Japan Macro Daily(Beta Mode)

Yen Weakens on BoJ Uncertainty

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 55,620.84 | +0.62% |

| USD/JPY | 158.01 | +0.30% |

| EUR/JPY | 182.50 | -0.20% |

| GBP/JPY | 211.70 | +0.61% |

| Gold | 5,158.70 | +1.84% |

| Brent Crude | 92.69 | +8.52% |

| Bitcoin | 67,255.60 | -0.03% |

| Japan 2Y Govt Yield | 0.73% | +30.70% |

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Headline Unemployment Rate | 2.60 | 2.60 | 2.70 |

| Capital Spending Year-over-Year | 2.90 | 3 | 6.50 |

| BoJ Gov Ueda Speech | - | - | - |

| Consumer Confidence Index | 37.90 | 38.20 | 40 |

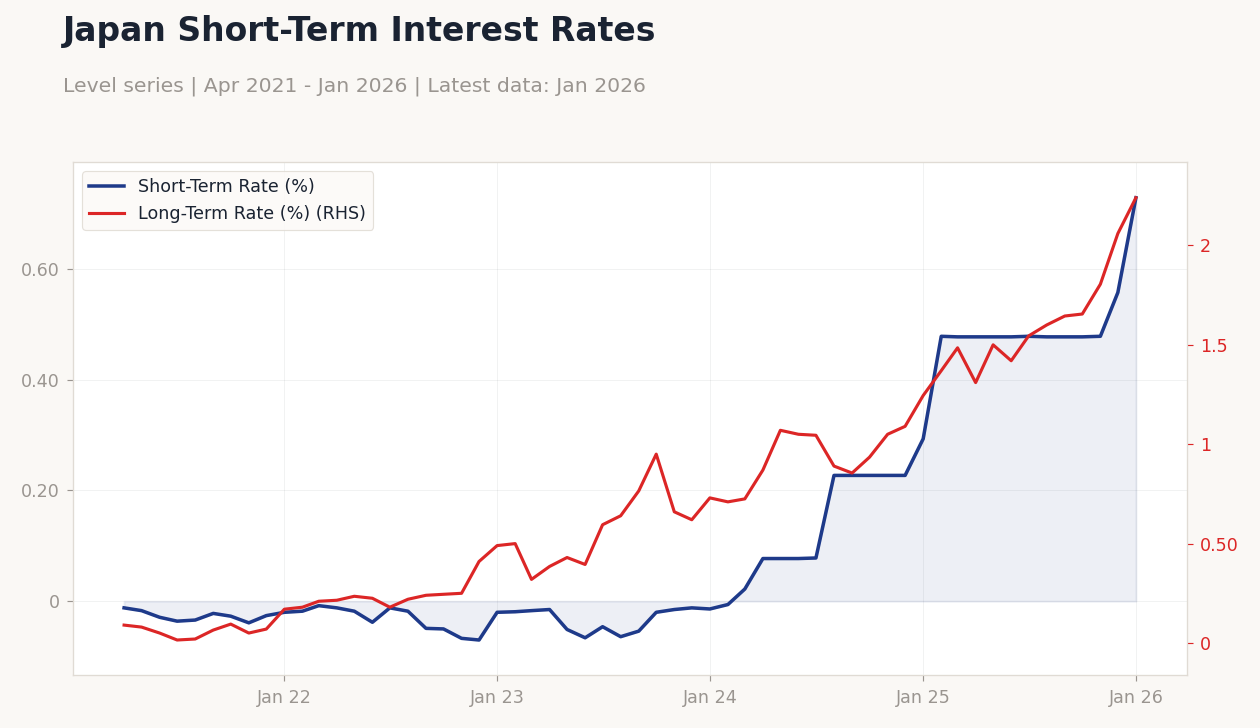

Japan Short-Term Interest Rates | Type: macro_line | Short-Term Rate (%): 0.728 (2026-01-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728 | Long-Term Rate (%): 2.24 (2026-01-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.24

Japan Short-Term Interest Rates | Type: macro_line | Short-Term Rate (%): 0.728 (2026-01-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728 | Long-Term Rate (%): 2.24 (2026-01-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.24

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Balance | 728,800m | 960,000m | 15:50 |

- Japanese unemployment rose to 2.7%, capital spending surged to 6.5% YoY, and consumer confidence climbed to 40.0, showing mixed economic signals.

- Nikkei 225 rose 0.62% to 55,620.84, USD/JPY gained 0.30% to 158.01, amid yen pressure from global tensions.

- JGB yields jumped, with 2-year at 0.73% (+30.70%) and 10-year at 2.24% (+8.74%), reflecting BoJ policy doubts.

Yesterday's Recap

Japanese data revealed unemployment edging up to 2.7% from 2.6%, slightly above consensus, indicating minor labor market softening. Capital spending accelerated to 6.5% YoY, exceeding expectations of 3% and previous 2.9%, underscoring strong corporate activity. Consumer confidence advanced to 40.0 from 37.9, surpassing forecasts of 38.2 and suggesting improved household outlook.

BoJ Governor Ueda's speech focused on steady policy tweaks without new commitments, adding to market fluctuations. The Nikkei 225 increased 0.62% to 55,620.84, supported by exporter benefits from yen softening, despite general wariness. USD/JPY advanced 0.30% to 158.01, EUR/JPY fell 0.20% to 182.50, and GBP/JPY rose 0.61% to 211.70, influenced by risk aversion.

JGB yields rose notably, with the 2-year yield at 0.73% (+30.70%) and 10-year at 2.24% (+8.74%), as traders factored in possible BoJ shifts amid Iran-related concerns. These developments highlighted uncertainty, with yen movements strained by external factors like oil price spikes.

The Day Ahead

Focus today is on Japan's current account balance at 15:50 ET, with consensus at 960 billion yen against previous 728.8 billion yen, which could shape yen views if it reflects trade vigor. Tomorrow lacks major events, giving markets time to process recent indicators and international news. Attention will stay on Middle East fallout, potentially raising Japanese import expenses through energy channels.

Without BoJ events, currency swings may persist based on global risk sentiment.

Other Economic Notes

Japan's economy contends with yen depreciation, which could heighten import costs despite the verified CPI YoY at -0.50% as of 2021-06-01, with indications of recent upward shifts. The 6.5% capital spending rise signals investment-driven progress, aiding GDP even as unemployment ticked higher. Consumer confidence at 40.0 points to bolstering internal demand, yet external risks like conflicts may hinder export areas.

These elements suggest resilience but vulnerability to global disruptions.