Japan Macro Daily(Beta Mode)

Yields Surge on Robust Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 54,245.54 | -3.61% |

| USD/JPY | 157.02 | -0.15% |

| EUR/JPY | 182.68 | -0.67% |

| GBP/JPY | 209.92 | -0.45% |

| Gold | 5,148.10 | +0.80% |

| Brent Crude | 82.55 | +1.41% |

| Bitcoin | 73,234.52 | +7.23% |

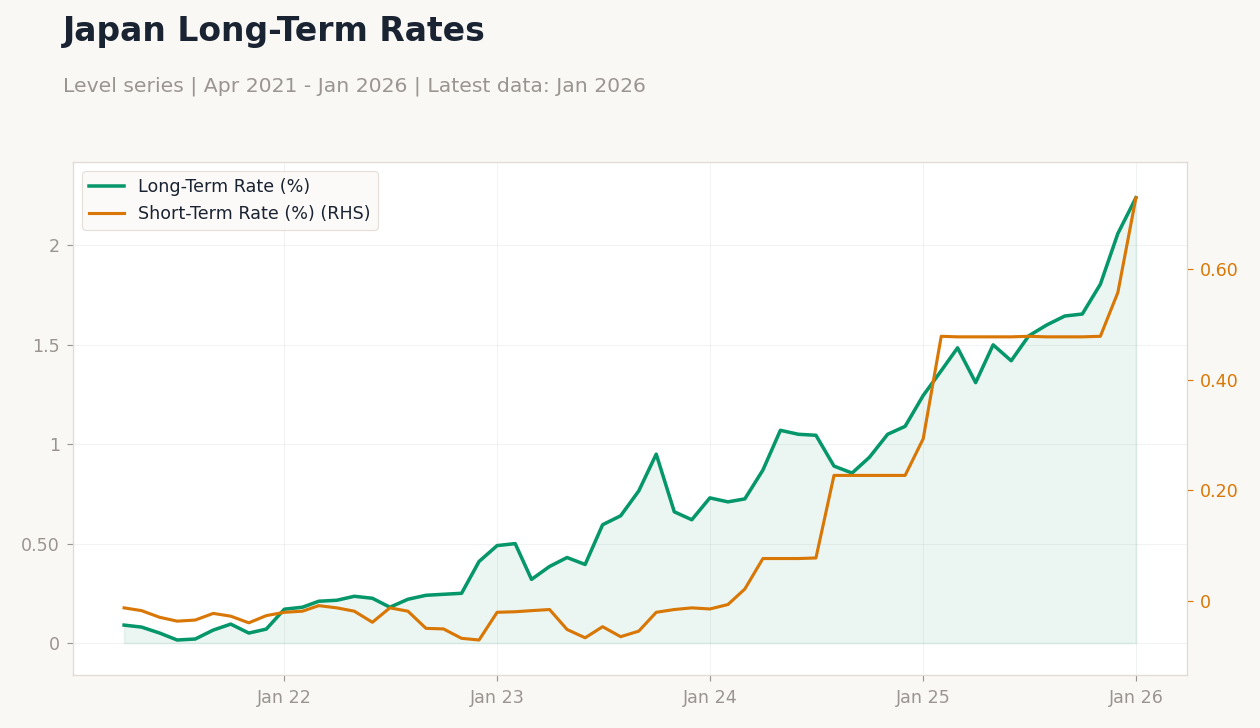

| Japan 2Y Govt Yield | 0.73% | +30.70% |

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 2.60 | 2.60 | 2.70 |

| Capital Spending Year-over-Year | 2.90 | 3 | 6.50 |

| BoJ Gov Ueda Speech | - | - | - |

| Consumer Confidence Index | 37.90 | 38.20 | 40 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Sunday (2026-03-08) | |||

| Current Account Balance | 7,288,000m | - | 15:50 |

- Unemployment ticked higher to 2.7%, while capital spending surged to 6.5% YoY, beating expectations and signaling corporate strength.

- Consumer confidence jumped to 40.0, exceeding consensus and reflecting improved household sentiment amid recovery hopes.

- Nikkei plunged 3.61% amid global risk-off, but JGB yields rose sharply, with 2Y up 30.70% to 0.73%, tracking BoJ normalization bets.

Yesterday's Recap

Japan's unemployment rate rose unexpectedly to 2.7% from 2.6%, missing consensus and highlighting labor market softening despite a tight jobs environment. Capital spending accelerated to 6.5% YoY, far surpassing the 3% forecast and previous 2.9%, driven by investments in tech and manufacturing amid export recovery. Consumer confidence soared to 40.0, beating the 38.2 consensus and prior 37.9, buoyed by wage gains and easing inflation pressures.

Bank of Japan Governor Ueda delivered a speech emphasizing gradual policy normalization, which markets interpreted as hawkish, pushing JGB yields higher. The Nikkei 225 tumbled 3.61% to 54,245.54, pressured by global equity sell-offs and yen strength concerns. USD/JPY dipped 0.15% to 157.02, while the 10Y JGB yield climbed 8.74% to 2.24%, reflecting bets on tighter policy.

Overall, equities faced headwinds from risk aversion, but bond markets priced in stronger growth signals from the data beats.

The Day Ahead

Today's calendar lacks major Japanese economic releases, providing markets a breather after yesterday's data-heavy session. Attention may shift to global developments, including any spillover from Asian equity weakness and oil price volatility. No key events are scheduled for tomorrow, March 5, allowing focus on digesting recent indicators like capital spending strength.

Looking further, the next notable release is the current account balance on March 8, which could influence yen dynamics if it shows export resilience. Traders should monitor BoJ commentary echoes, as normalization signals could sustain yield momentum. Overall, a quiet period may amplify external factors like U.S.

dollar movements on Japanese assets.

Other Economic Notes

Broader Japanese economic themes point to uneven recovery, with robust capital spending contrasting modest unemployment upticks, suggesting firms are prioritizing efficiency over hiring. Wage growth remains a critical watchpoint for sustained consumption, especially as consumer confidence improves but inflation lingers below target. Structural reforms in labor and energy sectors could bolster long-term growth, amid demographic challenges like an aging population.