Japan Macro Daily(Beta Mode)

Japan GDP Meets Forecasts, Spending Misses

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 55,025.37 | +1.43% |

| USD/JPY | 158.91 | +0.67% |

| EUR/JPY | 183.79 | +0.24% |

| GBP/JPY | 213.08 | +0.57% |

| Gold | 5,184.20 | -0.87% |

| Brent Crude | 90.28 | +2.82% |

| Bitcoin | 70,571.13 | +0.92% |

| Japan 2Y Govt Yield | 0.73% | +30.70% |

| Japan 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Household Spending Month-over-Month | -2.90 | 0.80 | -2.50 |

| Household Spending Year-over-Year | -2.60 | 2.50 | -1 |

| GDP Growth Annualized Final | -2.60 | 1.20 | 1.30 |

| GDP Growth Quarter-over-Quarter Final Estimate | -0.70 | 0.30 | 0.30 |

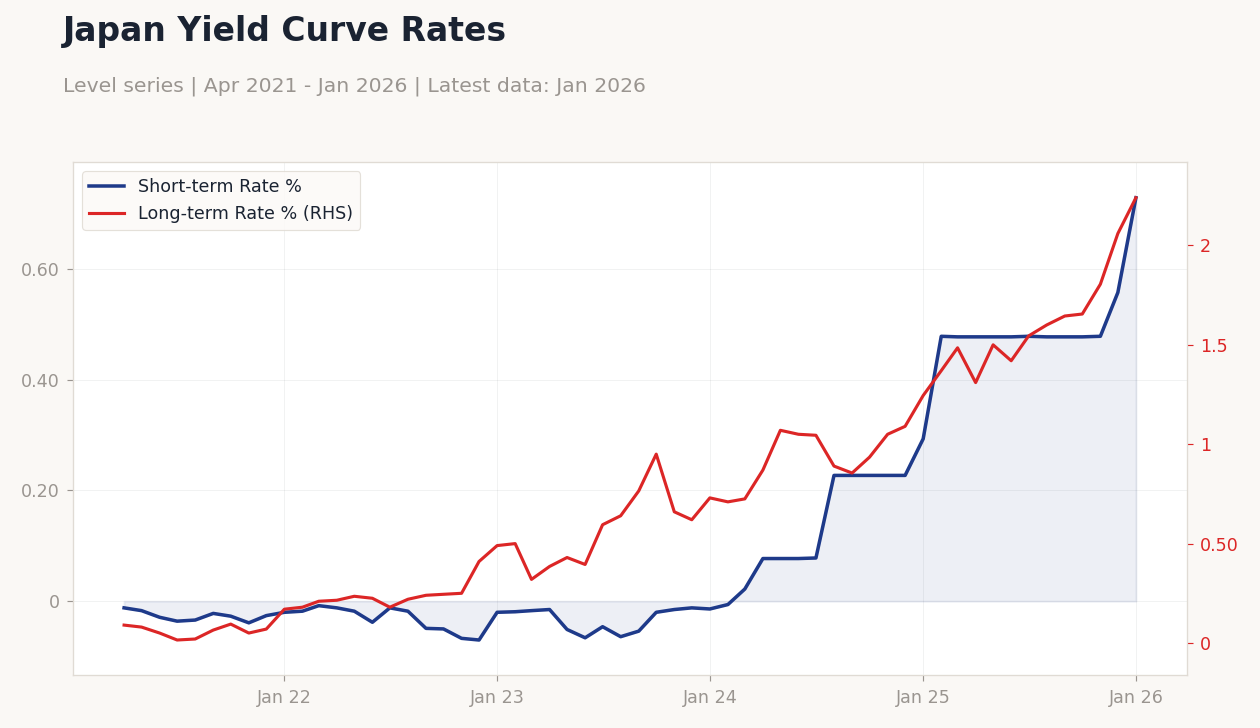

Japan Yield Curve Rates | Type: macro_line | Short-term Rate %: 0.728 (2026-01-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728 | Long-term Rate %: 2.24 (2026-01-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.24

Japan Yield Curve Rates | Type: macro_line | Short-term Rate %: 0.728 (2026-01-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728 | Long-term Rate %: 2.24 (2026-01-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.24

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Household spending fell short with MoM at -2.5% vs consensus 0.8%, indicating continued consumer restraint amid cost pressures.

- Final GDP data aligned with estimates at 1.3% annualized and 0.3% QoQ, bolstered by corporate investment.

- Nikkei rose 1.43% on exporter gains, while USD/JPY climbed 0.67% amid oil-driven global volatility.

Yesterday's Recap

Japan's household spending data disappointed, registering -2.5% month-over-month against a consensus of 0.8%, underscoring persistent weakness in consumer activity due to high living expenses. Year-over-year spending also lagged at -1% versus an expected 2.5%, heightening worries about slow domestic recovery. Final GDP figures were in line with projections, posting 1.3% annualized growth compared to consensus 1.2%, aided by robust capital spending.

Quarter-over-quarter GDP remained at 0.3%, affirming a mild recovery from the previous quarter's decline. Equities performed well, with the Nikkei 225 advancing 1.43% to 55,025.37, supported by gains in export-oriented firms as the yen depreciated. The USD/JPY pair gained 0.67% to 158.91, and the Japan 2-year government yield increased 30.70% to 0.73%, signaling stronger expectations for policy tightening.

These outcomes painted a varied economic landscape, with solid growth indicators tempered by consumer challenges.

The Day Ahead

No significant economic releases are planned for today, allowing markets to process recent data and international events. Focus may turn to Asian market responses to Middle East tensions affecting oil dynamics. Tomorrow similarly has no major events, likely directing attention to forex fluctuations and bond movements.

Traders will watch for any impromptu Bank of Japan announcements or yen interventions. This light schedule could heighten sensitivity to global news, including U.S. developments, potentially extending recent stock momentum.

Other Economic Notes

Oil prices climbing above $90 per barrel due to Middle East unrest elevate stagflation concerns for Japan, merging imported inflation with yen depreciation. Prime Minister Sanae Takaichi's views on monetary policy are under review, as her reservations about rate increases may shape responses to energy disruptions. Recent robust wage figures suggest potential for improved consumption, yet ongoing spending shortfalls moderate expectations.