Japan Macro Daily(Beta Mode)

Capex Beats, Yields Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 56,279.05 | -3.06% |

| USD/JPY | 157.68 | +0.67% |

| EUR/JPY | 183.05 | -0.61% |

| GBP/JPY | 210.57 | +0.28% |

| Gold | 5,100.20 | -3.67% |

| Brent Crude | 82.22 | +5.76% |

| Bitcoin | 68,057.60 | -1.04% |

| Japan 2Y Govt Yield | 0.73% | +30.70% |

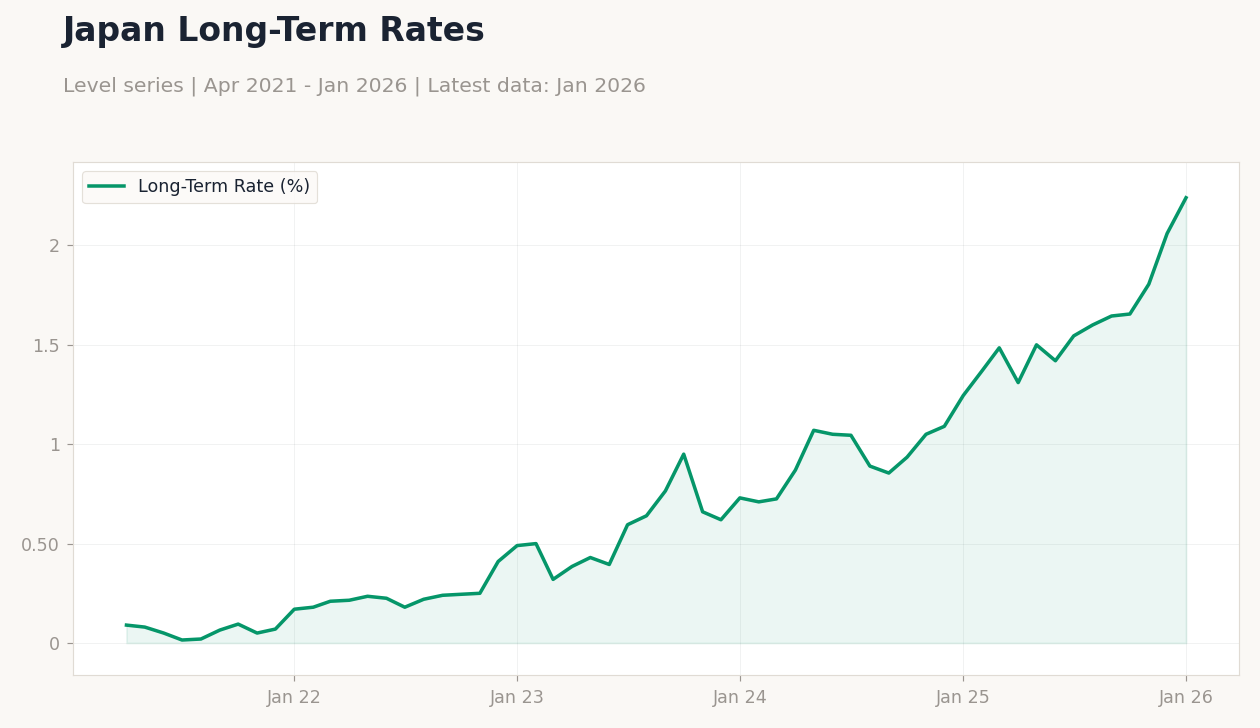

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 2.60 | 2.60 | 2.70 |

| Capital Spending Year-over-Year | 2.90 | 3 | 6.50 |

| BoJ Gov Ueda Speech | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-03-04) | |||

| Consumer Confidence Index | 37.90 | 38.20 | 19:00 |

| Sunday (2026-03-08) | |||

| Current Account Balance | 7,288,000m | - | 15:50 |

- Japan's unemployment ticked up to 2.7%, while capital spending surged 6.5% YoY, beating forecasts amid BoJ Governor Ueda's speech on data-driven policy.

- Nikkei 225 dropped 3.06% to 56,279.05 on global risk-off, with JGB yields rising sharply—2Y +30.70% to 0.73%, 10Y +8.74% to 2.24%.

- Yen weakened versus USD (+0.67% to 157.68), aiding exporters but pressured by oil disruptions and inflation concerns.

Yesterday's Recap

Japan's headline unemployment rate rose to 2.7% for the period, slightly above consensus of 2.6%, indicating mild labor market softening amid wage dynamics. Capital spending grew 6.5% year-over-year, exceeding the expected 3.0%, reflecting strong corporate outlays in tech and infrastructure despite broader challenges. Bank of Japan Governor Kazuo Ueda gave a key speech, stressing data-dependent policy without explicit hints on near-term rate adjustments, viewed as prudent given yen trends.

The Nikkei 225 fell 3.06% to 56,279.05, hit by global volatility and equity declines, though yen weakening (USD/JPY up 0.67% to 157.68) typically supports exporters. JGB yields climbed, with the 2-year up 30.70% to 0.73% and 10-year up 8.74% to 2.24%, tied to normalization expectations and external shocks. EUR/JPY declined 0.61% to 183.05, while GBP/JPY rose 0.28% to 210.57, showing mixed currency pressures.

These shifts occur against verified Japan CPI YoY at -0.50% as of mid-2021, with news suggesting potential upward trends from energy and imports.

The Day Ahead

Japan's consumer confidence index is set for release at 19:00 ET, with consensus at 38.2 versus prior 37.9, possibly signaling better household views on wages and economy. No other significant data today, shifting attention to global factors like U.S. indicators.

Further ahead, current account balance is due March 8 at 15:50 ET, offering insights into trade amid yen depreciation. Markets will watch for echoes of Ueda's speech on policy. Oil supply issues from Iran could influence sentiment, with today's light calendar potentially heightening reactions to yields and forex moves.

Other Economic Notes

Japan's yen has lost purchasing power to one-third over three decades, raising import costs and straining households amid price rises in essentials. Japanese investments in China continue to grow despite tensions, strengthening ties in chips and autos. The government now holds 11% voting rights in Rapidus Corp to boost local semiconductor output, reducing foreign dependency as global AI investments shift toward hardware makers.