Japan Macro Daily(Beta Mode)

Nikkei Dips, Yields Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 56,825.70 | -1.12% |

| USD/JPY | 154.90 | -0.17% |

| EUR/JPY | 182.74 | +0.07% |

| GBP/JPY | 208.84 | -0.00% |

| Gold | 5,080.90 | +2.11% |

| Brent Crude | 71.30 | -0.50% |

| Bitcoin | 67,463.52 | -0.79% |

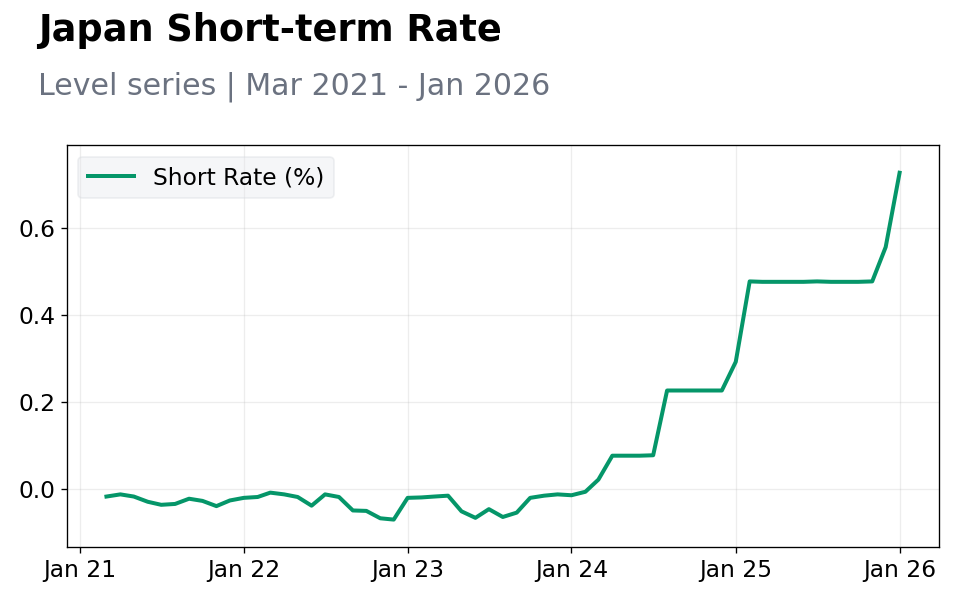

| Japan 2Y Govt Yield | 0.73% | +30.70% |

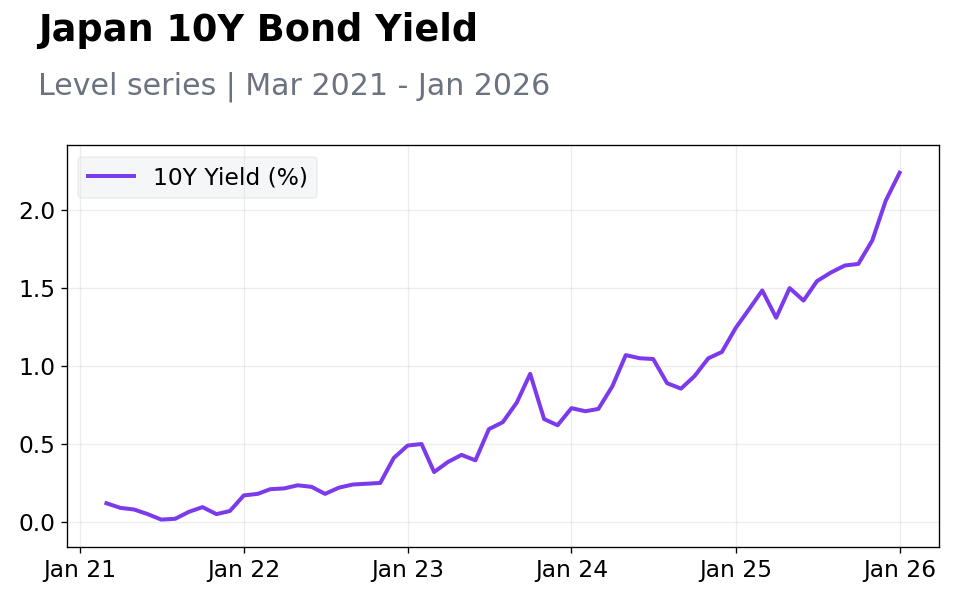

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nikkei 225 fell 1.12% to 56,825.70 amid global risk-off sentiment and geopolitical tensions.

- JGB yields rose sharply, with 10Y up 8.74% to 2.24% on BoJ tightening expectations.

- USD/JPY dipped 0.17% to 154.90, while gold climbed 2.11% as a safe haven.

Yesterday's Recap

Japanese markets faced downward pressure on February 21, with the Nikkei 225 closing at 56,825.70 after a 1.12% drop, primarily due to losses in exporters amid stable yen levels and broader global equity weakness. The USD/JPY pair declined 0.17% to 154.90, reflecting mild dollar softening, while EUR/JPY edged up 0.07% to 182.74 and GBP/JPY held flat at 208.84, showing varied currency responses to European economic resilience. Japanese Government Bond yields increased notably, with the 2-year yield rising 30.70% to 0.73% and the 10-year yield advancing 8.74% to 2.24%, driven by market bets on Bank of Japan policy normalization amid persistent inflation signals.

No major economic data was released, but sentiment was dampened by geopolitical headlines, including U.S. threats against Iran, which spurred safe-haven demand but pressured risk assets. Trading volumes were moderate, with financial stocks benefiting from higher yields, while tech and export sectors underperformed due to global uncertainties.

The Day Ahead

February 22 features no scheduled Japanese economic releases, shifting focus to global developments and potential unscheduled BoJ communications. Markets may react to overnight U.S. equity movements, particularly if tech rebounds influence Asian sentiment.

Yen pairs like USD/JPY could see volatility from U.S. Treasury yield shifts, with traders monitoring for intervention signals if depreciation accelerates. Geopolitical updates, such as U.S.-Iran tensions, may drive intraday swings in oil and safe-haven assets, indirectly affecting Japanese import costs and exporter margins.

Without data drivers, positioning for the upcoming BoJ meeting could sustain yield momentum.

Other Economic Notes

Japan's recovery remains uneven, with export growth supported by yen weakness but challenged by global demand slowdowns in key markets like China and the U.S. Inflation has stabilized above 2%, aiding BoJ's normalization efforts, though wage stagnation limits domestic consumption. Energy import dependencies heighten vulnerability to oil price fluctuations, as seen in recent Brent movements.

(cont...)