade dynamics. Global food inflation risks persist, keeping pressure on India’s vegetable and cereal prices. <i>↓ p.2</i>