Japan Macro Daily(Beta Mode)

Inflation Cools, Yen Pressured

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,749.62 | +2.87% |

| USD/JPY | 159.39 | +0.42% |

| EUR/JPY | 184.34 | +0.22% |

| GBP/JPY | 213.01 | +0.04% |

| Gold | 4,503.30 | +2.36% |

| Brent Crude | 98.05 | -6.16% |

| Bitcoin | 71,005.37 | +0.69% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

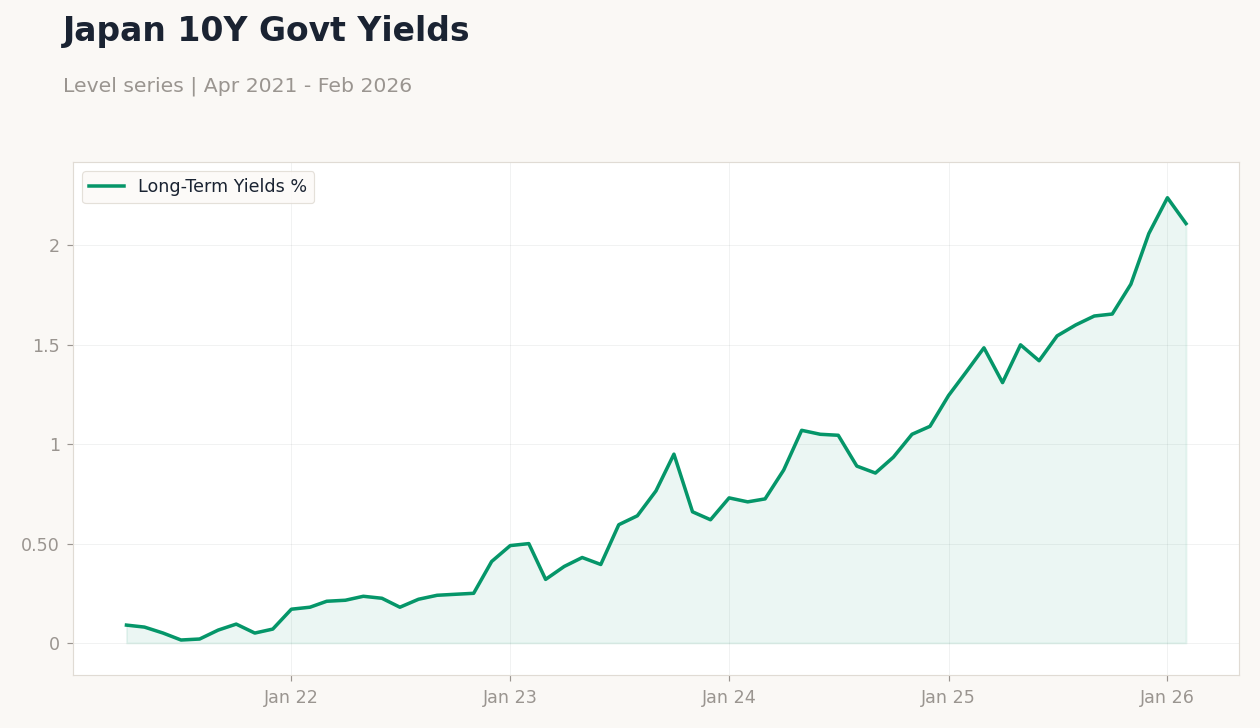

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.50 | - | 1.30 |

| Core Inflation Rate Year-over-Year | 2 | 1.70 | 1.60 |

| S&P Global Manufacturing PMI Flash | 53 | 52.80 | 51.40 |

| S&P Global Services PMI Flash | 53.80 | - | 52.80 |

| BoJ Monetary Policy Meeting Minutes | - | - | - |

BoJ Short-Term Rates | Type: macro_line | Short-Term Interest Rates %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

BoJ Short-Term Rates | Type: macro_line | Short-Term Interest Rates %: 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Sunday (2026-03-29) | |||

| BoJ Summary of Opinions | - | - | 15:50 |

- Japan's inflation eased to 1.3% YoY, missing expectations and complicating BoJ's rate path amid persistent yen weakness.

- Flash PMIs showed manufacturing weakening to 51.4 and services slowdown to 52.8, signaling softening economic momentum.

- Nikkei rallied 2.87% on global risk appetite, while 10Y JGB yield fell 5.8% as markets digest BoJ minutes.

Yesterday's Recap

Japan's inflation data disappointed, with headline YoY rate dropping to 1.3% from 1.5% prior, underscoring cooling price pressures. Core inflation printed at 1.6%, below the 1.7% consensus and previous 2.0%, raising questions on BoJ's 2% target sustainability. S&P Global Manufacturing PMI flash fell to 51.4 against 52.8 expected, indicating weakening but still in expansion, driven by export softness, while Services PMI eased to 52.8 from 53.8.

The BoJ released Monetary Policy Meeting Minutes, revealing deliberations on gradual normalization without specifying immediate hikes. Markets reacted with Nikkei 225 surging 2.87% to 53,749.62, buoyed by tech gains and a weaker yen. USD/JPY climbed 0.42% to 159.39, reflecting persistent yen depreciation despite hawkish signals, as 10Y JGB yield dropped 5.8% to 2.11% on tempered rate expectations.

EUR/JPY and GBP/JPY saw modest gains of 0.22% and 0.04%, respectively, amid mixed global cues.

The Day Ahead

Today's calendar is light with no major Japanese data releases, allowing markets to focus on digesting yesterday's inflation miss and BoJ minutes. Attention shifts to broader Asia-Pacific sentiment, potentially influenced by any spillover from US or European trading sessions. The upcoming BoJ Summary of Opinions on March 29 could provide further clarity on policy directions, though it's not immediate.

Investors will monitor yen dynamics closely, given recent weakness against the dollar. No significant events are scheduled for tomorrow, keeping the focus on global macro developments.

Other Economic Notes

Broader themes highlight Japan's struggle with disinflation, as core CPI dipped below the BoJ's target, complicating communication on potential rate hikes. Manufacturing faces rising input costs from Middle East tensions, exacerbating expense surges and pressuring profit margins. Regional banks like Mizuho, Shiga, Suruga, Toho, and Chiba are under strain from shifting rate environments, with stocks facing volatility amid global banking uncertainties.