Japan Macro Daily(Beta Mode)

Yen Recovers on BoJ Focus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,700.39 | -0.09% |

| USD/JPY | 158.98 | -0.37% |

| EUR/JPY | 183.46 | +0.55% |

| GBP/JPY | 212.37 | +0.47% |

| Gold | 5,007.90 | +0.28% |

| Brent Crude | 103.56 | +3.34% |

| Bitcoin | 74,560.31 | -0.40% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

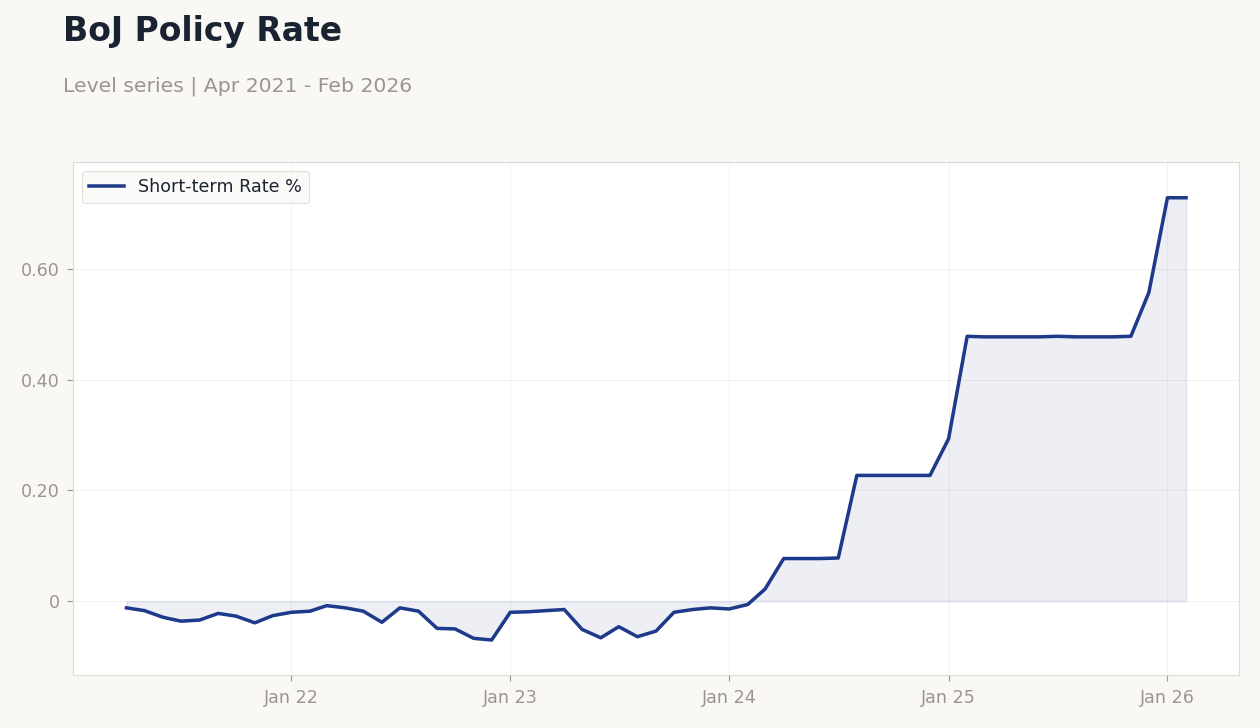

BoJ Policy Rate | Type: macro_line | Short-term Rate %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

BoJ Policy Rate | Type: macro_line | Short-term Rate %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | -1,152,700m | -483,200m | 15:50 |

| Exports Year-over-Year | 16.80 | 1.60 | 15:50 |

| Wednesday (2026-03-18) | |||

| Machinery Orders Month-over-Month | 19.10 | -9.60 | 15:50 |

| Machinery Orders Year-over-Year | 16.80 | 10.50 | 15:50 |

| BoJ Gov Ueda Speech | - | - | 18:30 |

| BoJ Interest Rate Decision | 0.75 | 0.75 | 19:00 |

- Japanese yen strengthened against USD amid anticipation of BoJ rate decision, with USD/JPY down 0.37% to 158.98.

- Nikkei 225 dipped 0.09% to 53,700.39, while JGB 10Y yield fell sharply by 5.80% to 2.11%.

- Oil surge from geopolitical tensions pressures Japan's economy, imperiling tourism's yen support.

Yesterday's Recap

Japanese markets exhibited muted activity on March 16 with no major data releases, allowing focus to shift to global influences. The Nikkei 225 closed slightly lower at 53,700.39, down 0.09%, as investors weighed yen strength against export competitiveness. USD/JPY declined 0.37% to 158.98, reflecting a yen recovery driven by safe-haven flows amid rising oil prices.

EUR/JPY and GBP/JPY rose 0.55% to 183.46 and 0.47% to 212.37 respectively, buoyed by broader currency dynamics. JGB yields diverged, with the 10Y dropping 5.80% to 2.11% on policy normalization bets, while the 2Y held steady at 0.73%. Brent crude surged 3.34% to 103.56, exacerbating inflation concerns for import-dependent Japan.

Overall, equity weakness contrasted with bond market relief, setting a cautious tone ahead of upcoming BoJ events.

The Day Ahead

Today's calendar features high-impact Trade Balance data at 15:50 ET, with consensus expecting a narrower deficit of -483.2 billion yen versus the previous -1.1527 trillion yen. Medium-impact Exports YoY follows at the same time, forecasted at 1.6% compared to prior 16.8%, potentially signaling export slowdown amid global demand shifts. Tomorrow brings Machinery Orders MoM at 15:50 ET, consensus -9.6% after 19.1%, alongside YoY at 10.5% from 16.8%, highlighting manufacturing trends.

BoJ Governor Ueda's speech at 18:30 ET could provide policy clues, followed by the high-impact BoJ Interest Rate Decision at 19:00 ET, with consensus holding at 0.73%. These events may influence yen volatility and JGB yields. Markets anticipate cautious BoJ rhetoric amid inflation pressures.

Other Economic Notes

Broader themes underscore Japan's vulnerability to external shocks, particularly war-fueled oil surges that threaten tourism's role in supporting the yen. Rising energy costs from Iran conflict inflation pose a dilemma for the BoJ, balancing growth risks with price stability. Subdued wage growth and manufacturing weakness, as seen in prior data, complicate policy normalization efforts.