India Macro Daily(Beta Mode)

India IP Beats Forecasts as RBI Flags Oil Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,005.85 | +0.59% |

| Sensex | 76,922.64 | +0.58% |

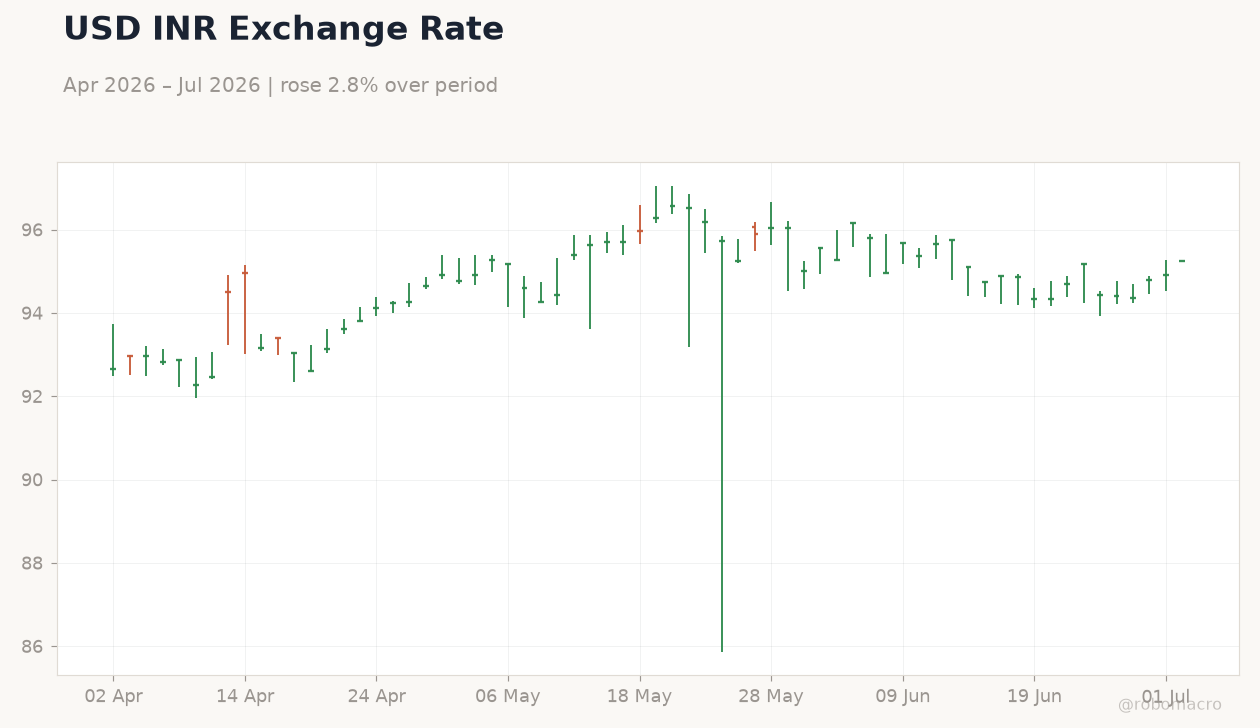

| USD/INR | 95.24 | +0.34% |

| EUR/INR | 108.42 | +0.43% |

| Reliance | 1,305.60 | +0.90% |

| HDFC Bank | 795.50 | -0.31% |

| Brent Crude | 70.84 | -2.85% |

| Gold | 4,068.20 | +1.13% |

| Bitcoin | 60,388.51 | +3.12% |

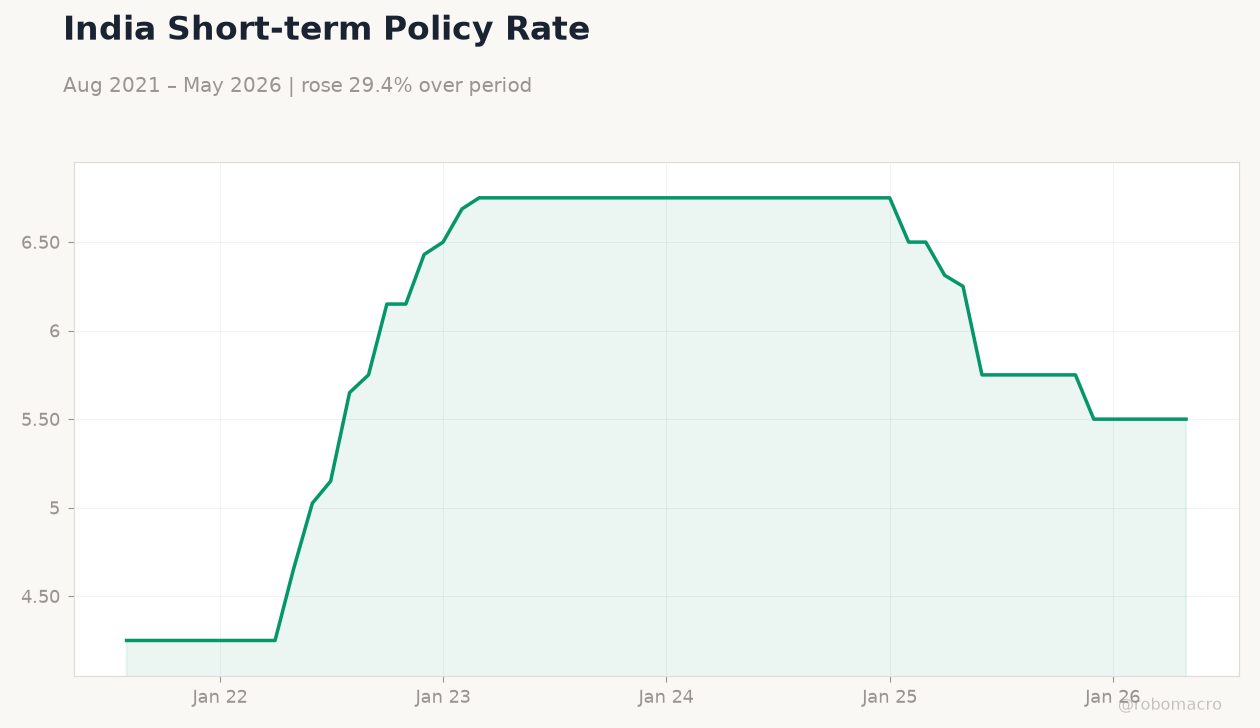

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

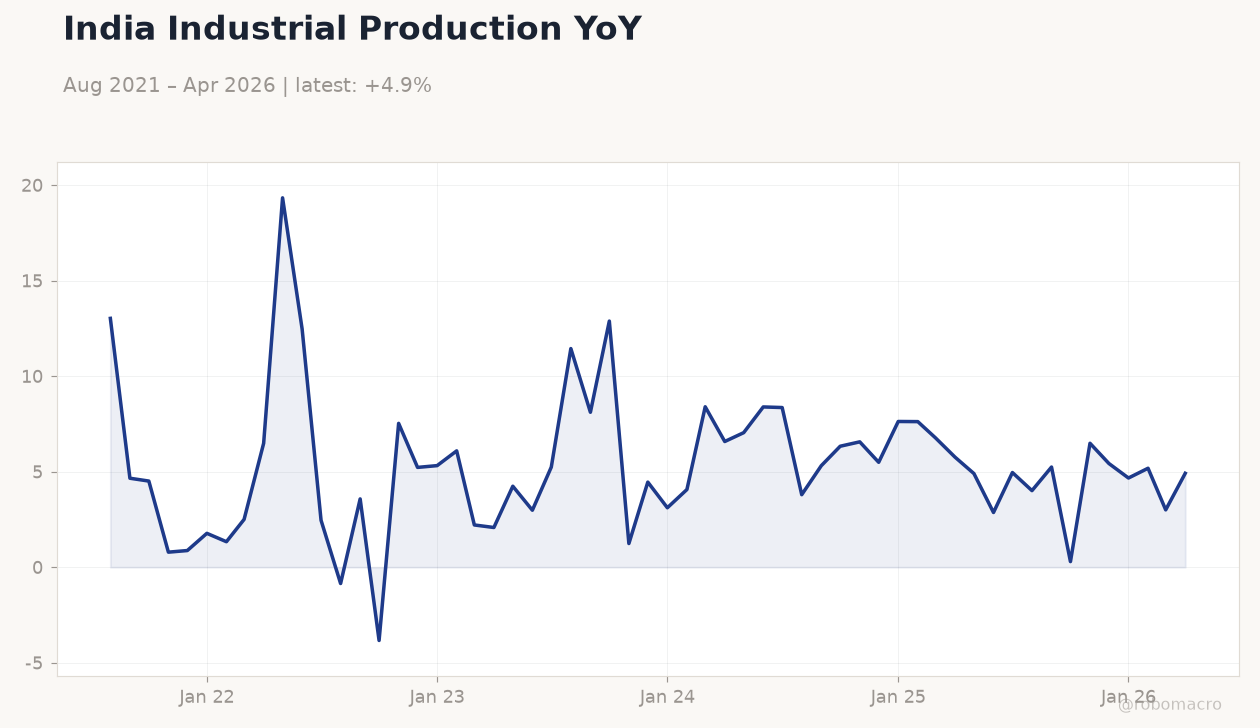

| Industrial Production Year-over-Year | 4.90 | 4.70 | 5.10 |

| Manufacturing Production Year-over-Year | 6.10 | - | 5.50 |

India Industrial Production YoY | Type: macro_line | YoY %: 4.916 (2026-04-01) | Range: -3.835–19.33 | Trend(5pt): 13.02,-3.835,4.455,7.621,4.916

India Industrial Production YoY | Type: macro_line | YoY %: 4.916 (2026-04-01) | Range: -3.835–19.33 | Trend(5pt): 13.02,-3.835,4.455,7.621,4.916

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Industrial production rose 5.1% YoY in May, above 4.7% consensus, while manufacturing output grew 5.5%.

- Nifty 50 climbed 0.59% to 24,005.85 and Sensex gained 0.58% to 76,922.64 as Brent crude fell 2.85%.

- USD/INR rose 0.34% to 95.24 with RBI intervention capping gains amid surging US Treasury yields.

Yesterday's Recap

Industrial production expanded 5.1% year-over-year, exceeding expectations, while manufacturing output increased 5.5%. Equity benchmarks closed higher with Nifty and Sensex both advancing nearly 0.6% as falling Brent crude eased imported inflation concerns. The rupee slipped to a two-week low at 95.24 against the dollar after US yields climbed, though RBI dollar sales limited further depreciation.

RBI’s latest report highlighted India’s continued vulnerability to energy price spikes from West Asia tensions given heavy import dependence. Banks’ gross non-performing assets fell to a multi-decadal low of 1.8%, underscoring sustained balance-sheet repair. Short-term rates stayed anchored at 5.50% with no liquidity stress evident in overnight markets.

The Day Ahead

Markets enter a data-light session with no major domestic releases scheduled. Attention will turn to US non-farm payrolls and Treasury yields for cues on external capital flows. Traders will monitor oil price movements given RBI warnings on imported inflation risks.

RBI Governor’s recent remarks on local-currency trade pacts may keep rupee internationalisation in focus. FII positioning and RBI intervention patterns remain key variables for USD/INR direction.

Other Economic Notes

Strong balance-of-payments fundamentals continue to underpin rupee resilience despite periodic external pressures. RBI’s forward guidance emphasises inflation targeting while supporting growth through calibrated liquidity management. Banks’ improving asset quality creates room for stronger credit expansion in the second half of the fiscal year.

Energy import dependence remains the primary external vulnerability flagged in recent RBI assessments.

Global Macro News

Brent crude declined sharply as supply signals improved, offering temporary relief to India’s current-account outlook. Rising US Treasury yields triggered broad dollar strength that pressured emerging-market currencies including the rupee. Societe Generale noted RBI intervention has capped rupee upside even as strong BoP flows provide underlying support.

<i>↓ p.2</i>