Japan Macro Daily(Beta Mode)

Machinery Orders Surge, Yields Jump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 57,877.39 | +2.43% |

| USD/JPY | 158.97 | +0.11% |

| EUR/JPY | 187.65 | +0.16% |

| GBP/JPY | 215.64 | +0.03% |

| Gold | 4,813.00 | -0.25% |

| Brent Crude | 94.94 | +0.16% |

| Bitcoin | 74,875.00 | +0.93% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.35% | +11.14% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BOJ Gov Ueda Speech | - | - | - |

| Machinery Orders Month-over-Month | -5.50 | -1.10 | 13.60 |

| Machinery Orders Year-over-Year | 13.70 | 8.50 | 24.70 |

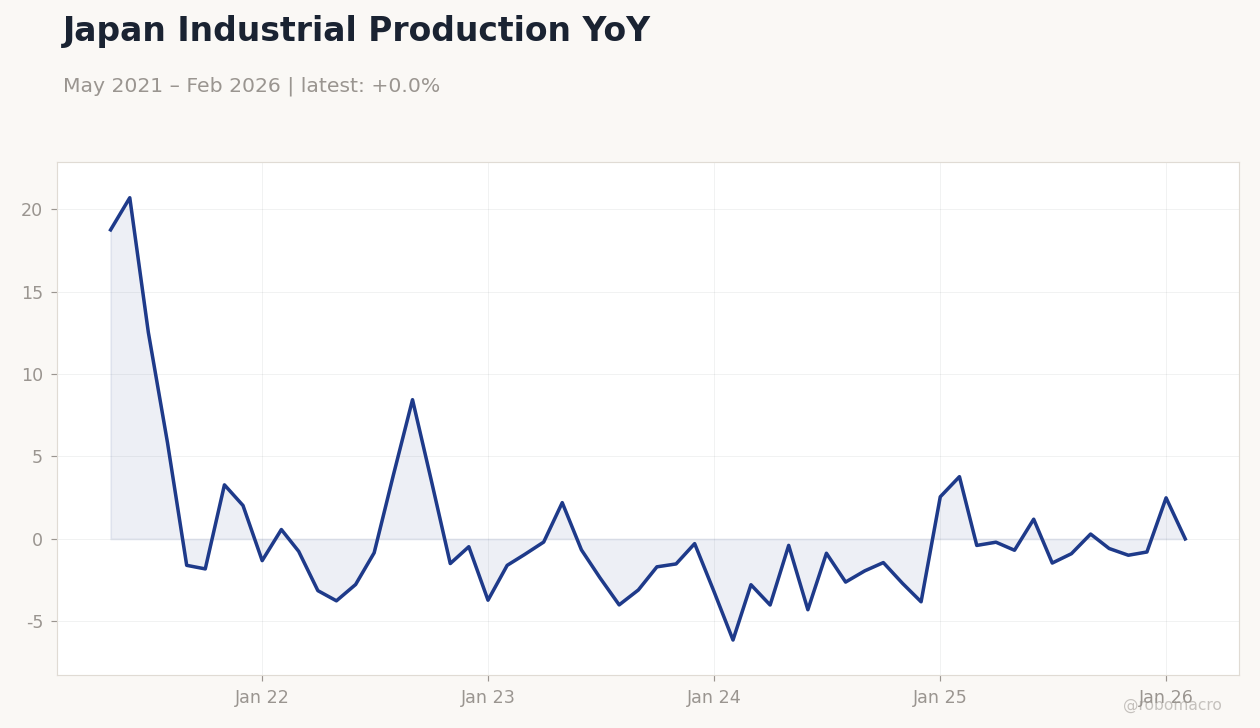

Japan Industrial Production YoY | Type: macro_line | Industrial Production (% YoY): 0 (2026-02-01) | Range: -6.13–20.69 | Trend(6pt): 18.74,-0.8419,-3.096,-2.695,2.49,0

Japan Industrial Production YoY | Type: macro_line | Industrial Production (% YoY): 0 (2026-02-01) | Range: -6.13–20.69 | Trend(6pt): 18.74,-0.8419,-3.096,-2.695,2.49,0

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Machinery orders beat forecasts sharply, pointing to strong capex recovery.

- Nikkei rose 2.43% amid risk-on mood; 10Y yields up 11.14% on inflation concerns.

- Yen softened versus majors as oil risks from Iran tensions pressured sentiment.

Yesterday's Recap

Japan's machinery orders beat expectations, with month-over-month growth at 13.6% versus consensus of -1.1%, and year-over-year at 24.7% against 8.5%, highlighting robust business investment. Bank of Japan Governor Ueda gave a speech, with no immediate market reaction noted. The Nikkei 225 advanced 2.43% to 57,877.39, supported by tech and export gains in a global risk-on environment.

USD/JPY rose 0.11% to 158.97, EUR/JPY gained 0.16% to 187.65, and GBP/JPY increased 0.03% to 215.64, influenced by elevated oil prices. Japan 10Y government bond yields rose 11.14% to 2.35%, signaling inflation worries from geopolitical factors. The 2Y yield remained at 0.73%, matching the BoJ's policy rate.

Markets reacted positively to the data, with equities strong despite mild yen weakness.

The Day Ahead

No significant Japanese economic data is due today, allowing markets to digest recent developments. Focus may turn to global events, such as Middle East updates affecting oil and yen. Tomorrow also has no key releases, likely shifting attention to currency and bond movements.

Watch for any impromptu BoJ statements or external data impacting Japanese assets. Asian sentiment could influence Nikkei in the absence of local drivers. JGB volatility may arise from global yield shifts.

Other Economic Notes

Standard Chartered notes Japan's higher inflation and weaker growth outlook, challenging policy normalization. Rising oil prices from Iran risks are weakening the yen, with EUR/JPY steady near 187.50. Japanese banks are competing for dollars to fund overseas payments, reflecting liquidity pressures amid depreciation.

Yen has reached new lows against the Singapore dollar, underscoring broad weakness.

Global Macro News

Tensions in the Strait of Hormuz, tempered by Iran diplomacy, are making yen bulls cautious, adding to currency pressure. The IMF states the Bank of Japan can ignore temporary inflation shocks from the Iran war, favoring policy stability. Brent crude rose 0.16% to 94.94, weighing on yen strength and steadying EUR/JPY at 187.50.

(cont...)