Japan Macro Daily(Beta Mode)

Yen Weakens on Stagflation Fears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 59,596.10 | +1.31% |

| USD/JPY | 158.96 | -0.13% |

| EUR/JPY | 187.18 | +0.18% |

| GBP/JPY | 214.88 | +0.14% |

| Gold | 4,813.90 | -0.90% |

| Brent Crude | 95.15 | +5.28% |

| Bitcoin | 75,696.82 | +2.49% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.35% | +11.14% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

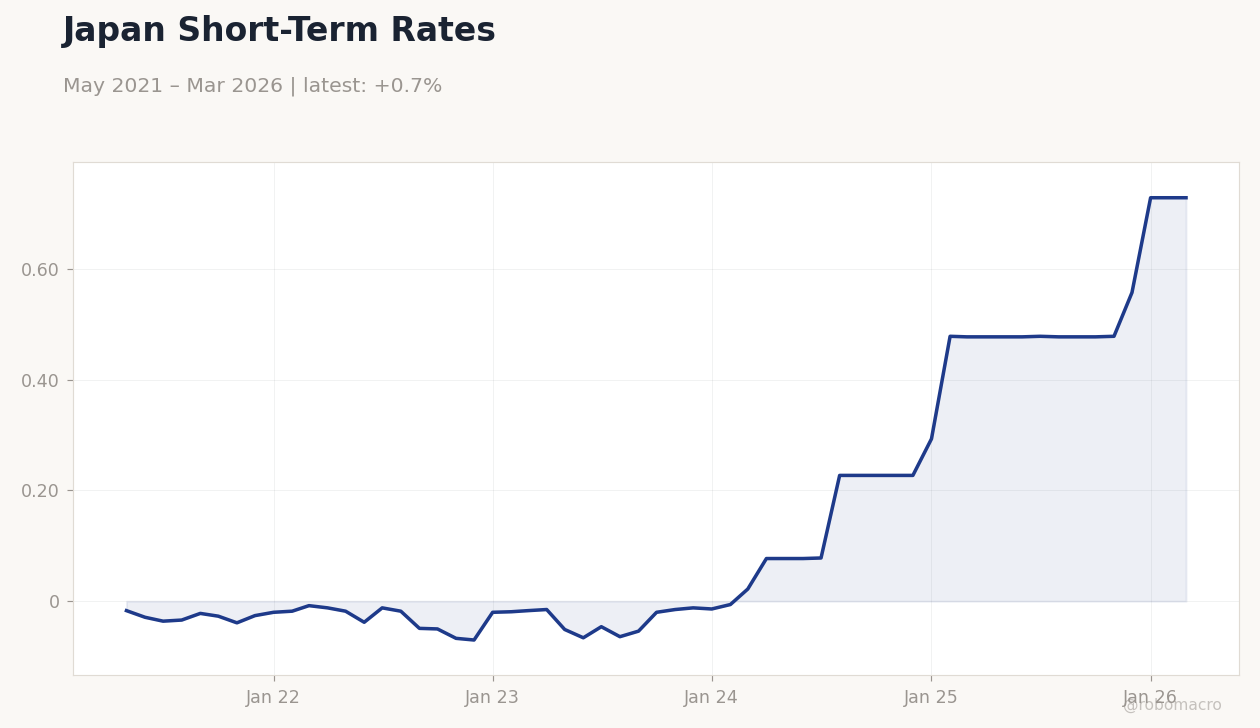

Japan Short-Term Rates | Type: macro_line | Short-Term Rate %: 0.728 (2026-03-01) | Range: -0.07–0.728 | Trend(5pt): -0.017,-0.012,-0.054,0.227,0.728

Japan Short-Term Rates | Type: macro_line | Short-Term Rate %: 0.728 (2026-03-01) | Range: -0.07–0.728 | Trend(5pt): -0.017,-0.012,-0.054,0.227,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-04-21) | |||

| Trade Balance | 57,300m | 1,106,000m | 15:50 |

| Exports Year-over-Year | 4.20 | 11 | 15:50 |

| Wednesday (2026-04-22) | |||

| S&P Global Manufacturing PMI Flash | 51.60 | 51.80 | 16:30 |

| S&P Global Services PMI Flash | 53.40 | - | 16:30 |

| Thursday (2026-04-23) | |||

| Inflation Rate Year-over-Year | 1.30 | - | 15:30 |

| Core Inflation Rate Year-over-Year | 1.60 | 1.80 | 15:30 |

- Yen softens amid BoJ Governor Ueda's stagflation warnings, with USD/JPY near 159 despite minor daily dip.

- Nikkei surges 1.31% on risk-on mood, while 10Y JGB yield rises sharply on policy tightening bets.

- Hormuz tensions lift Brent crude 5.28%, raising Japan's import costs and inflation pressures.

Yesterday's Recap

Japanese markets advanced, with the Nikkei 225 up 1.31% to 59,596.10, supported by gains in tech and export sectors amid reduced global risks. The yen firmed slightly against peers, as USD/JPY declined 0.13% to 158.96, EUR/JPY increased 0.18% to 187.18, and GBP/JPY rose 0.14% to 214.88, driven by limited safe-haven demand despite ongoing weakness. Japan 10Y government bond yield climbed to 2.35% with a notable increase, reflecting expectations of BoJ tightening amid stagflation concerns.

The 2Y yield remained at 0.73%, consistent with the current policy rate. No significant data was released, though reports of potential forex intervention briefly boosted sentiment. Gold fell 0.90% to 4,813.90, while Bitcoin advanced 2.49% to 75,696.82, showing varied risk sentiment.

Brent crude jumped 5.28% to 95.15, amplifying Japan's energy import challenges.

The Day Ahead

Key releases start tomorrow with Japan's trade balance at 15:50 ET, consensus at 1.106 trillion yen surplus versus prior 57.3 billion, which could support the yen if strong. Exports year-over-year are expected at 11% from 4.2%, gauging external demand and industrial strength. Wednesday includes S&P Global Manufacturing PMI flash at 16:30 ET, consensus 51.8 from 51.6, potentially indicating growth and affecting BoJ rate outlooks.

Services PMI flash follows, no consensus but prior 53.4, assessing service activity amid labor costs. Thursday brings inflation rate year-over-year at 15:30 ET, no consensus but prior 1.3%, vital for normalization path. Core inflation consensus is 1.8% from 1.6%, which might reinforce Ueda's stagflation alerts if elevated.

Other Economic Notes

Japan has transitioned from negative rates, with the BoJ policy rate at 0.73% as of March 2026, enabling measured normalization yet straining the yen due to low real rates. Fiscal estimates project an 8.4 trillion yen increase in JGB interest costs by FY 2034, highlighting debt challenges as yields rise. Sustained wage increases and export rebound are essential for deflation exit, but oil disruptions from geopolitics may intensify imported inflation.