Japan Macro Daily(Beta Mode)

Nikkei Dips, Yields Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 56,825.70 | -1.12% |

| USD/JPY | 154.59 | -0.37% |

| EUR/JPY | 182.23 | -0.21% |

| GBP/JPY | 208.85 | +0.04% |

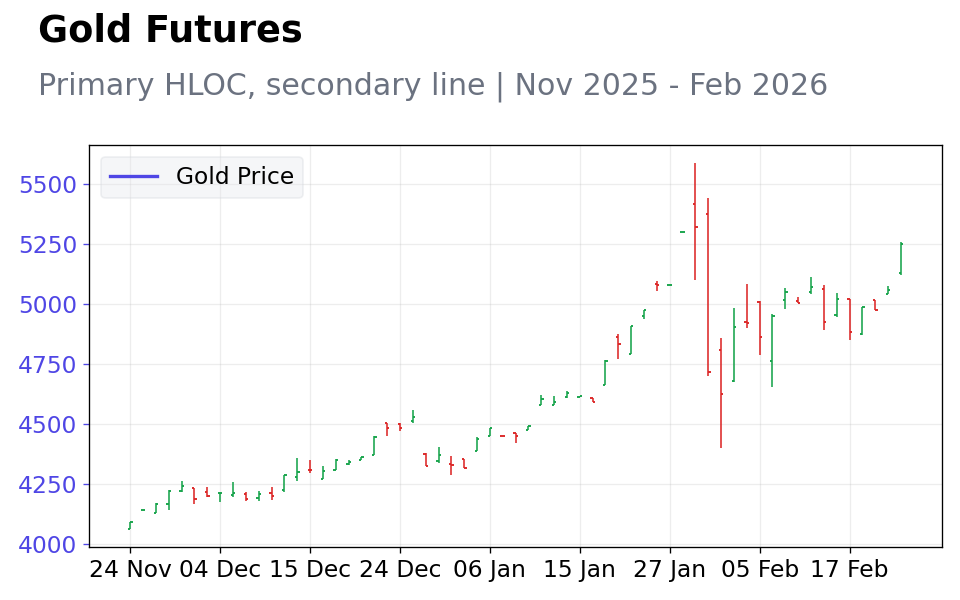

| Gold | 5,247.90 | +3.73% |

| Brent Crude | 71.10 | -0.92% |

| Bitcoin | 64,874.63 | -4.12% |

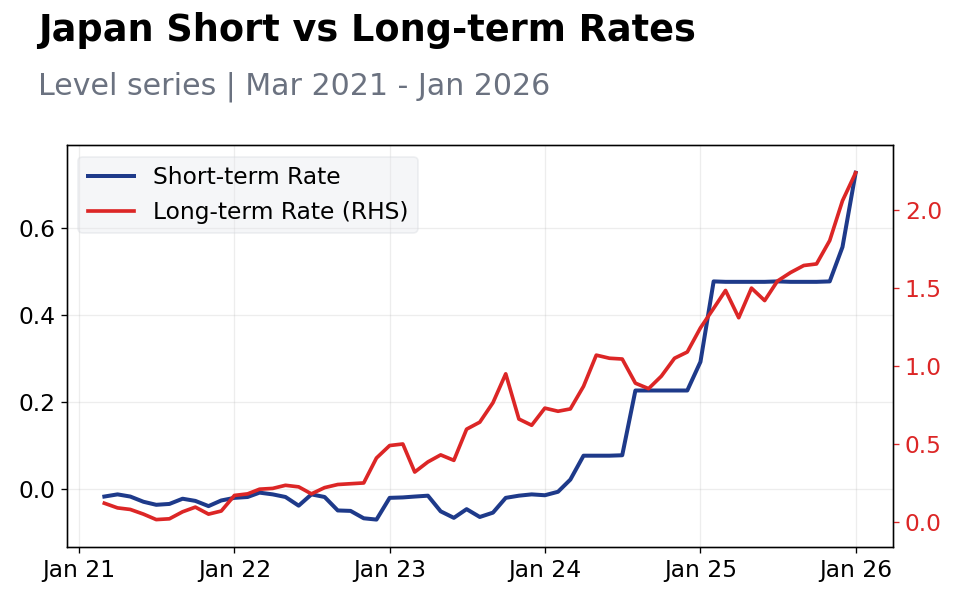

| Japan 2Y Govt Yield | 0.73% | +30.70% |

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-02-25) | |||

| BoJ Takada Speech | - | - | 15:30 |

| Thursday (2026-02-26) | |||

| Industrial Production Month-over-Month Preliminary | -0.10 | 5.30 | 13:50 |

| Retail Sales Year-over-Year | -0.90 | -0.40 | 13:50 |

| Friday (2026-02-27) | |||

| Housing Starts Year-over-Year | -1.30 | -1.60 | 19:00 |

- Nikkei 225 fell 1.12% to 56,825.70 amid global risk aversion, with tech stocks leading losses.

- JGB yields rose sharply, 2-year up 30.70% to 0.73% and 10-year up 8.74% to 2.24%, on BoJ hike expectations.

- Yen strengthened modestly versus USD, with USD/JPY down 0.37% to 154.59; gold surged 3.73% to 5,247.90.

Yesterday's Recap

Japanese markets faced a risk-off tone yesterday, with the Nikkei 225 declining 1.12% to close at 56,825.70, primarily due to profit-taking in technology sectors amid wider global equity softness. The yen appreciated slightly against the dollar, as USD/JPY decreased 0.37% to 154.59, bolstered by safe-haven demand despite U.S. economic strength.

EUR/JPY fell 0.21% to 182.23, while GBP/JPY edged up 0.04% to 208.85, showing mixed currency dynamics. Japanese Government Bond yields climbed significantly, with the 2-year yield increasing 30.70% to 0.73% and the 10-year yield rising 8.74% to 2.24%, reflecting growing market anticipation of Bank of Japan policy tightening amid persistent inflation signals. No major economic data was released yesterday, shifting focus to external drivers like gold's 3.73% gain to 5,247.90, which underscored safe-haven flows.

Brent crude slipped 0.92% to 71.10, easing Japan's energy import costs but highlighting global demand concerns. Bitcoin dropped 4.12% to 64,874.63, adding to volatility in risk assets. Export-oriented sectors felt pressure from the firmer yen, potentially curbing competitiveness, while bond market movements suggested ongoing yield curve adjustments in response to BoJ normalization bets.

The Day Ahead

Attention turns to the BoJ Takada speech on February 25 at 15:30 ET, which may offer guidance on monetary policy amid debates over rate normalization. On February 26 at 13:50 ET, preliminary industrial production month-over-month is forecasted at 5.3% compared to -0.1% prior, possibly indicating a rebound in manufacturing activity. Retail sales year-over-year, expected at -0.4% from -0.9% previous, could signal strengthening consumer demand.

Housing starts year-over-year, slated for February 26 at 19:00 ET with consensus at -1.6% versus -1.3% prior, will provide insights into the real estate market's resilience. These indicators may drive yen movements and influence JGB yield trajectories as traders position ahead of potential policy shifts.

Other Economic Notes

Japan's economic landscape continues to grapple with weak domestic consumption, as evidenced by recent trade figures emphasizing dependence on exports amid yen fluctuations. (cont...)