Japan Macro Daily(Beta Mode)

Yen Strengthens, Yields Drop

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,373.07 | -0.43% |

| USD/JPY | 159.73 | -0.32% |

| EUR/JPY | 183.09 | -0.56% |

| GBP/JPY | 210.47 | -0.77% |

| Gold | 4,533.70 | +0.93% |

| Brent Crude | 108.80 | -3.35% |

| Bitcoin | 66,617.78 | +1.01% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

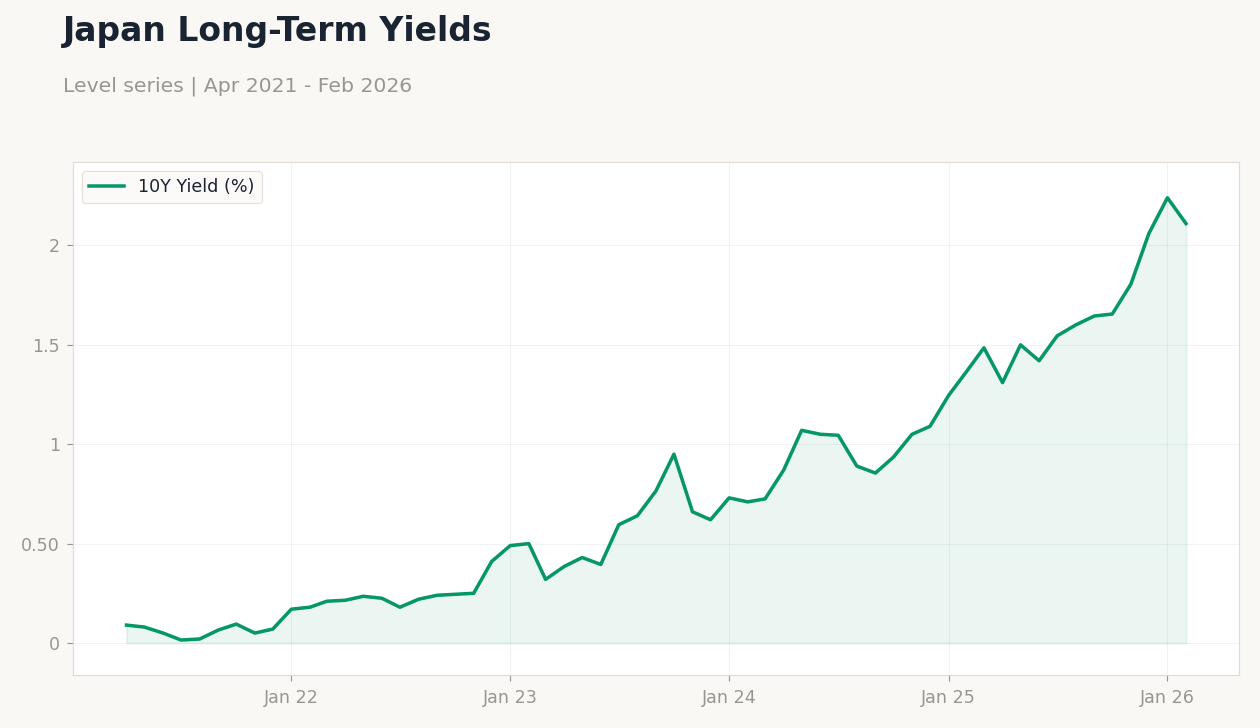

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

BoJ Short-Term Policy Rates | Type: macro_line | Short-Term Rate (%): 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

BoJ Short-Term Policy Rates | Type: macro_line | Short-Term Rate (%): 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(6pt): -0.012,-0.038,-0.064,0.227,0.557,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 2.70 | 2.70 | 15:30 |

| Industrial Production Month-over-Month Preliminary | 4.30 | -2.10 | 15:50 |

| Retail Sales Year-over-Year | 1.80 | 0.80 | 15:50 |

| Tuesday (2026-03-31) | |||

| Tankan Large Manufacturers Index | 15 | 16 | 15:50 |

- Nikkei falls 0.43% on global risk aversion, yen gains against dollar.

- JGB 10Y yield declines 5.80% amid safe-haven buying.

- Key data releases today could shape BoJ policy outlook.

Yesterday's Recap

Japanese markets ended lower on March 29, with the Nikkei 225 dropping 0.43% to 53,373.07, driven by exporter pressures and worldwide stock weakness. The USD/JPY rate fell 0.32% to 159.73, indicating yen strength from safe-haven demand linked to Middle East conflicts. EUR/JPY decreased 0.56% to 183.09, and GBP/JPY slipped 0.77% to 210.47.

Japan 10Y government bond yields dropped 5.80% to 2.11%, reflecting investor wariness on inflation, while the 2Y yield stayed flat at 0.73%. Gold climbed 0.93% to 4,533.70 on haven appeal, but Brent crude fell 3.35% to 108.80 due to supply dynamics. Bitcoin rose 1.01% to 66,617.78, diverging from risk assets.

With no significant data out, attention centered on geopolitical news.

The Day Ahead

March 30 features important Japanese metrics, beginning with the headline unemployment rate at 15:30 ET, expected steady at 2.7% given labor resilience. At 15:50 ET, preliminary industrial production month-over-month for February is forecast at -2.1% from 4.3% prior, hinting at manufacturing softness. Retail sales year-over-year, also at 15:50 ET, may slow to 0.8% from 1.8%, showing consumer restraint.

On March 31, the Tankan large manufacturers index at 15:50 ET is projected to edge up to 16 from 15, providing business sentiment and investment clues. These figures may affect yen movements and JGB yields before BoJ reviews. Surprises could spur talks on faster policy shifts.

Other Economic Notes

Japan's economy grapples with global headwinds, including Iran war effects on energy costs and logistics. Reforms in corporate governance are drawing overseas funds to Japanese stocks, as noted in advice for Australian investors seeking diversification in sectors like manufacturing. Wage trends are key, with union successes possibly aiding spending, yet tempered by inflation easing below goals.

Global Macro News

Worldwide factors impact Japan, with the dollar rising on Iran war escalation, nearing recent USD/JPY peaks and hurting exporters. The yen hit 160 per dollar on March 27, its weakest since July 2024, raising intervention concerns. BOJ officials lean hawkish, advocating rate hikes amid ongoing inflation and wage momentum, though core CPI fell below 2% in February.

(cont...)