Japan Macro Daily(Beta Mode)

Yen Hits 160, Yields Tumble

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,373.07 | -0.43% |

| USD/JPY | 160.15 | +0.28% |

| EUR/JPY | 184.25 | +0.01% |

| GBP/JPY | 212.48 | -0.23% |

| Gold | 4,524.30 | +3.40% |

| Brent Crude | 105.32 | -2.49% |

| Bitcoin | 66,537.93 | +0.33% |

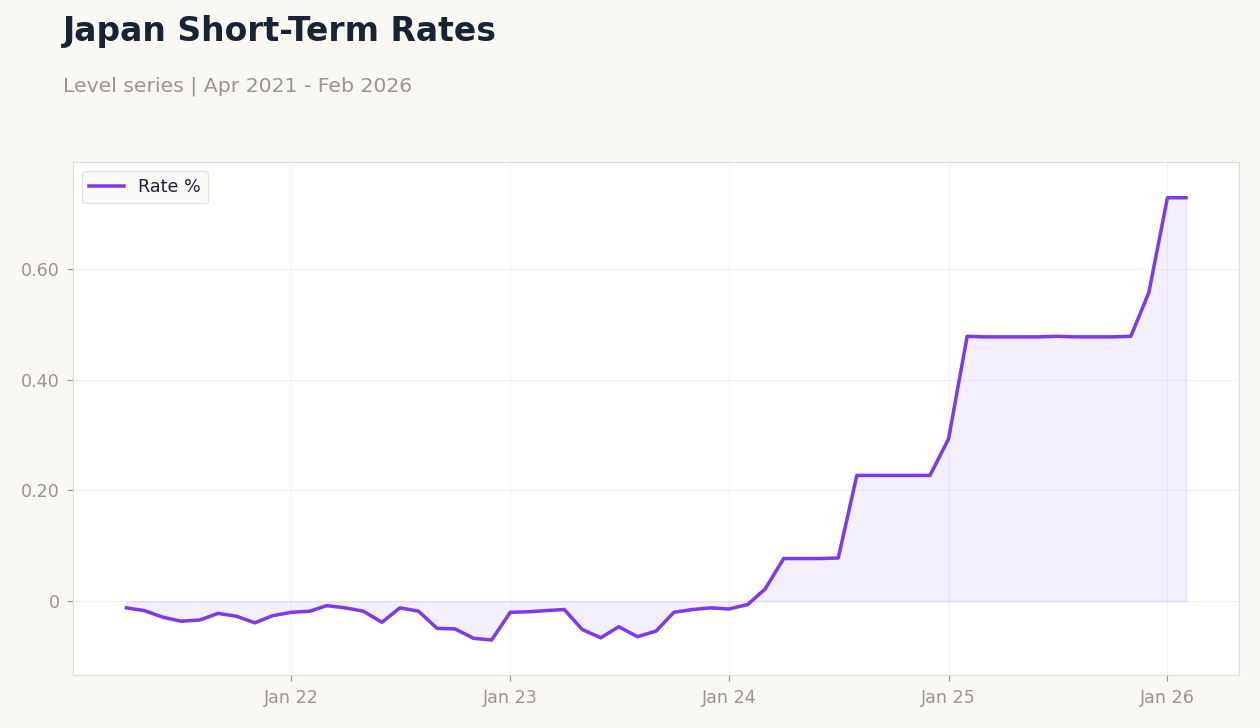

| Japan 2Y Govt Yield | 0.73% | +0.00% |

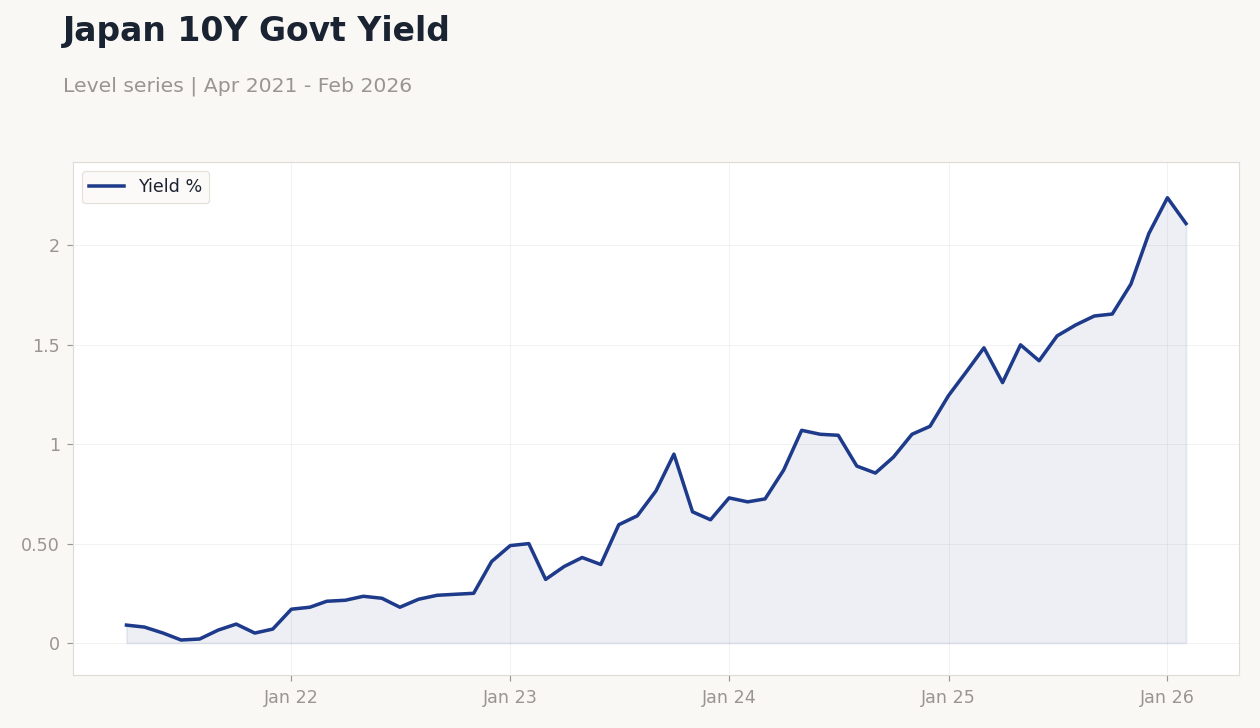

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan 10Y Govt Yield | Type: macro_line | Yield %: 2.11 (2026-02-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.11

Japan 10Y Govt Yield | Type: macro_line | Yield %: 2.11 (2026-02-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.11

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoJ Summary of Opinions | - | - | 19:50 |

| Monday (2026-03-30) | |||

| Housing Starts Year-over-Year | -0.40 | -4.70 | 01:00 |

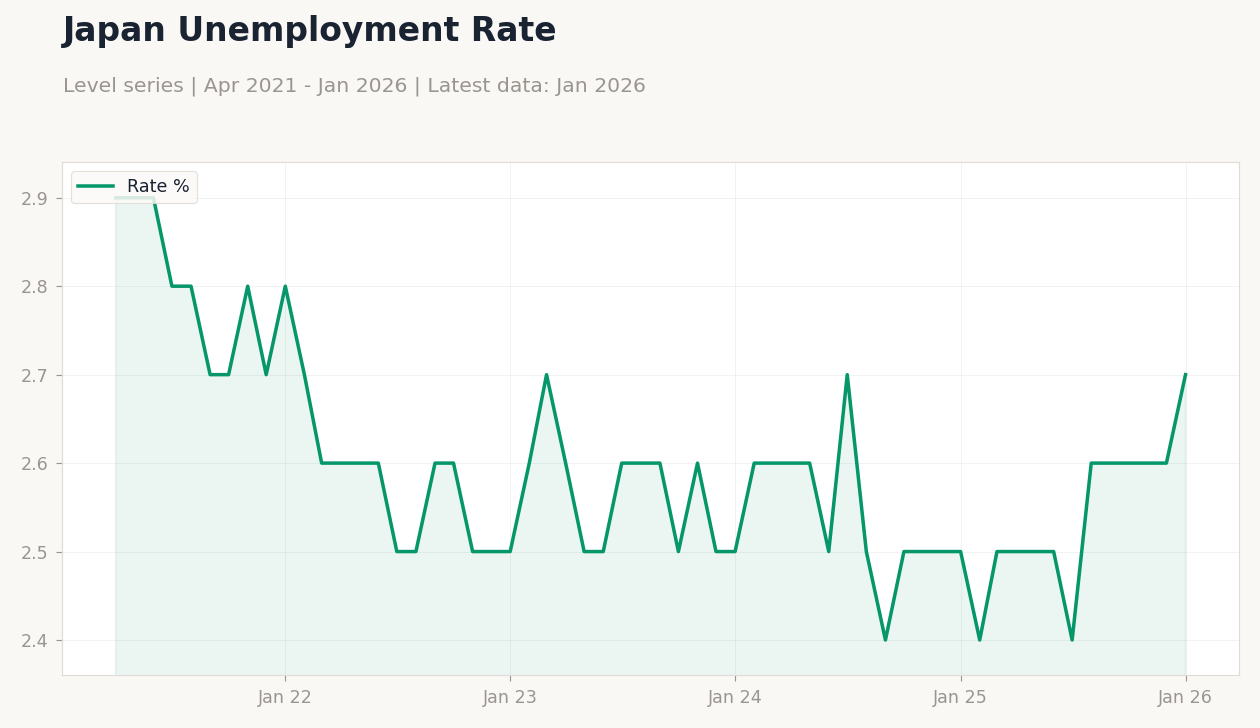

| Headline Unemployment Rate | 2.70 | 2.70 | 19:30 |

| Industrial Production Month-over-Month Preliminary | 4.30 | -2.10 | 19:50 |

| Retail Sales Year-over-Year | 1.80 | 0.80 | 19:50 |

| Tuesday (2026-03-31) | |||

| Tankan Large Manufacturers Index | 15 | 16 | 19:50 |

- Yen weakens to 160 against dollar amid global risk shifts, pressuring exporters while boosting Nikkei marginally despite daily dip.

- JGB 10Y yield drops sharply to 2.11%, reflecting reduced policy tightening bets ahead of BoJ Summary of Opinions.

- Industrial data and Tankan survey loom, with consensus pointing to softening growth signals amid persistent deflation risks.

Yesterday's Recap

Japanese markets closed mixed on March 28 with no major data releases, as the Nikkei 225 fell 0.43% to 53,373.07, driven by profit-taking in tech sectors amid global volatility. The USD/JPY pair climbed 0.28% to 160.15, marking the yen's weakest level since July 2024 and fueling intervention speculation from authorities. EUR/JPY edged up 0.01% to 184.25, while GBP/JPY declined 0.23% to 212.48, reflecting broader currency pressures from dollar strength.

Japan 10Y government bond yields plunged 5.80% to 2.11%, signaling investor flight to safety amid Middle East tensions, with 2Y yields holding steady at 0.73%. Gold surged 3.40% to 4,524.30, benefiting Japanese importers, but Brent crude dropped 2.49% to 105.32, easing energy cost concerns for manufacturers. Bitcoin rose 0.33% to 66,537.93, adding to risk asset fluctuations that influenced yen dynamics.

Overall, the absence of economic prints shifted focus to global cues, keeping JGB demand elevated.

The Day Ahead

The BoJ Summary of Opinions releases at 19:50 ET on March 29, offering insights into policymakers' views on inflation and normalization, potentially swaying yen and yield expectations. On March 30, Housing Starts YoY is due at 01:00 ET with consensus at -4.7% versus previous -0.4%, highlighting construction sector weakness amid demographic pressures. Headline Unemployment Rate follows at 19:30 ET, expected steady at 2.7%, underscoring labor market resilience despite growth headwinds.

Industrial Production MoM Preliminary at 19:50 ET forecasts -2.1% from 4.3%, signaling manufacturing slowdown, while Retail Sales YoY at the same time eyes 0.8% from 1.8%, reflecting consumer spending caution. The Tankan Large Manufacturers Index on March 31 at 19:50 ET, with consensus at 16 from 15, carries high impact for gauging business sentiment and BoJ policy signals.

Other Economic Notes

Japan's economy grapples with deflationary pressures, as core CPI slowed below the BoJ's 2% target in February, complicating rate hike paths amid wage-price cycle uncertainties. (cont...)