Japan Macro Daily(Beta Mode)

Nikkei Rallies, Yields Spike

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 58,583.12 | +2.20% |

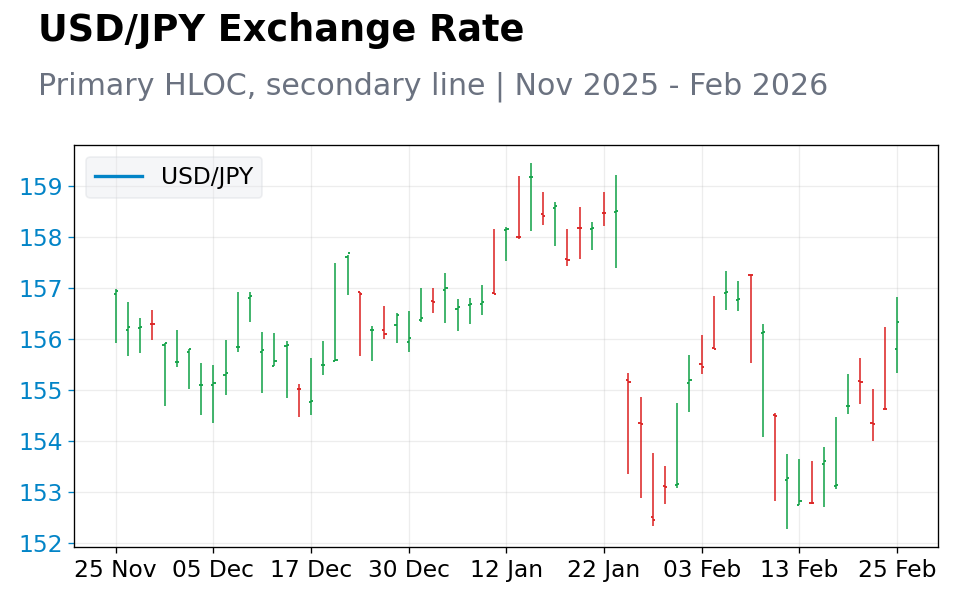

| USD/JPY | 156.33 | +1.10% |

| EUR/JPY | 184.59 | +1.22% |

| GBP/JPY | 211.86 | +1.52% |

| Gold | 5,183.70 | +0.54% |

| Brent Crude | 70.86 | +0.13% |

| Bitcoin | 69,166.44 | +7.94% |

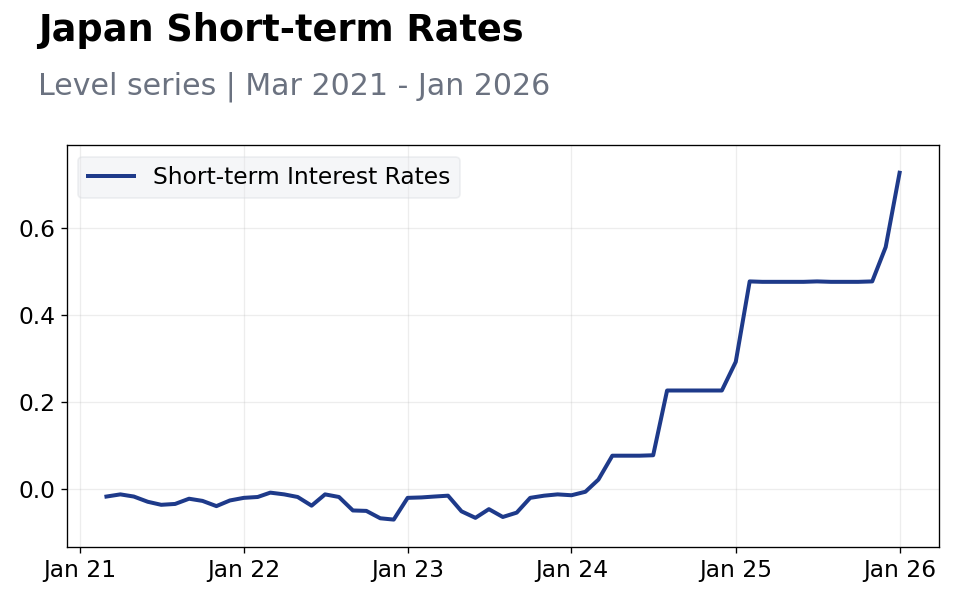

| Japan 2Y Govt Yield | 0.73% | +30.70% |

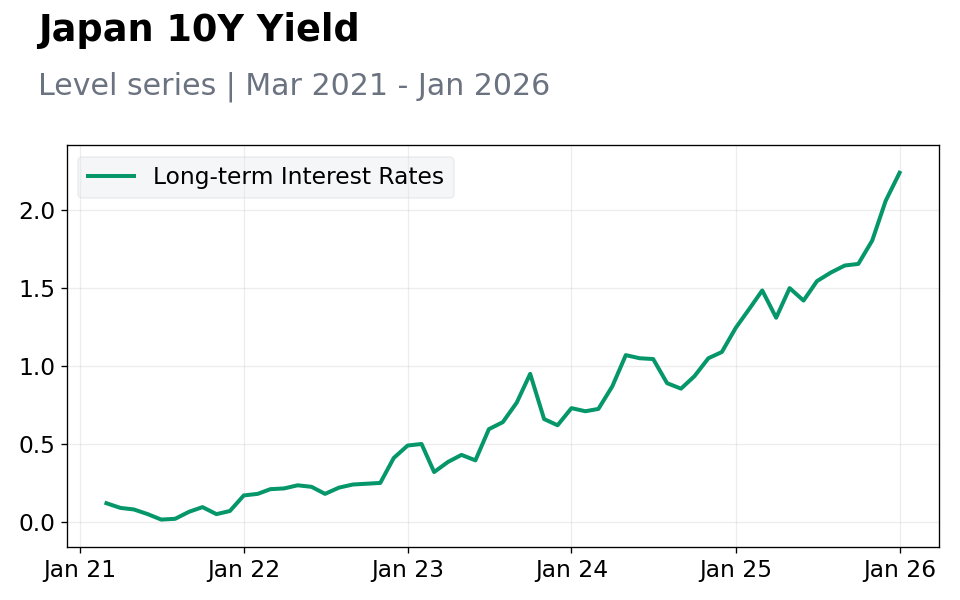

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoJ Takada Speech | - | - | 15:30 |

| Thursday (2026-02-26) | |||

| Industrial Production Month-over-Month Preliminary | -0.10 | 5.30 | 13:50 |

| Retail Sales Year-over-Year | -0.90 | -0.40 | 13:50 |

| Friday (2026-02-27) | |||

| Housing Starts Year-over-Year | -1.30 | -1.60 | 19:00 |

- Nikkei 225 surged 2.20% amid global risk-on sentiment, while JGB yields climbed sharply on policy normalization bets.

- Yen weakened with USD/JPY up 1.10%, reflecting stronger dollar and hawkish BoJ signals.

- No major data releases yesterday, but markets positioned for upcoming industrial and retail figures.

Yesterday's Recap

Japanese markets posted strong gains yesterday, with the Nikkei 225 closing at 58,583.12 after a 2.20% rally driven by tech and export sectors benefiting from a weaker yen. USD/JPY advanced 1.10% to 156.33, pressuring importers but boosting multinational earnings outlooks. JGB yields rose significantly, with the 10-year at 2.24% up 8.74% and the 2-year at 0.73% surging 30.70%, as investors priced in faster BoJ tightening amid persistent inflation.

EUR/JPY and GBP/JPY also strengthened, climbing 1.22% to 184.59 and 1.52% to 211.86 respectively, underscoring broad yen depreciation. Equity gains were supported by global commodity stability, with gold up 0.54% to 5,183.70 and Brent crude edging 0.13% higher to 70.86, though bitcoin's 7.94% jump to 69,166.44 highlighted crypto volatility spillover. Absent data releases, sentiment was shaped by anticipation of BoJ speeches and upcoming economic prints, with no immediate catalysts disrupting the bullish tone.

The Day Ahead

Today's calendar features a high-impact BoJ Takada speech at 15:30 ET, which could provide insights into policy normalization and yield curve adjustments. Markets will scrutinize any hints on rate hike timing amid recent yen weakness and inflation trends. Tomorrow brings medium-impact releases including industrial production MoM preliminary at 13:50 ET, expected at 5.3% versus prior -0.1%, signaling potential manufacturing rebound; retail sales YoY at the same time, forecasted at -0.4% from -0.9%, offering clues on consumer spending resilience; and housing starts YoY at 19:00 ET, projected at -1.6% from -1.3%, which may reflect ongoing real estate pressures from higher yields.

Other Economic Notes

Broader Japanese economic themes center on balancing inflation control with growth support, as persistent wage pressures and energy costs challenge the 2% target. Export competitiveness remains key, with yen depreciation aiding manufacturers but raising import inflation risks. Structural reforms in labor markets and digital transformation are gaining traction to address demographic headwinds and boost productivity.

Global Macro News

Global macro developments are influencing Japan through trade and currency channels, with U.S. Treasury yields rising on strong jobs data, pressuring JGBs and weakening the yen further. (cont...)