Japan Macro Daily(Beta Mode)

Spending Misses, GDP Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 54,248.39 | +2.88% |

| USD/JPY | 158.02 | -0.26% |

| EUR/JPY | 183.51 | +0.52% |

| GBP/JPY | 212.01 | +0.61% |

| Gold | 5,204.80 | +2.23% |

| Brent Crude | 87.84 | -11.24% |

| Bitcoin | 70,265.76 | +2.72% |

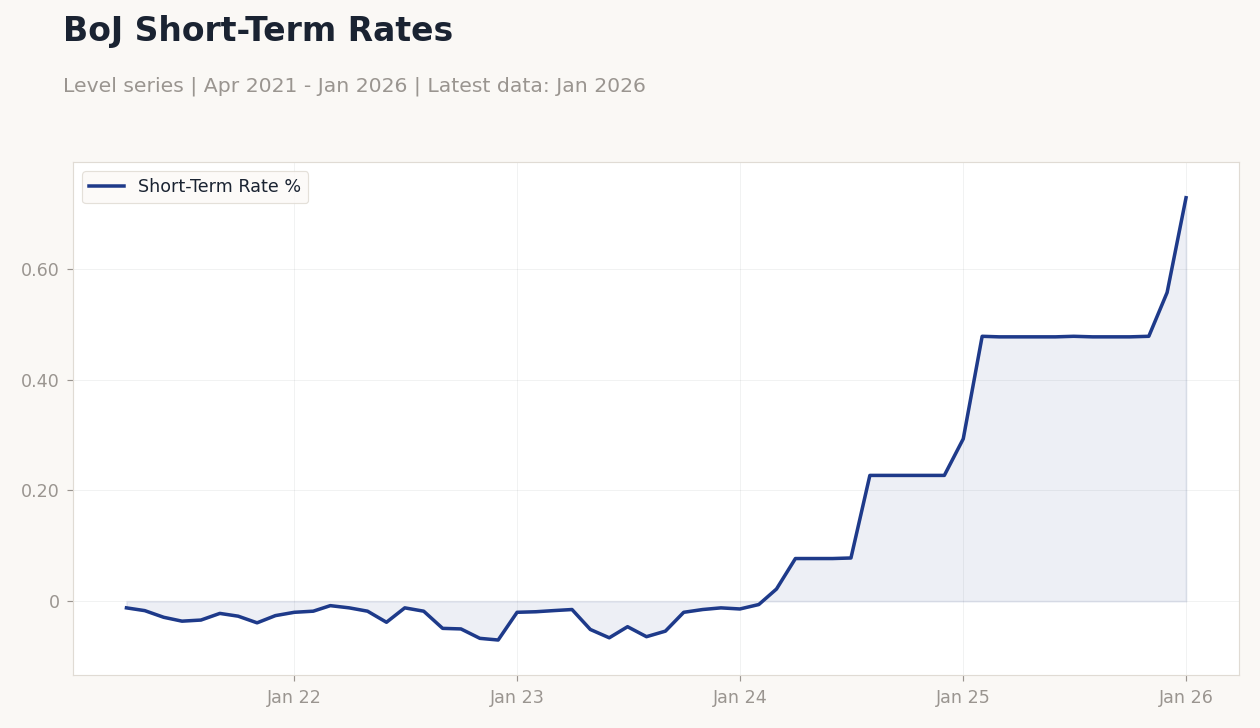

| Japan 2Y Govt Yield | 0.73% | +30.70% |

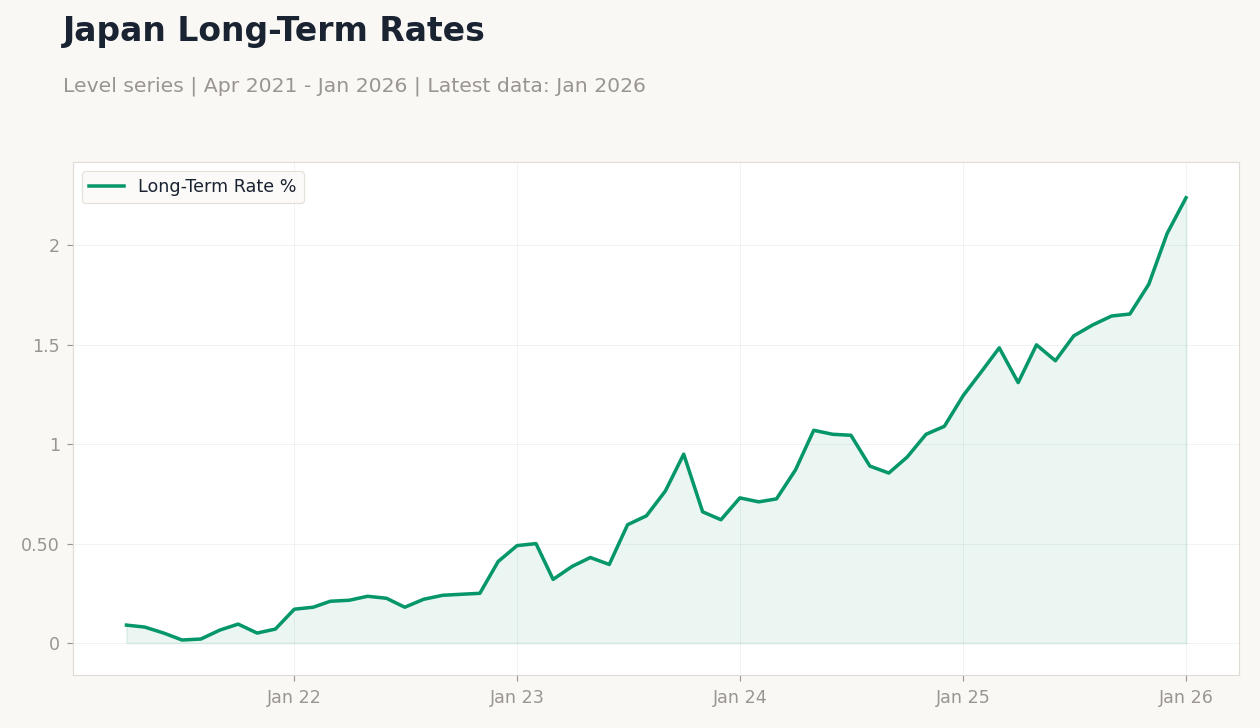

| Japan 10Y Govt Yield | 2.24% | +8.74% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Household Spending Month-over-Month | -2.90 | 0.80 | -2.50 |

| Household Spending Year-over-Year | -2.60 | 2.50 | -1 |

| GDP Growth Annualized Final | -2.60 | 1.20 | 1.30 |

| GDP Growth Quarter-over-Quarter Final Estimate | -0.70 | 0.30 | 0.30 |

BoJ Short-Term Rates | Type: macro_line | Short-Term Rate %: 0.728 (2026-01-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

BoJ Short-Term Rates | Type: macro_line | Short-Term Rate %: 0.728 (2026-01-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Household spending disappointed with MoM at -2.5% vs consensus 0.8%, signaling consumer weakness amid inflation pressures.

- GDP finalized at 1.3% annualized, slightly above expectations, supporting modest growth outlook.

- Nikkei surged 2.88% on global risk appetite, while JGB yields rose amid BoJ tightening bets.

Yesterday's Recap

Japanese household spending data released on March 9 missed estimates, with month-over-month figures at -2.5% against a consensus of 0.8%, and year-over-year at -1% versus 2.5%, highlighting persistent consumer caution despite wage gains. The final GDP estimates aligned closely with forecasts, showing annualized growth of 1.3% compared to 1.2% expected, and quarter-over-quarter at 0.3% as anticipated, indicating stable but tepid expansion. Markets reacted positively to the GDP print, pushing the Nikkei 225 up 2.88% to 54,248.39, driven by tech and export sectors amid yen weakness.

The USD/JPY pair dipped 0.26% to 158.02, reflecting safe-haven flows, while EUR/JPY and GBP/JPY gained 0.52% and 0.61% respectively. Japanese government bond yields climbed, with the 2-year at 0.73% up 30.70% and 10-year at 2.24% up 8.74%, fueled by speculation of further BoJ policy normalization. Overall, equities rallied on global cues, but spending weakness tempered optimism for domestic demand recovery.

The Day Ahead

No major economic data releases are scheduled for March 10 in Japan, allowing markets to digest yesterday's figures and global developments. Attention may shift to broader Asian market movements, particularly in response to oil price volatility and currency fluctuations. Investors will monitor any unscheduled BoJ communications or government statements on fiscal policy.

With no events tomorrow on March 11 either, focus could extend to upcoming wage negotiations influencing inflation trends. Traders should watch yen pairs for potential interventions amid recent underperformance.

Other Economic Notes

Broader themes in Japan's economy include mounting stagflation risks from surging oil prices and a weakening yen, as noted in recent analyses, potentially pressuring the government for increased fiscal support. Wage data showing strong growth fuels expectations for sustained inflation, aligning with BoJ's normalization path despite deflationary history. Consumer sentiment remains fragile, with household spending misses underscoring challenges in achieving robust domestic demand amid global uncertainties.