Japan Macro Daily(Beta Mode)

BoJ Holds Amid Iran Tensions, Yields Fall

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,372.53 | -3.38% |

| USD/JPY | 159.22 | -0.36% |

| EUR/JPY | 184.25 | +0.59% |

| GBP/JPY | 212.44 | +0.24% |

| Gold | 4,492.00 | -2.36% |

| Brent Crude | 106.77 | -1.73% |

| Bitcoin | 70,534.80 | +0.89% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

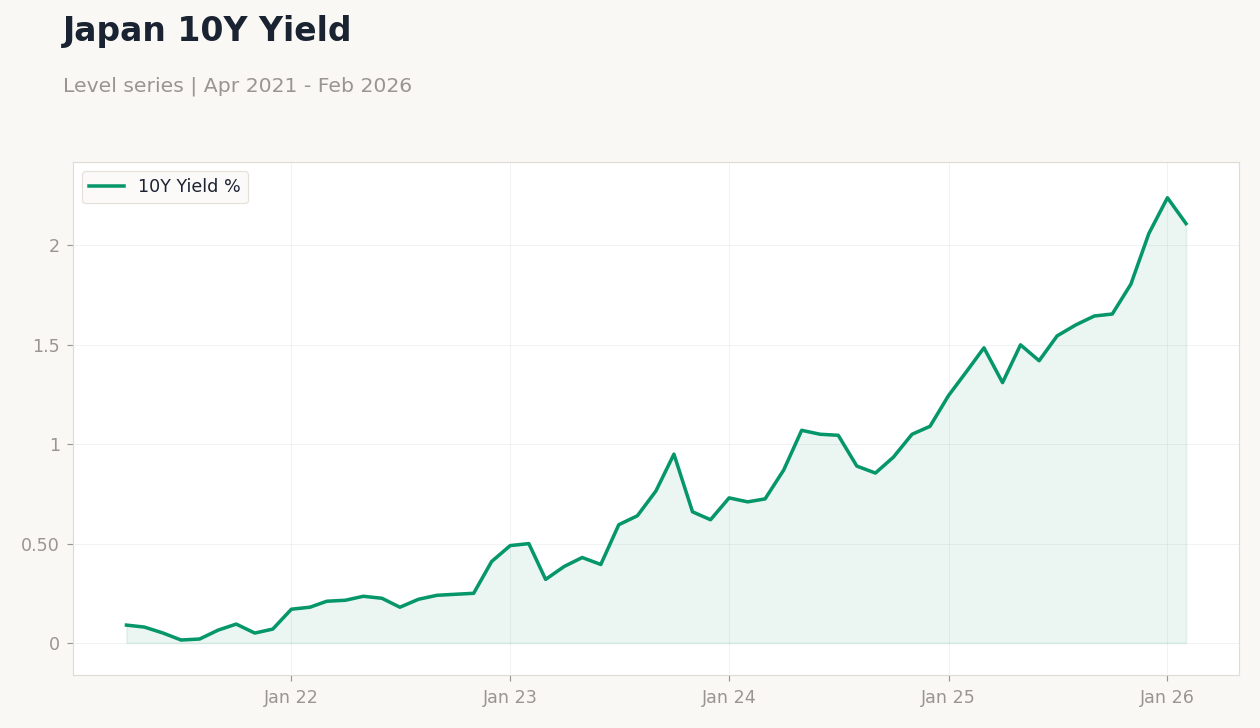

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | -1,163,500m | -483,200m | 57,300m |

| Exports Year-over-Year | 16.80 | 1.60 | 4.20 |

| Machinery Orders Month-over-Month | 19.10 | -9.60 | -5.50 |

| Machinery Orders Year-over-Year | 16.80 | 10.50 | 13.70 |

| BoJ Gov Ueda Speech | - | - | - |

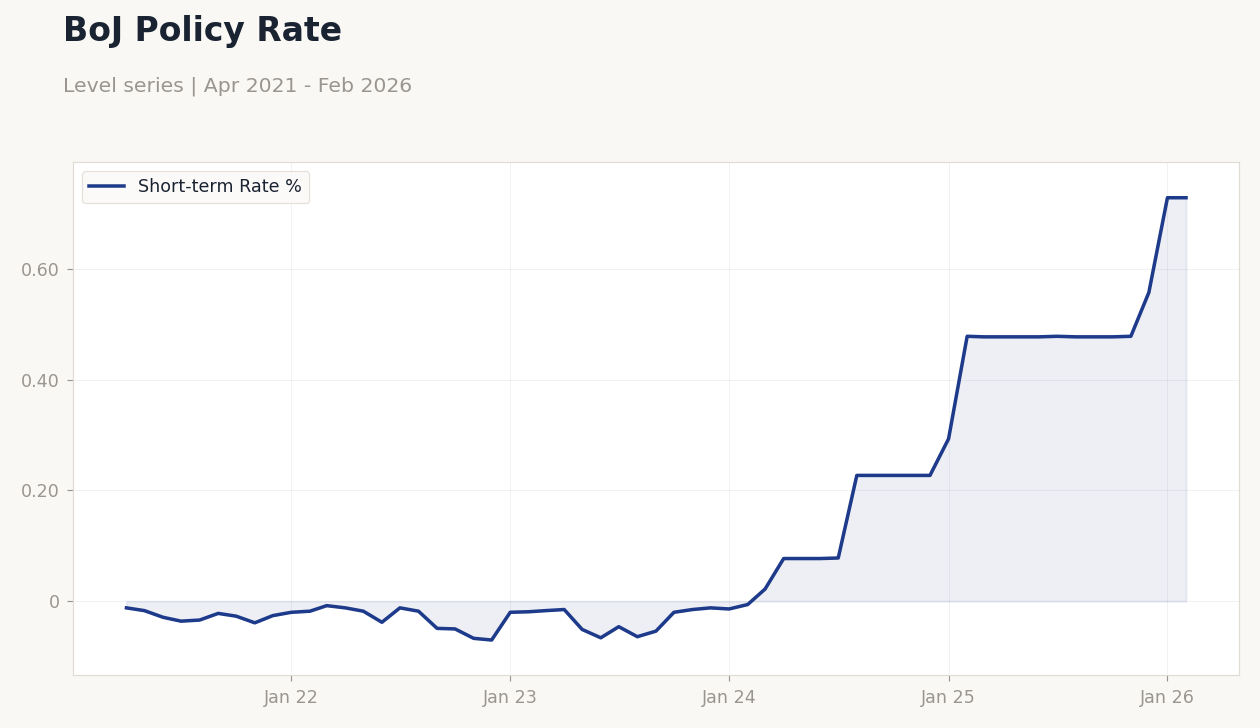

| BoJ Interest Rate Decision | 0.75 | 0.75 | 0.75 |

BoJ Policy Rate | Type: macro_line | Short-term Rate %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

BoJ Policy Rate | Type: macro_line | Short-term Rate %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BoJ kept rates at 0.75% amid global uncertainty, with Ueda's speech highlighting data-dependent policy.

- Trade balance posted surprise surplus of ¥57.3B, exports up 4.2% YoY; machinery orders fell less than expected.

- Nikkei dropped 3.38% on risk aversion; 10Y JGB yield fell 5.80% as Iran tensions spurred safe-haven bids.

Yesterday's Recap

Japan's trade balance surprised with a ¥57.3 billion surplus, far exceeding the consensus forecast of a ¥483.2 billion deficit and reversing the previous ¥1.1635 trillion shortfall, bolstered by exports rising 4.2% year-over-year against expectations of 1.6%. Machinery orders declined 5.5% month-over-month, outperforming the anticipated 9.6% drop, while year-over-year growth reached 13.7% versus the 10.5% consensus, indicating sustained capital spending despite challenges. The Bank of Japan maintained its policy rate at 0.75%, matching expectations, as Governor Ueda's speech stressed vigilance on global risks without introducing fresh hawkish signals.

Equities tumbled, with the Nikkei 225 closing down 3.38% at 53,372.53, driven by geopolitical concerns. Currency shifts were subdued: USD/JPY fell 0.36% to 159.22, while EUR/JPY rose 0.59% to 184.25 and GBP/JPY gained 0.24% to 212.44, reflecting post-decision yen fluctuations. JGB yields declined notably, with the 10-year yield dropping 5.80% to 2.11% and the 2-year unchanged at 0.73%, as the Iran crisis fueled safe-haven demand.

These outcomes highlight Japan's export resilience amid external pressures clouding the economic outlook.

The Day Ahead

No significant Japanese economic releases are slated for today, providing space for markets to process the BoJ's rate hold and recent trade data. Focus may turn to any additional BoJ remarks on the decision and normalization prospects. Yen movements could respond to international developments, especially if shifts in major currencies affect carry trades.

Nikkei futures might see attempts at recovery from the prior session's decline, influenced by exporter outlooks. With no events tomorrow, emphasis stays on how recent figures shape BoJ expectations, though external factors like Middle East news could drive volatility in bonds and currencies.

Other Economic Notes

Japan's exports demonstrate recovery momentum, with the trade surplus underscoring strength against global slowdowns, yet reliance on key markets poses risks. Pressures in the banking sector persist, as Aozora Bank and Toho Bank face challenges from rate uncertainty and slower regional lending. (cont...)