Japan Macro Daily(Beta Mode)

Yen Weakens on Geopolitics, BoJ Warns

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 58,824.89 | +0.60% |

| USD/JPY | 159.37 | +0.13% |

| EUR/JPY | 187.12 | +0.15% |

| GBP/JPY | 215.23 | +0.30% |

| Gold | 4,738.50 | -1.42% |

| Brent Crude | 93.86 | -1.70% |

| Bitcoin | 75,589.48 | -0.37% |

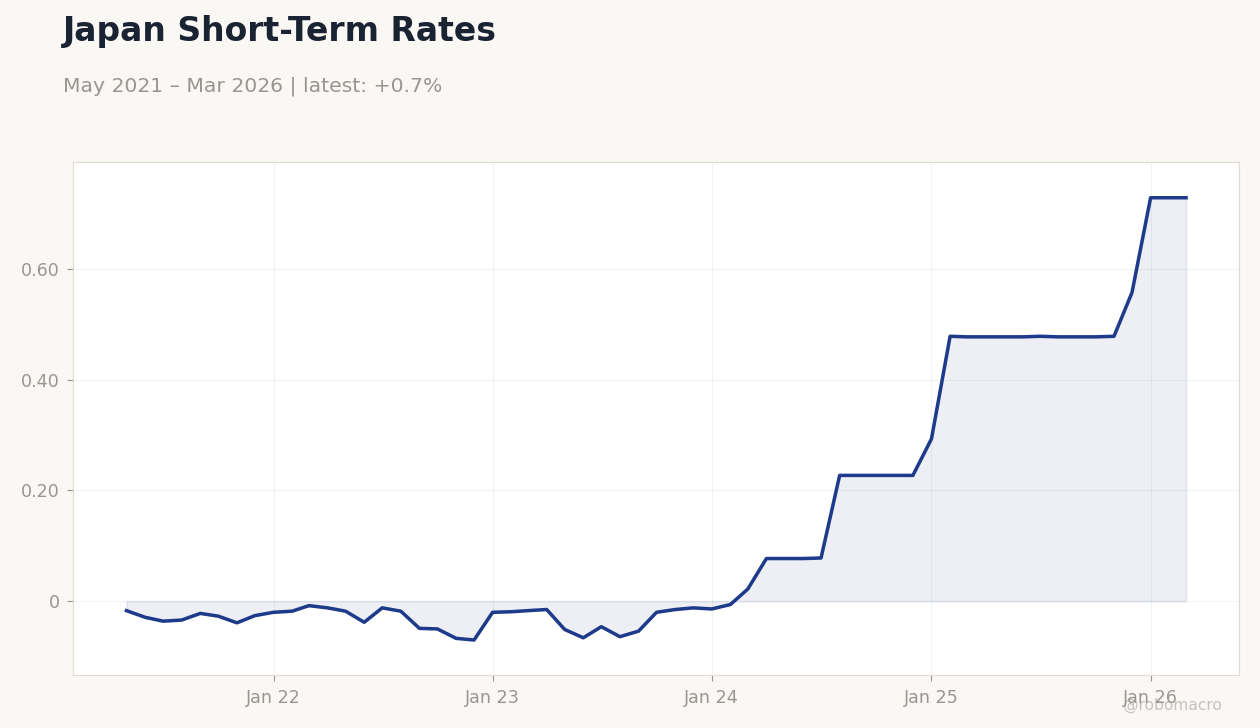

| Japan 2Y Govt Yield | 0.73% | +0.00% |

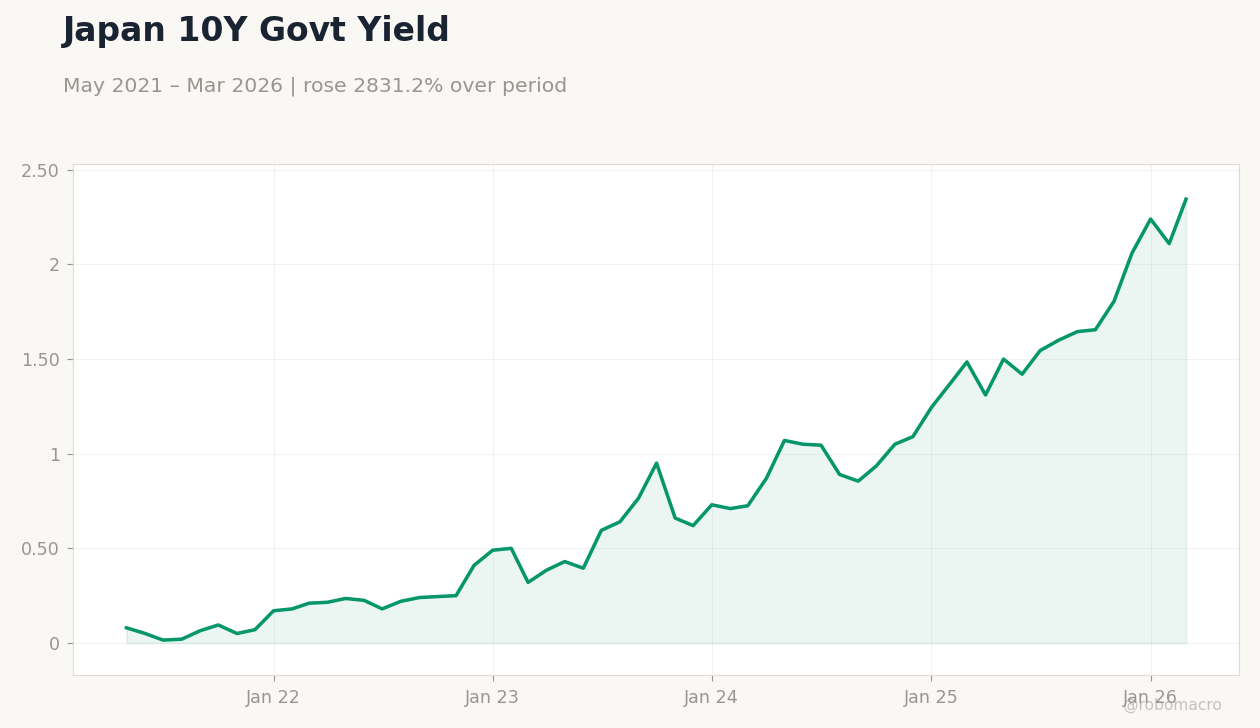

| Japan 10Y Govt Yield | 2.35% | +11.14% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan Short-Term Rates | Type: macro_line | Short-Term Rate: 0.728 (2026-03-01) | Range: -0.07–0.728 | Trend(5pt): -0.017,-0.012,-0.054,0.227,0.728

Japan Short-Term Rates | Type: macro_line | Short-Term Rate: 0.728 (2026-03-01) | Range: -0.07–0.728 | Trend(5pt): -0.017,-0.012,-0.054,0.227,0.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 57,300m | 1,106,000m | 15:50 |

| Exports Year-over-Year | 4.20 | 11 | 15:50 |

| Wednesday (2026-04-22) | |||

| S&P Global Manufacturing PMI Flash | 51.60 | 51.80 | 16:30 |

| S&P Global Services PMI Flash | 53.40 | - | 16:30 |

| Thursday (2026-04-23) | |||

| Inflation Rate Year-over-Year | 1.30 | - | 15:30 |

| Core Inflation Rate Year-over-Year | 1.60 | 1.80 | 15:30 |

- Yen softens amid US-Iran tensions and Middle East risks, pushing USD/JPY to 159.37.

- BoJ affirms financial system stability but highlights geopolitical and non-bank vulnerabilities.

- Markets eye upcoming trade data; Nikkei gains 0.60% on exporter boost.

Yesterday's Recap

Japanese markets saw modest gains yesterday with the Nikkei 225 closing at 58,824.89, up 0.60%, driven by exporter stocks benefiting from a weaker yen. The USD/JPY pair rose 0.13% to 159.37, reflecting yen depreciation amid renewed geopolitical tensions in the Strait of Hormuz. JGB yields surged, with the 10-year yield jumping 11.14% to 2.35%, signaling market bets on delayed BoJ normalization due to external risks.

EUR/JPY and GBP/JPY also advanced, by 0.15% to 187.12 and 0.30% to 215.23 respectively, as safe-haven demand for yen waned. Gold and Brent crude declined, with gold down 1.42% to 4,738.50 and Brent off 1.70% to 93.86, pressuring commodity-linked sectors in Japan. Bitcoin edged lower by 0.37% to 75,589.48, while the 2-year JGB yield held steady at 0.73%.

No major data releases occurred, but BoJ's stability report influenced sentiment, tempering rate hike expectations.

The Day Ahead

Today's key releases include Japan's Trade Balance at 15:50 ET, with consensus expecting a 1.106 trillion yen surplus versus the previous 57.3 billion yen. Exports Year-over-Year are forecast at 11% growth, up from 4.2%, potentially signaling stronger external demand amid yen weakness. Tomorrow brings S&P Global Manufacturing PMI Flash at 16:30 ET, consensus 51.8 from 51.6, offering insights into industrial momentum.

Services PMI Flash follows, with no consensus but prior at 53.4, highlighting domestic recovery trends. Thursday's Inflation Rate Year-over-Year lacks consensus but follows 1.3% previous, while Core Inflation is eyed at 1.8% from 1.6%. These data points could shape BoJ policy expectations amid ongoing yen pressures.

Other Economic Notes

Broader themes in Japan's economy include persistent yen depreciation, exacerbated by slow BoJ rate hikes as warned by the ADB chief, potentially fueling import inflation. Retail investors are increasingly embracing shareholder activism, as noted in Nikkei Asia, which could drive corporate governance reforms and boost equity valuations. Opposition pushes for a 5-year primary balance surplus roadmap highlight fiscal discipline concerns amid rising rate fears, influencing JGB supply dynamics.