Japan Macro Daily(Beta Mode)

Nikkei Rises, Yields Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 57,321.09 | +0.87% |

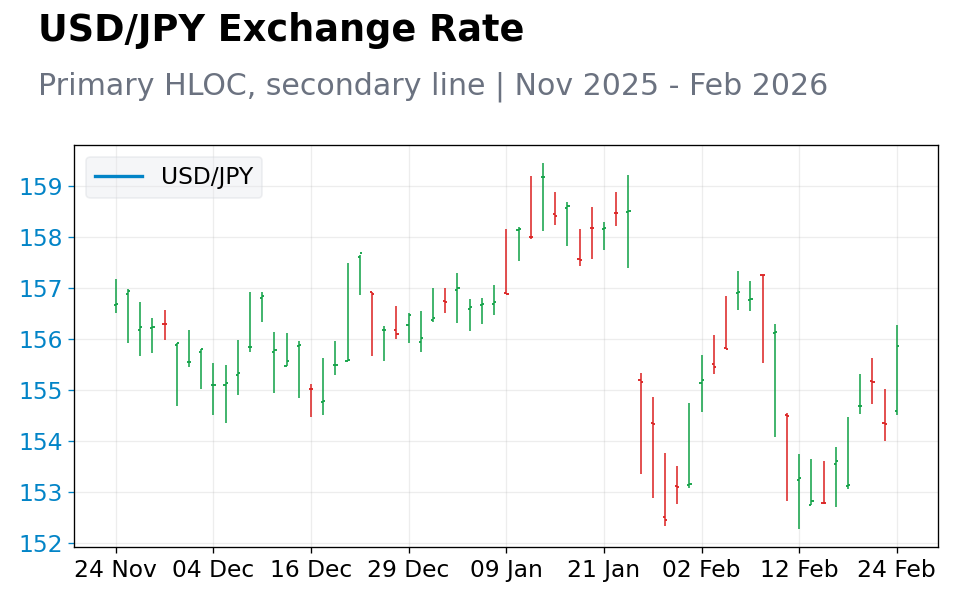

| USD/JPY | 155.82 | +0.96% |

| EUR/JPY | 183.46 | +0.44% |

| GBP/JPY | 210.24 | +0.66% |

| Gold | 5,160.50 | -0.85% |

| Brent Crude | 71.08 | -0.57% |

| Bitcoin | 64,168.06 | -0.69% |

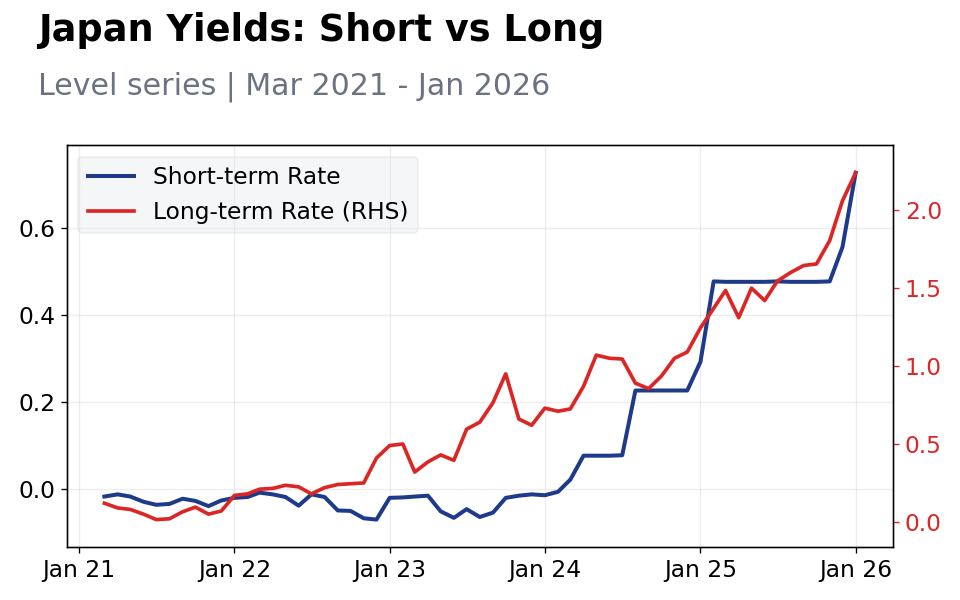

| Japan 2Y Govt Yield | 0.73% | +30.70% |

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-02-25) | |||

| BoJ Takada Speech | - | - | 15:30 |

| Thursday (2026-02-26) | |||

| Industrial Production Month-over-Month Preliminary | -0.10 | 5.30 | 13:50 |

| Retail Sales Year-over-Year | -0.90 | -0.40 | 13:50 |

| Friday (2026-02-27) | |||

| Housing Starts Year-over-Year | -1.30 | -1.60 | 19:00 |

- Nikkei 225 climbed 0.87% on tech gains, while JGB yields jumped amid BoJ tightening bets.

- Yen weakened versus majors, with USD/JPY up 0.96% on improved global risk sentiment.

- Key data and BoJ speech ahead to guide policy outlook.

Yesterday's Recap

Japanese markets displayed strength yesterday, with the Nikkei 225 advancing 0.87% to 57,321.09, fueled by export-focused tech stocks benefiting from reduced global AI supply chain worries. The broader TOPIX index presumably aligned, though details were absent, indicating general equity positivity. JGB yields rose significantly, with the 2-year yield increasing 30.70% to 0.73% and the 10-year yield up 8.74% to 2.24%, reflecting stronger anticipation of Bank of Japan policy shifts.

The yen lost ground, as USD/JPY rose 0.96% to 155.82, EUR/JPY gained 0.44% to 183.46, and GBP/JPY advanced 0.66% to 210.24, driven by a firmer dollar following U.S. tariff announcements. No significant economic indicators were released, enabling focus on earlier inflation trends and international news.

These dynamics highlighted market adjustments for possible BoJ rate increases amid ongoing price pressures.

The Day Ahead

Attention turns to the BoJ Takada speech on February 25 at 15:30 ET, high impact, potentially offering insights into normalization plans. On February 26, preliminary industrial production month-over-month data is due at 13:50 ET, consensus 5.3% versus prior -0.1%, indicating possible manufacturing upturn. Retail sales year-over-year follows at the same time, expected at -0.4% from -0.9%, shedding light on consumer activity.

Housing starts year-over-year arrives February 26 at 19:00 ET, forecasted at -1.6% versus -1.3%, reflecting housing sector trends. These events may drive yen movements and influence JGB yields.

Other Economic Notes

Japan's economy exhibits steady progress, with inflation above 2% bolstering BoJ's shift from ultra-loose policy. Wage developments are critical, as ongoing talks hint at increases that could support internal demand. Exports encounter challenges from international trade frictions, but domestic spending improves with tourism recovery.

Global Macro News

U.S. equities fell after President Trump intensified tariffs, including a 15% blanket increase, impacting Japanese exporters dependent on U.S. demand.

(cont...)