Japan Macro Daily(Beta Mode)

Nikkei Plunges on Stagflation Fears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,372.53 | -3.38% |

| USD/JPY | 159.22 | +0.82% |

| EUR/JPY | 184.25 | +0.78% |

| GBP/JPY | 212.44 | +0.20% |

| Gold | 4,574.90 | -0.56% |

| Brent Crude | 106.41 | -2.06% |

| Bitcoin | 70,276.18 | -0.35% |

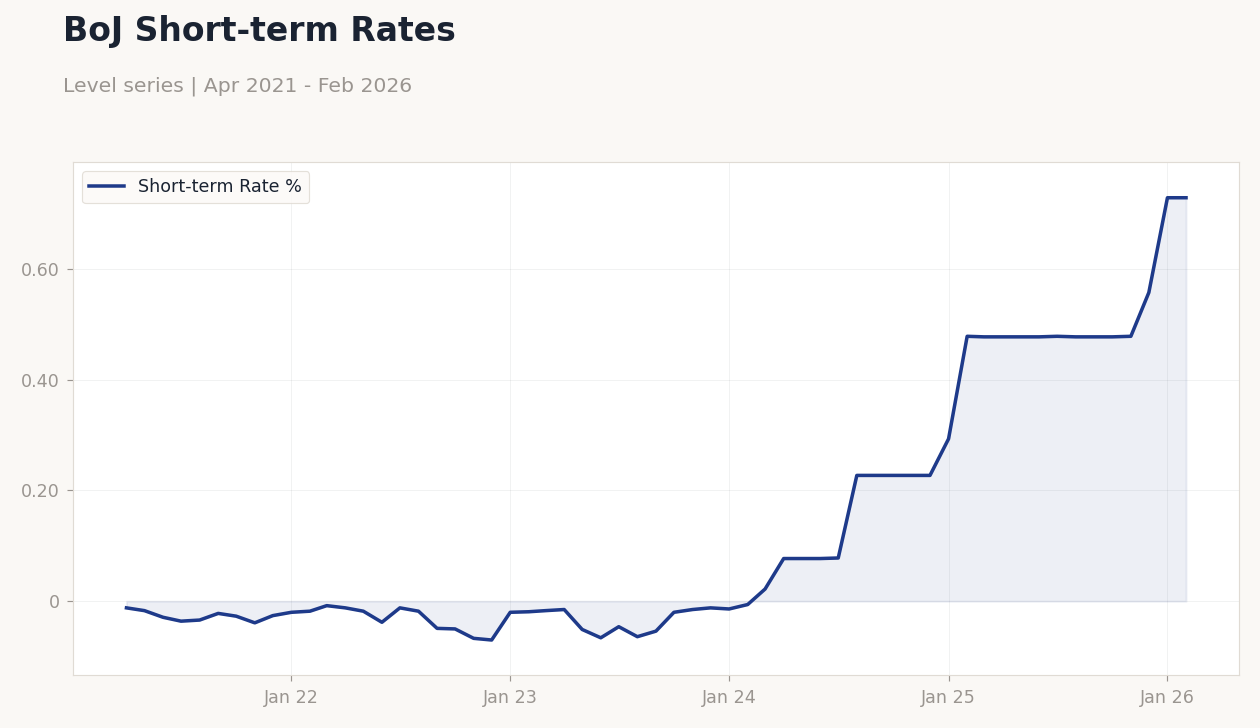

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

BoJ Short-term Rates | Type: macro_line | Short-term Rate %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

BoJ Short-term Rates | Type: macro_line | Short-term Rate %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Monday (2026-03-23) | |||

| Inflation Rate Year-over-Year | 1.50 | - | 19:30 |

| Core Inflation Rate Year-over-Year | 2 | 1.70 | 19:30 |

| Tuesday (2026-03-24) | |||

| S&P Global Manufacturing PMI Flash | 53 | 52.80 | 20:30 |

| S&P Global Services PMI Flash | 53.80 | - | 20:30 |

| BoJ Monetary Policy Meeting Minutes | - | - | 19:50 |

- Nikkei 225 tumbled 3.38% to 53,372.53 amid oil-yen squeeze and stagflation risks.

- JGB 10-year yield fell 5.80% to 2.11%, signaling bets on delayed BoJ hikes.

- USD/JPY climbed 0.82% to 159.22, pressuring importers amid currency volatility.

Yesterday's Recap

Japanese markets saw sharp declines yesterday, with the Nikkei 225 dropping 3.38% to 53,372.53, fueled by stagflation concerns from rising oil prices and a depreciating yen. The USD/JPY pair advanced 0.82% to 159.22, heightening import costs and dragging on equities, while EUR/JPY rose 0.78% to 184.25 and GBP/JPY gained 0.20% to 212.44. JGB yields declined, with the 10-year yield falling 5.80% to 2.11% and the 2-year yield unchanged at 0.73%, as markets priced in slower BoJ normalization amid uncertainty.

No significant data was released, but sentiment weakened on reports of oil-yen pressures, leading to risk-off trading. Gold slipped 0.56% to 4,574.90, Brent crude dropped 2.06% to 106.41, providing minor relief but failing to counter yen-related strains on importers. Bitcoin fell 0.35% to 70,276.18, aligning with global caution.

The session underscored Japan's export-driven economy's exposure to volatile currencies and commodities.

The Day Ahead

Attention turns to Japan's inflation figures on March 23, with the year-over-year inflation rate set for 19:30 ET, building on a previous 1.5% reading and potentially highlighting ongoing price pressures from oil surges. Core inflation, due at the same time with consensus at 1.7% versus prior 2.0%, may shape BoJ expectations if it misses estimates. The S&P Global Manufacturing PMI flash arrives at 20:30 ET on March 23, with consensus at 52.8 against previous 53.0, shedding light on industrial activity.

Services PMI flash, also at 20:30 ET, has no consensus but follows prior 53.8, key for assessing service-sector strength. BoJ Monetary Policy Meeting Minutes are scheduled for March 24 at 19:50 ET, possibly detailing discussions on rate trajectories. March 22 has no events, directing focus to these releases for cues on yen and stock movements.

Other Economic Notes

Japan's economy contends with rising stagflation threats as high oil prices intersect with yen weakness, inflating import expenses and curbing consumer outlays. Retail players like ABC-Mart and Workman face challenges from decelerating spending and exchange-rate swings, hurting share prices. Regional lenders including Mebuki Financial and Toho Bank navigate uncertainties around rate hikes, affecting lending volumes and margins in a slowing economy.