Japan Macro Daily(Beta Mode)

Japan Inflation Cools, PMIs Firm

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 56,825.70 | -1.12% |

| USD/JPY | 155.42 | +0.47% |

| EUR/JPY | 182.89 | +0.29% |

| GBP/JPY | 208.75 | +0.49% |

| Gold | 5,060.40 | +1.70% |

| Brent Crude | 70.98 | -0.95% |

| Bitcoin | 66,718.42 | -0.36% |

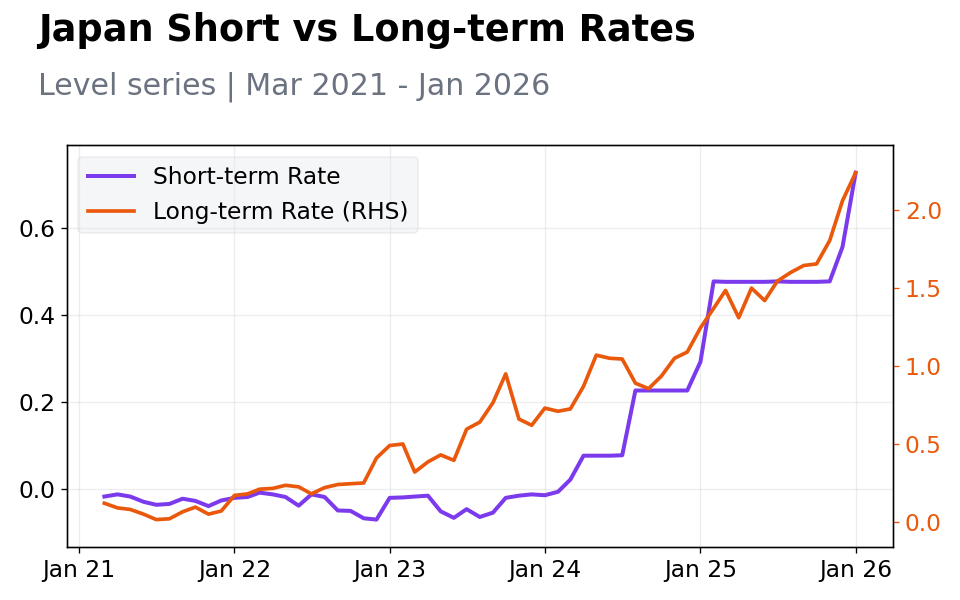

| Japan 2Y Govt Yield | 0.73% | +30.70% |

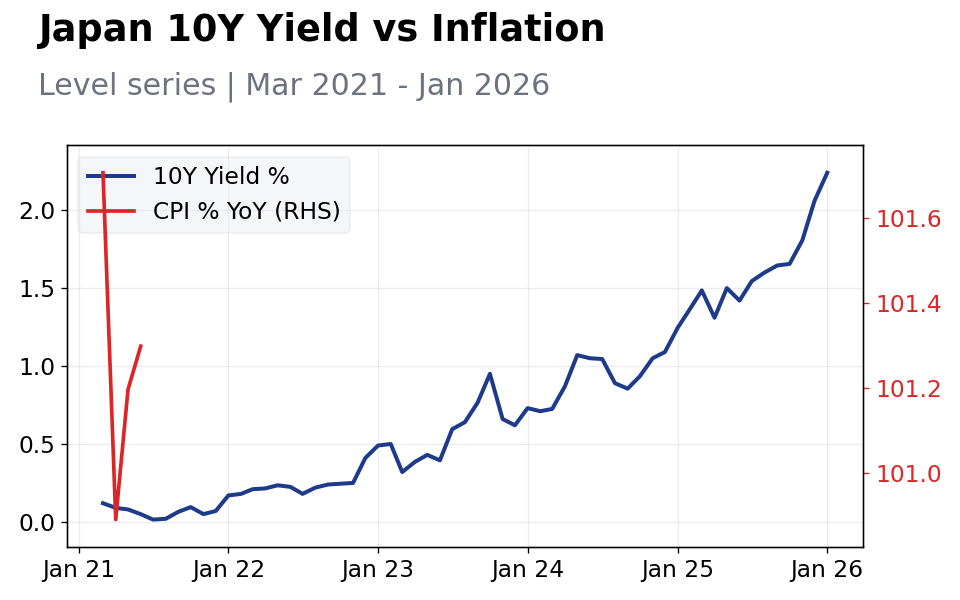

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.10 | - | 1.50 |

| Core Inflation Rate Year-over-Year | 2.40 | 2 | 2 |

| S&P Global Manufacturing PMI Flash | 51.50 | - | 52.80 |

| S&P Global Services PMI Flash | 53.70 | - | 53.80 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-02-26) | |||

| BoJ Takada Speech | - | - | 20:30 |

| Industrial Production Month-over-Month Preliminary | -0.10 | - | 18:50 |

| Retail Sales Year-over-Year | -0.90 | - | 18:50 |

| Friday (2026-02-27) | |||

| Housing Starts Year-over-Year | -1.30 | - | 00:00 |

- Japan's headline inflation eased to 1.5% YoY in January, missing expectations, while core held at 2.0% as forecast, easing pressure on BoJ policy.

- Flash PMIs rose, with manufacturing at 52.8 and services at 53.8, signaling ongoing expansion amid domestic resilience.

- Nikkei fell 1.12%, yen weakened with USD/JPY up 0.47% to 155.42, and JGB yields climbed sharply on tightening bets.

Yesterday's Recap

Japan's data highlighted cooling inflation, with headline CPI at 1.5% YoY from 2.1% prior, below consensus and reflecting yen strength curbing import prices. Core CPI dropped to 2.0% YoY from 2.4%, matching expectations and aligning with the BoJ's 2% target, though it questions rate hike urgency. Manufacturing PMI advanced to 52.8 from 51.5, boosted by stronger orders and production, while services PMI ticked up to 53.8 from 53.7, aided by solid demand.

The Nikkei 225 declined 1.12% to 56,825.70, hit by tech losses in a global risk-off mood. The yen depreciated modestly, with USD/JPY up 0.47% to 155.42, driven by wider rate differentials. JGB yields rose notably, with the 2-year up 30.70% to 0.73% and 10-year up 8.74% to 2.24%, as markets bet on BoJ normalization.

These shifts balanced easing inflation against economic strength.

The Day Ahead

Focus shifts to upcoming releases next week, including BoJ Takada's high-impact speech on February 25, potentially clarifying policy amid mixed data. On February 26, preliminary industrial production MoM and retail sales YoY will gauge sector health, following prior -0.1% and -0.9%. Housing starts YoY on February 27 tracks property trends after -1.3% previously.

These could drive yen and JGB moves. No events today, so global factors may dominate; watch for any surprise BoJ remarks.

Other Economic Notes

Japan's recovery appears steady but vulnerable to external shocks, with PMI gains indicating manufacturing and services momentum despite soft global demand. Wage trends are key for consumption, as lower inflation may relieve households but challenge BoJ's tightening path. Long-term issues like demographics and productivity persist, urging structural reforms to bolster growth.

Global Macro News

Global volatility affected Japan, with rising U.S. yields narrowing differentials and pressuring the yen, as USD/JPY climbed. European stocks weakened on ECB cut hints, lifting EUR/JPY 0.29% to 182.89 and GBP/JPY 0.49% to 208.75.

(cont...)