Japan Macro Daily(Beta Mode)

Nikkei Sinks, Yen Firms on Warnings

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 51,885.85 | -2.79% |

| USD/JPY | 158.73 | -0.69% |

| EUR/JPY | 183.41 | +0.16% |

| GBP/JPY | 209.86 | -0.32% |

| Gold | 4,696.80 | +3.77% |

| Brent Crude | 103.33 | -8.38% |

| Bitcoin | 68,173.80 | +2.22% |

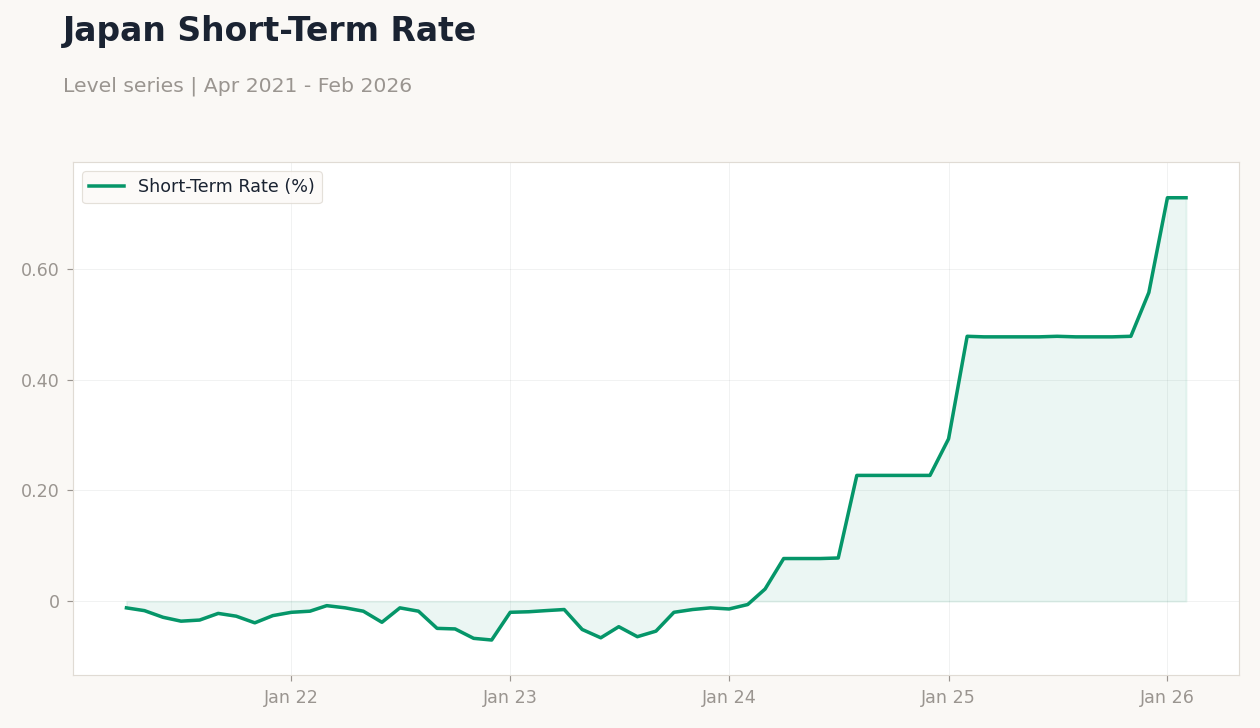

| Japan 2Y Govt Yield | 0.73% | +0.00% |

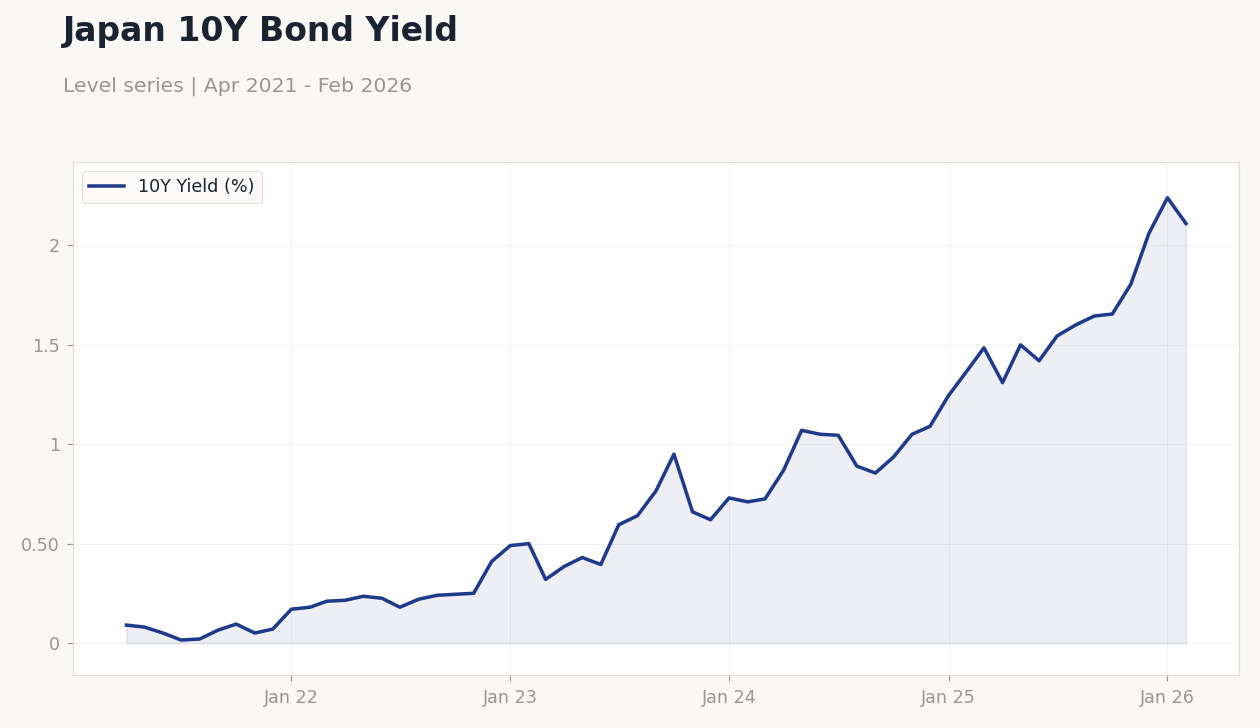

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

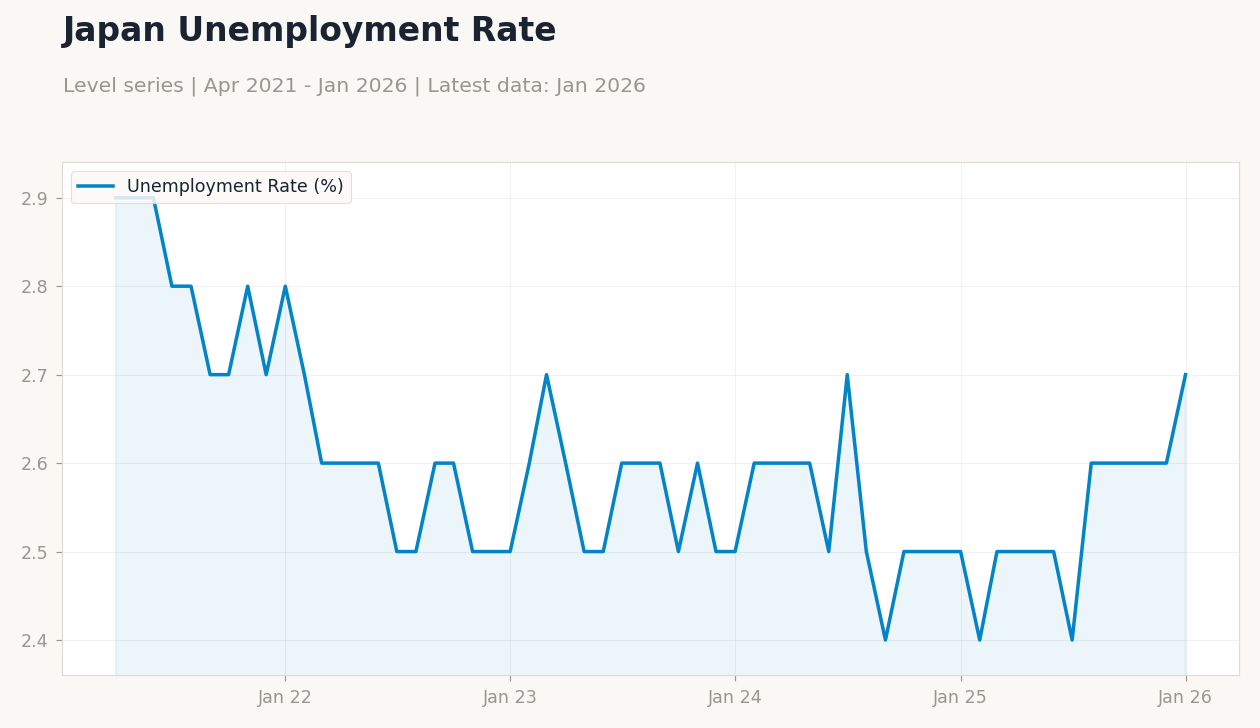

| Headline Unemployment Rate | 2.70 | 2.70 | 2.60 |

| Industrial Production Month-over-Month Preliminary | 4.30 | -2.10 | -2.10 |

| Retail Sales Year-over-Year | 1.80 | 0.80 | -0.20 |

| Housing Starts Year-over-Year | -0.40 | -4.70 | -4.90 |

Japan 10Y Bond Yield | Type: macro_line | 10Y Yield (%): 2.11 (2026-02-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.11

Japan 10Y Bond Yield | Type: macro_line | 10Y Yield (%): 2.11 (2026-02-01) | Range: 0.015–2.24 | Trend(6pt): 0.09,0.225,0.64,0.935,2.06,2.11

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tankan Large Manufacturers Index | 15 | 16 | 19:50 |

| Monday (2026-04-06) | |||

| Household Spending Month-over-Month | -2.50 | - | 19:30 |

| Household Spending Year-over-Year | -1 | - | 19:30 |

| Tuesday (2026-04-07) | |||

| Current Account Balance | 941,600m | - | 19:50 |

- Japanese data showed mixed signals with unemployment dipping to 2.6% but retail sales contracting -0.2% YoY, fueling recession concerns.

- Nikkei 225 plunged -2.79% amid global risk-off, while USD/JPY fell -0.69% as BoJ ramped up yen defense rhetoric.

- JGB 10Y yield dropped -5.80% to 2.11%, reflecting safe-haven bids and policy normalization uncertainties.

Yesterday's Recap

Japanese economic data released on March 30 painted a softening picture, with headline unemployment rate improving to 2.6% from 2.7%, beating consensus and signaling labor market resilience. However, industrial production fell -2.1% MoM as expected, indicating ongoing manufacturing weakness amid global demand slowdowns. Retail sales disappointed sharply at -0.2% YoY versus consensus 0.8%, highlighting consumer caution driven by persistent inflation pressures.

Housing starts declined -4.9% YoY, slightly worse than the -4.7% forecast, underscoring construction sector strains from higher material costs. Markets reacted negatively, with the Nikkei 225 tumbling -2.79% to 51,885.85 on recession fears and oil price volatility. The yen strengthened, pushing USD/JPY down -0.69% to 158.73, supported by BoJ intervention threats.

JGB yields eased, with the 10Y dropping to 2.11% amid safe-haven flows, while the 2Y held steady at 0.73%.

The Day Ahead

The Tankan Large Manufacturers Index for Q1 releases at 19:50 JST on March 31, with consensus at 16 versus previous 15, potentially signaling improved business sentiment amid export recoveries. A stronger-than-expected reading could bolster BoJ hike expectations, lifting JGB yields and equities. Looking further, household spending data for both MoM and YoY arrives on April 6, offering insights into consumption trends without firm consensus yet.

Current account balance follows on April 7, critical for yen dynamics given trade surplus implications. Markets will watch for any unscheduled BoJ statements on yen volatility. Overall, Tankan headlines today's focus, with implications for policy normalization paths.

Other Economic Notes

Broader Japanese economic themes revolve around deflationary risks, as the latest CPI YoY stands at -0.50% from June 2021 data, complicating BoJ efforts to achieve stable 2% inflation. Energy market instability, with Brent crude down -8.38% to 103.33 amid Gulf tensions, pressures import-dependent sectors like manufacturing. Fiscal consolidation remains key, with PM signals avoiding new stimulus to manage debt, potentially weighing on growth recovery.