Japan Macro Daily(Beta Mode)

Nikkei Surges, Yen Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 53,739.68 | +5.24% |

| USD/JPY | 159.56 | +0.55% |

| EUR/JPY | 183.98 | +0.05% |

| GBP/JPY | 211.04 | -0.00% |

| Gold | 4,696.50 | -1.81% |

| Brent Crude | 108.88 | +7.63% |

| Bitcoin | 66,936.65 | -1.68% |

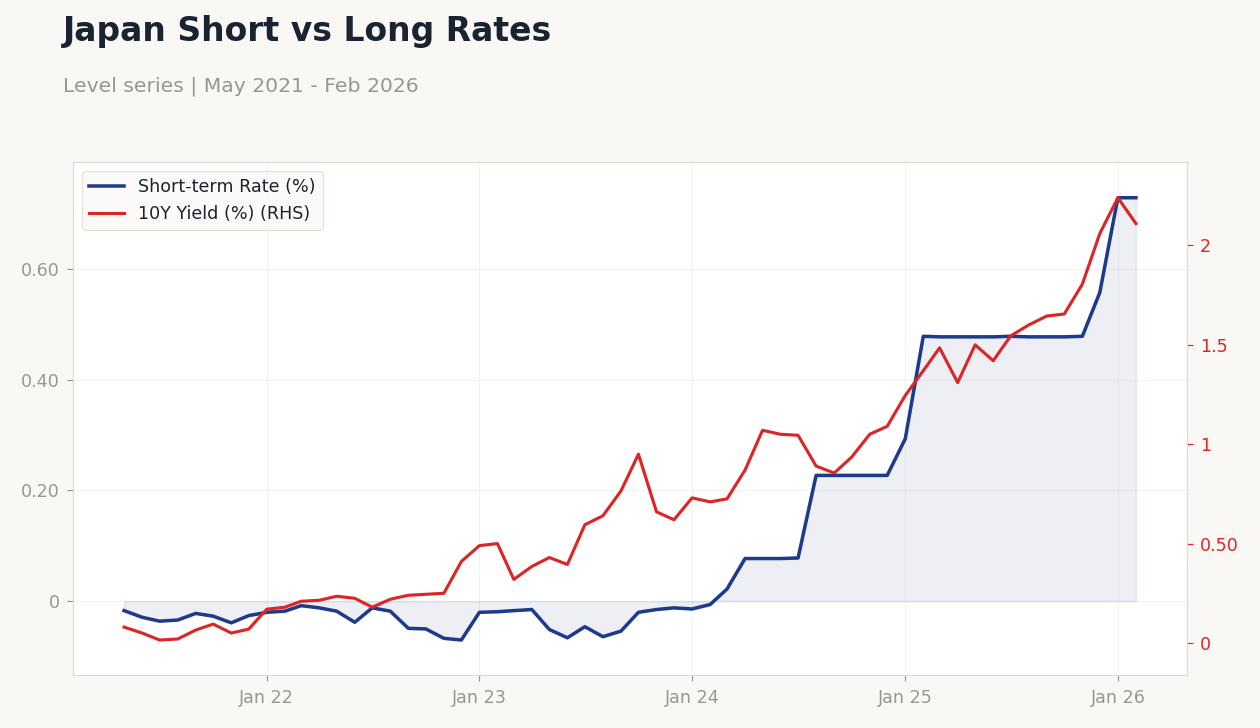

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.11% | -5.80% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

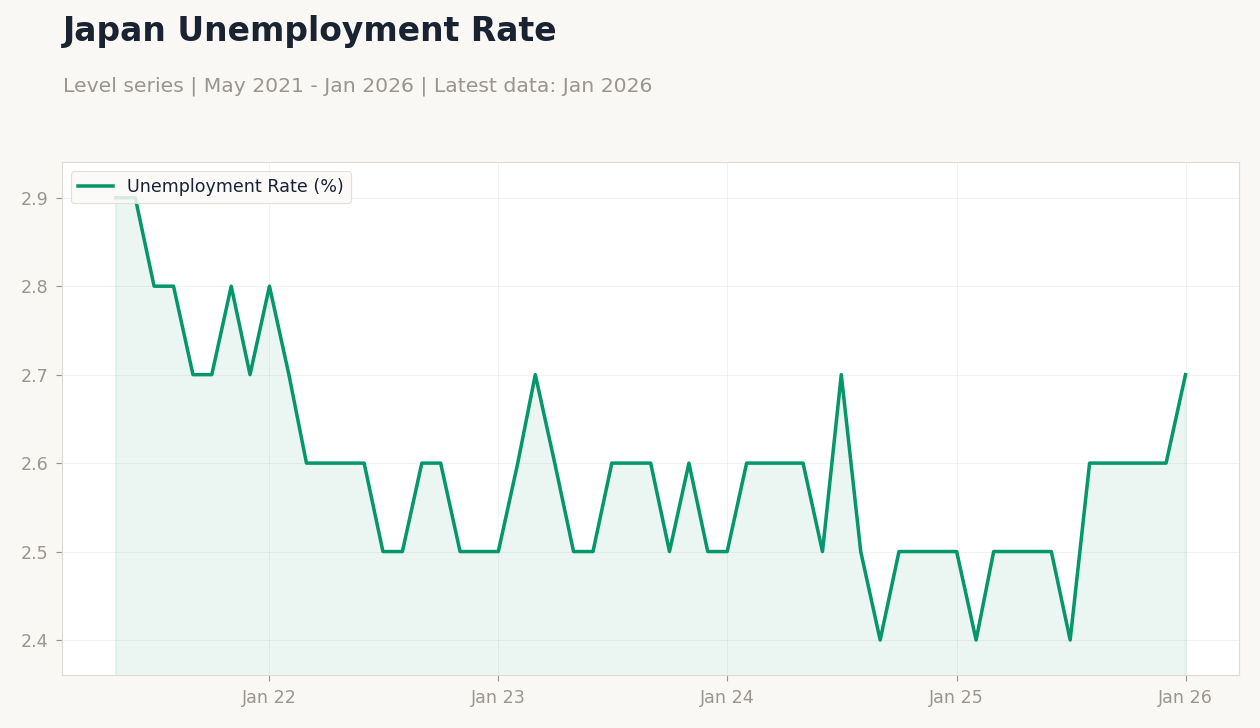

| Headline Unemployment Rate | 2.70 | 2.70 | 2.60 |

| Industrial Production Month-over-Month Preliminary | 4.30 | -2.10 | -2.10 |

| Retail Sales Year-over-Year | 1.80 | 0.80 | -0.20 |

| Housing Starts Year-over-Year | -0.40 | -4.70 | -4.90 |

| Tankan Large Manufacturers Index | 15 | 16 | 17 |

Japan Short vs Long Rates | Type: macro_line | Short-term Rate (%): 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(5pt): -0.017,-0.012,-0.054,0.227,0.728 | 10Y Yield (%): 2.11 (2026-02-01) | Range: 0.015–2.24 | Trend(6pt): 0.08,0.18,0.765,1.05,2.24,2.11

Japan Short vs Long Rates | Type: macro_line | Short-term Rate (%): 0.728 (2026-02-01) | Range: -0.07–0.728 | Trend(5pt): -0.017,-0.012,-0.054,0.227,0.728 | 10Y Yield (%): 2.11 (2026-02-01) | Range: 0.015–2.24 | Trend(6pt): 0.08,0.18,0.765,1.05,2.24,2.11

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Nikkei 225 soared 5.24% to 53,739.68, driven by exporter gains amid yen depreciation.

- Tankan index hit 17, beating expectations and signaling manufacturing optimism despite soft retail sales.

- Stagflation warnings from Middle East tensions add to yen intervention threats and rate hike bets.

Yesterday's Recap

Japan's headline unemployment rate dropped to 2.6% as reported on March 30, 2026, beating consensus of 2.7% and indicating a tightening labor market that may bolster wage growth. Industrial production fell 2.1% month-over-month preliminary, matching consensus and reflecting supply chain issues and weak demand. Retail sales declined 0.2% year-over-year, missing consensus of 0.8% growth and underscoring consumer hesitancy amid cost pressures.

Housing starts weakened to -4.9% year-over-year, slightly below consensus of -4.7%, highlighting property sector struggles. The Tankan large manufacturers index rose to 17 on March 31, 2026, exceeding consensus of 16 and pointing to improved business sentiment from export rebounds. Markets responded strongly, with the Nikkei 225 up 5.24% to 53,739.68 on tech and auto advances, while the 10-year JGB yield declined 5.80% to 2.11% on safe-haven demand.

USD/JPY climbed 0.55% to 159.56, driven by dollar strength despite Japan's yen intervention warnings.

The Day Ahead

No major Japanese economic data is due today, April 2, 2026, leaving markets to process yesterday's releases and track yen movements. Focus may turn to global factors, such as Middle East developments impacting oil and inflation. Traders will monitor for Japanese official statements on currency weakness.

Asian equity trends could guide Nikkei futures. Tomorrow, April 3, 2026, also has no key events, suggesting a subdued period before possible April policy updates.

Other Economic Notes

Japan's economy faces stagflation risks from Middle East conflicts, as cautioned by a former Bank of Japan official, with potential energy cost spikes amid yen weakness. This contrasts with the latest CPI year-over-year at -0.50% as of June 2021. Tankan's upbeat manufacturing signal clashes with sluggish retail and production figures, revealing uneven sectoral recovery.

Broader themes include persistent currency depreciation exacerbating import inflation, though labor market strength offers some support for consumption.