India Macro Daily(Beta Mode)

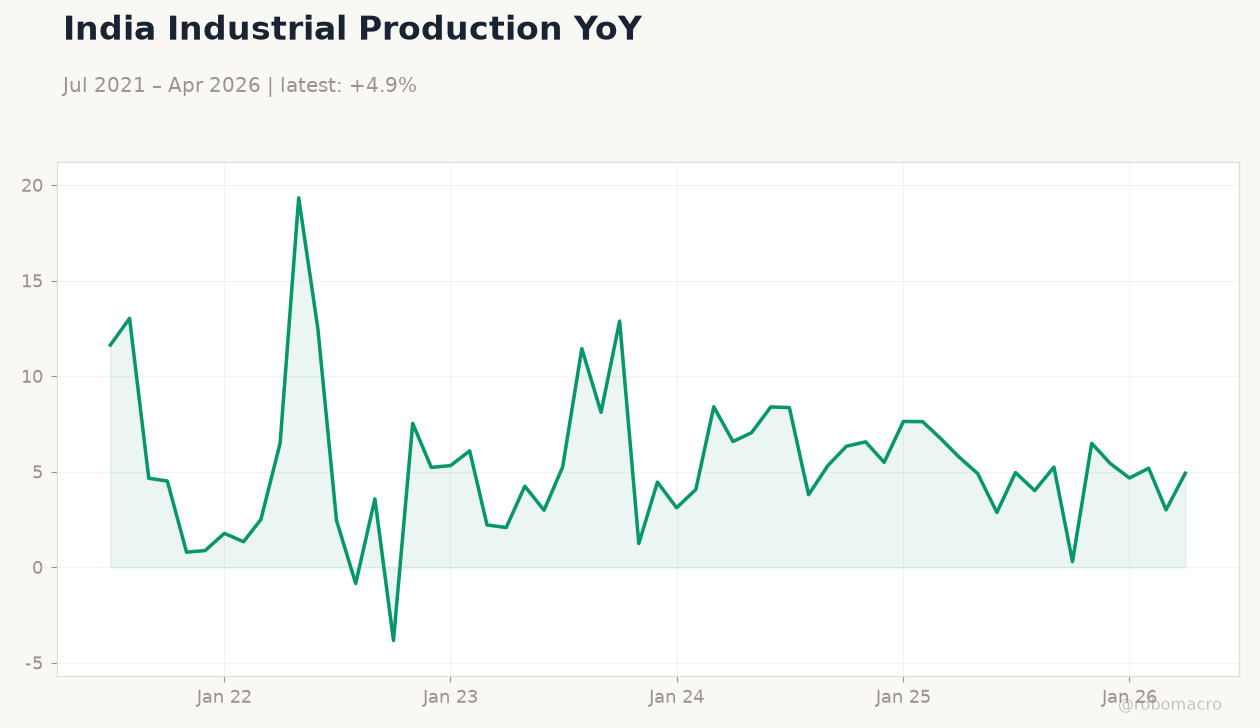

IIP Tops Ests.; External Debt Hits $762.8bn

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 23,946.25 | -0.46% |

| Sensex | 76,728.37 | -0.48% |

| USD/INR | 94.36 | -0.04% |

| EUR/INR | 107.34 | +0.17% |

| Reliance | 1,316.50 | +0.22% |

| HDFC Bank | 796.00 | +0.35% |

| Brent Crude | 73.62 | +2.26% |

| Gold | 3,975.40 | -2.53% |

| Bitcoin | 59,853.96 | +0.54% |

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Industrial Production Year-over-Year | 4.90 | 4.70 | 5.10 |

| Manufacturing Production Year-over-Year | 6.20 | - | 5.50 |

India Policy Rate | Type: macro_line | Repo Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

India Policy Rate | Type: macro_line | Repo Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,5.75,6.75,6.75,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Industrial production rose 5.1% y/y in May, above 4.7% consensus, while manufacturing output eased to 5.5%.

- Nifty 50 fell 0.46% to 23,946.25 and Sensex declined 0.48% to 76,728.37 as Brent crude climbed 2.26%.

- RBI repo rate held at 5.50%; external debt reached $762.8 billion with debt-to-GDP ratio at 20.8%.

Yesterday's Recap

May industrial production printed at 5.1% y/y, beating the 4.7% consensus and prior 4.9% reading, while manufacturing production slowed to 5.5% from 6.2%. Equity markets closed lower with Nifty 50 at 23,946.25 and Sensex at 76,728.37. USD/INR eased 0.04% to 94.36 despite Brent crude rising to 73.62.

Gold fell 2.53% to 3,975.40 and Reliance and HDFC Bank posted modest gains of 0.22% and 0.35%. No RBI policy actions occurred and short-term rates stayed at 5.50%. The print reinforced expectations that the central bank will maintain its current stance.

External debt data released by the RBI showed a rise to 762.8 billion dollars by end-March 2026, lifting the debt-to-GDP ratio to 20.8%. Markets absorbed the figures without sharp moves in bonds or the rupee.

The Day Ahead

No major Indian data releases are scheduled for today or tomorrow. Traders will monitor global oil price movements and any follow-through commentary on external debt figures released by the RBI. SEZ policy overhaul discussions and bond inflow trends may also influence sentiment.

Equity open interest and rupee volatility remain the key variables to watch. Forward guidance from any RBI officials could shift OIS pricing around the 5.50% repo rate. Normal monsoon rainfall continues to support kharif sowing expectations and broader growth forecasts for FY27.

Other Economic Notes

External debt climbed to 762.8 billion dollars by end-March 2026, lifting the debt-to-GDP ratio to 20.8%. EY projects FY27 growth at 6.6-6.8%, supported by normal monsoon rainfall and rising FDI equity inflows. Goldman Sachs highlighted preference for India 30-year bonds on improved fiscal visibility.

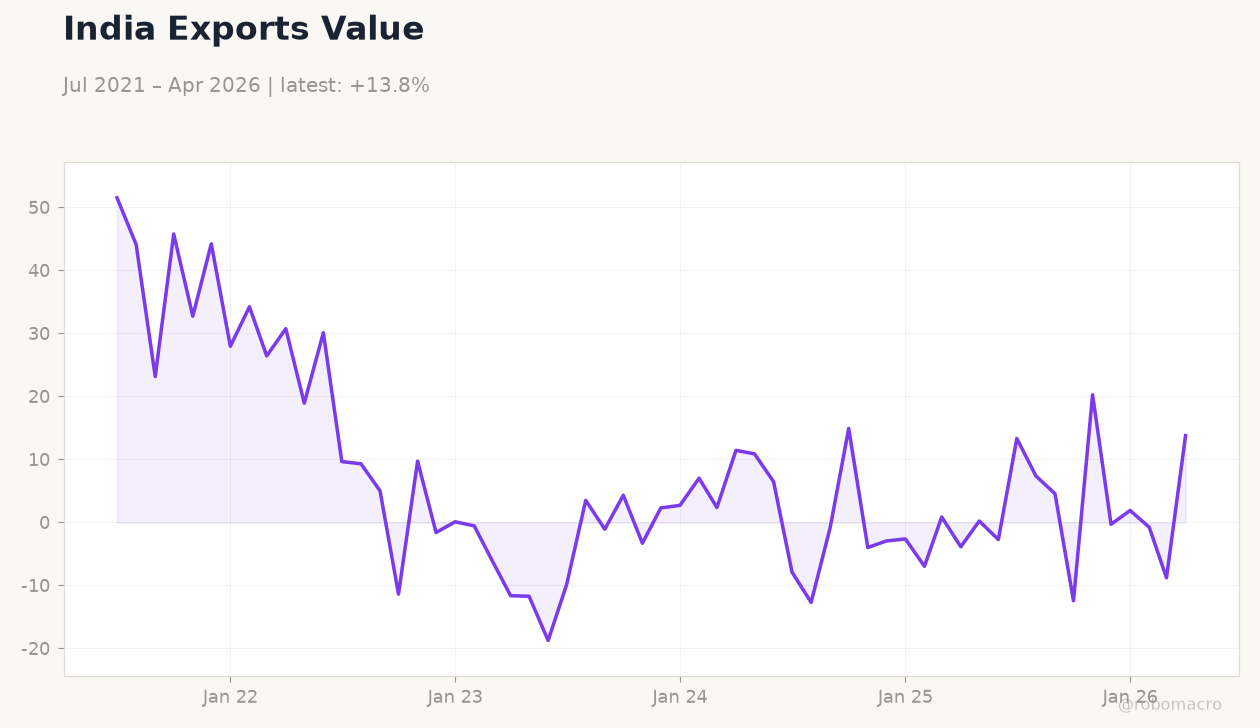

SEZ 2.0 reforms are under consideration following a decline in exports. Bond markets received 32,630 crore rupees in inflows after recent tax adjustments. Cumulative rainfall running 6% above normal has bolstered agricultural prospects and reduced downside risks to rural demand.