India Macro Daily(Beta Mode)

IIP Tops Forecasts as Rupee Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nifty 50 | 24,175.70 | +0.71% |

| Sensex | 77,502.12 | +0.75% |

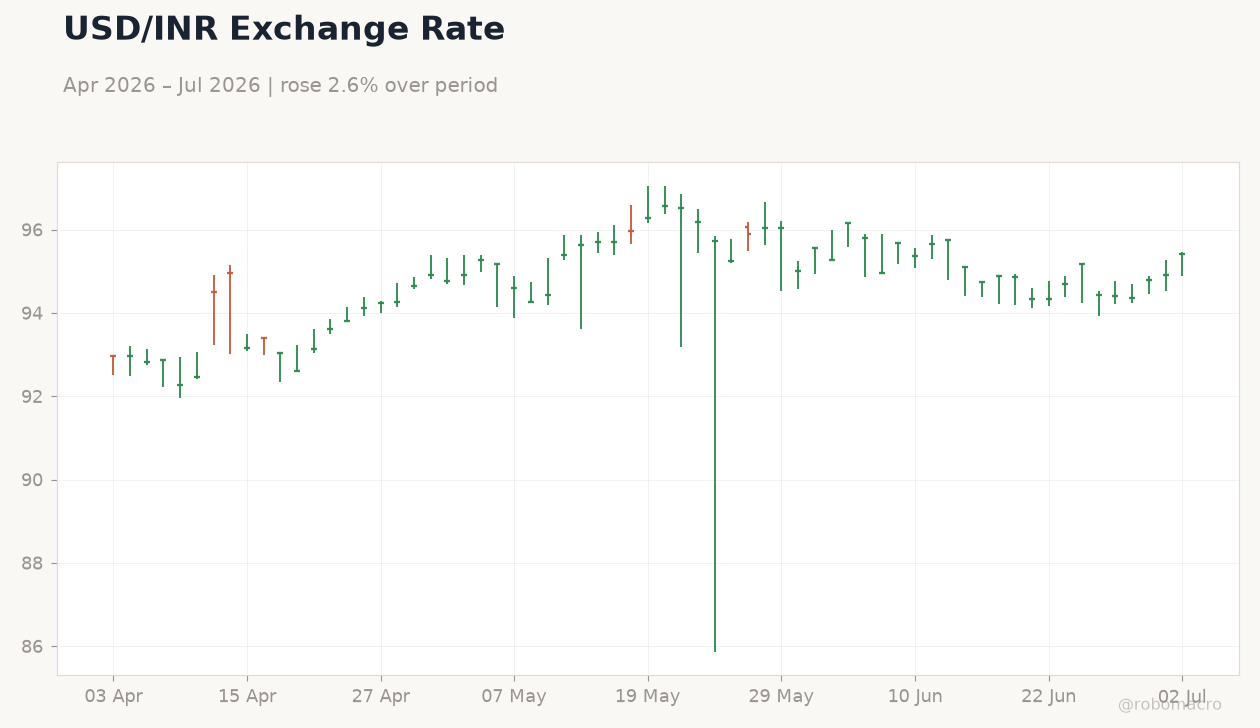

| USD/INR | 95.42 | +0.53% |

| EUR/INR | 108.30 | +0.31% |

| Reliance | 1,303.50 | -0.34% |

| HDFC Bank | 795.90 | -0.03% |

| Brent Crude | 71.51 | -0.08% |

| Gold | 4,153.30 | +2.09% |

| Bitcoin | 61,231.68 | +2.05% |

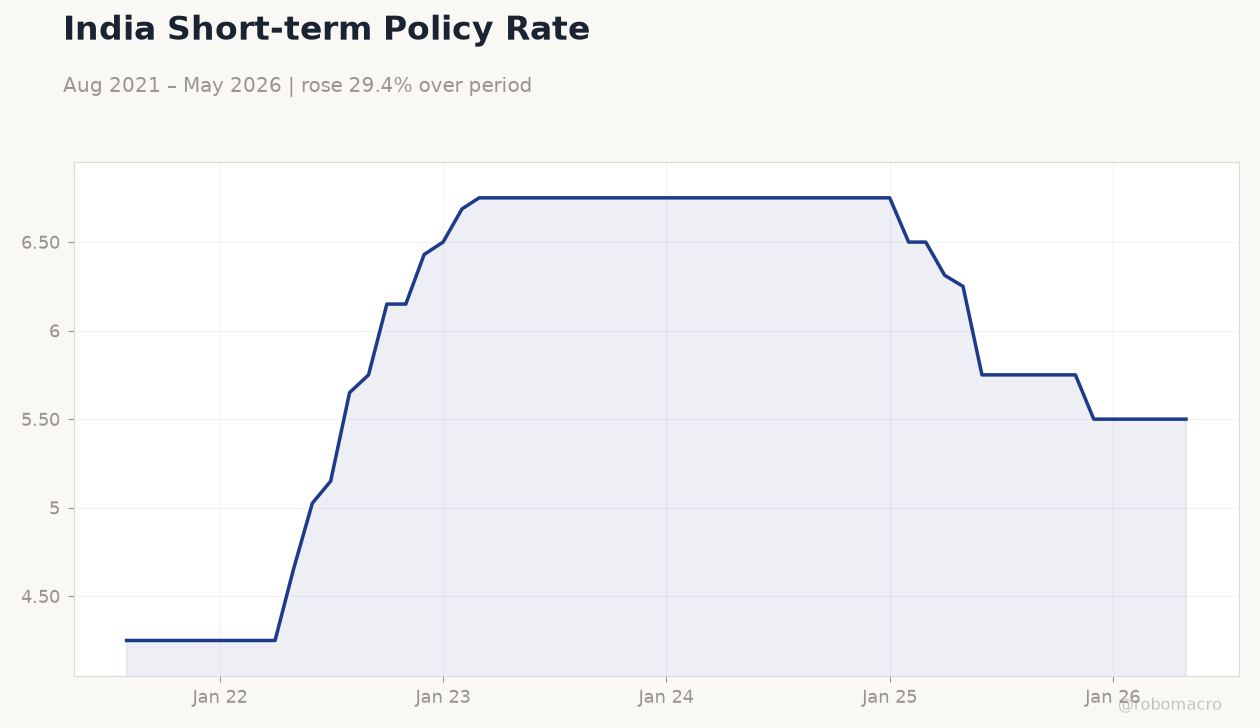

| India Short-term Rate | 5.50% | +0.00% |

| India Long-term Rate | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

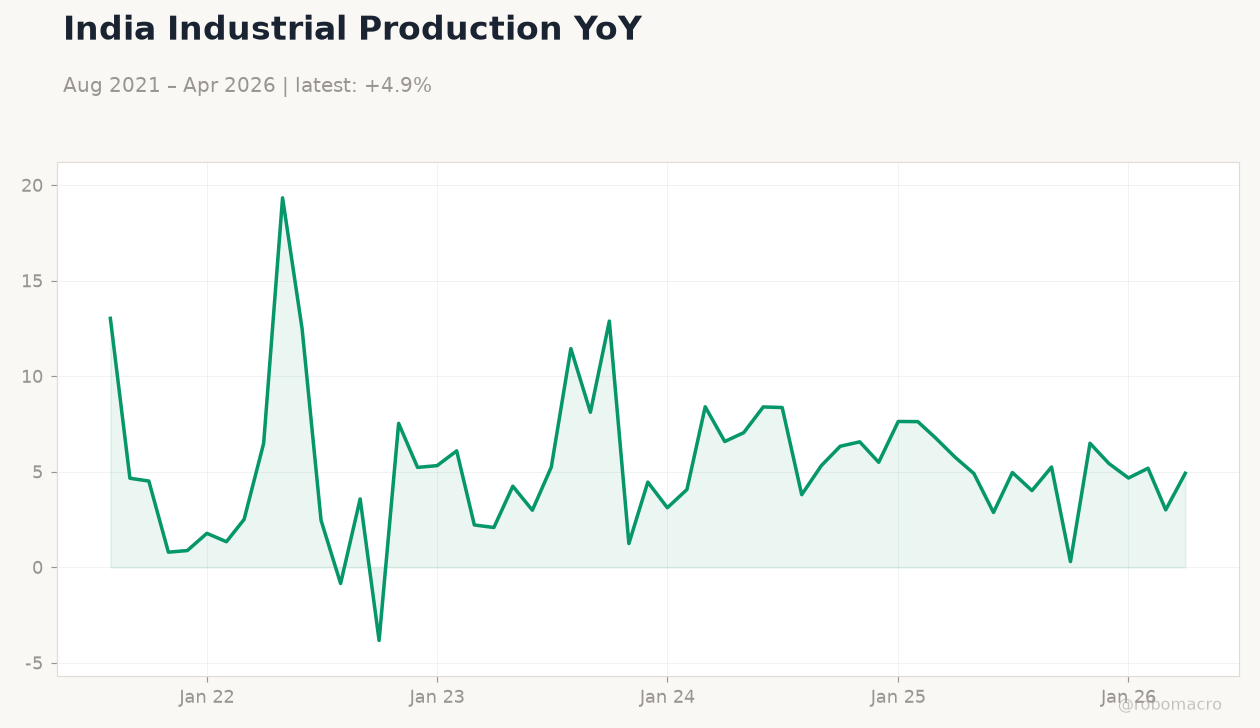

| Industrial Production Year-over-Year | 4.90 | 4.70 | 5.10 |

| Manufacturing Production Year-over-Year | 6.10 | - | 5.50 |

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,6.15,6.75,6.5,5.5

India Short-term Policy Rate | Type: macro_line | Rate %: 5.5 (2026-05-01) | Range: 4.25–6.75 | Trend(5pt): 4.25,6.15,6.75,6.5,5.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Industrial production rose 5.1% y/y in May, above the 4.7% consensus, while manufacturing output grew 5.5%.

- Nifty 50 advanced 0.71% to 24,175.70 and Sensex gained 0.75%, but USD/INR climbed 0.53% to 95.42 on thinner RBI support.

- RBI repo rate remains at 5.50%; markets now price the first cut only for late 2026 after stronger growth prints.

Yesterday's Recap

Industrial production expanded 5.1% y/y in May, exceeding the 4.7% consensus and prior 4.9% reading, while manufacturing production increased 5.5% against a 6.1% prior. Equity markets responded positively with Nifty 50 rising 0.71% to close at 24,175.70 and Sensex adding 0.75% to 77,502.12. The rupee came under pressure as USD/INR advanced 0.53% to 95.42 amid reduced RBI intervention and rising arbitrage outflows.

Gold climbed 2.09% to 4,153.30 while Brent crude eased 0.08% to 71.51. Short-term rates stayed anchored at 5.50% with no change in the policy stance. News flow highlighted RBI statements labeling cryptocurrency a threat to the economy and parliamentary scrutiny of the digital rupee.

The Day Ahead

No scheduled data releases or MPC member speeches are set for 2 July or 3 July. Traders will monitor RBI’s weekly statistical supplement for liquidity signals. Focus remains on rupee flows and any follow-up comments from the parliamentary panel on crypto risks.

Global cues from US yields and oil prices will influence INR direction given thin domestic calendars. Markets expect continued RBI efforts to smooth volatility through targeted intervention.

Other Economic Notes

India Inc holds substantial cash reserves yet shows limited conviction to deploy capital into new projects amid policy uncertainty. Strong balance-of-payments support and RBI’s steady stance continue to underpin the rupee despite short-term pressures from US Treasury yields. RBI currency swaps have improved overseas borrowing conditions for Indian financial institutions according to S&P assessments.

Corporate commentary from IT firms points to AI-driven deal momentum supporting medium-term growth.

Global Macro News

Softer US ISM data and dovish Fed minutes eased global yields, providing a modest tailwind for emerging-market assets including India. Surging US Treasury yields nevertheless weighed on INR despite India’s robust external position. Brent crude hovered near 71.51 amid OPEC+ supply discipline and Middle-East tensions.

<i>↓ p.2</i>