Japan Macro Daily(Beta Mode)

Yen Weakens Ahead of GDP as Bonds Slump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 61,409.29 | -1.99% |

| USD/JPY | 158.75 | -0.06% |

| EUR/JPY | 185.07 | +0.32% |

| GBP/JPY | 213.26 | +0.87% |

| Gold | 4,570.80 | +0.33% |

| Brent Crude | 109.28 | +0.02% |

| Bitcoin | 77,091.99 | -0.44% |

| Japan 2Y Govt Yield | 0.73% | -0.14% |

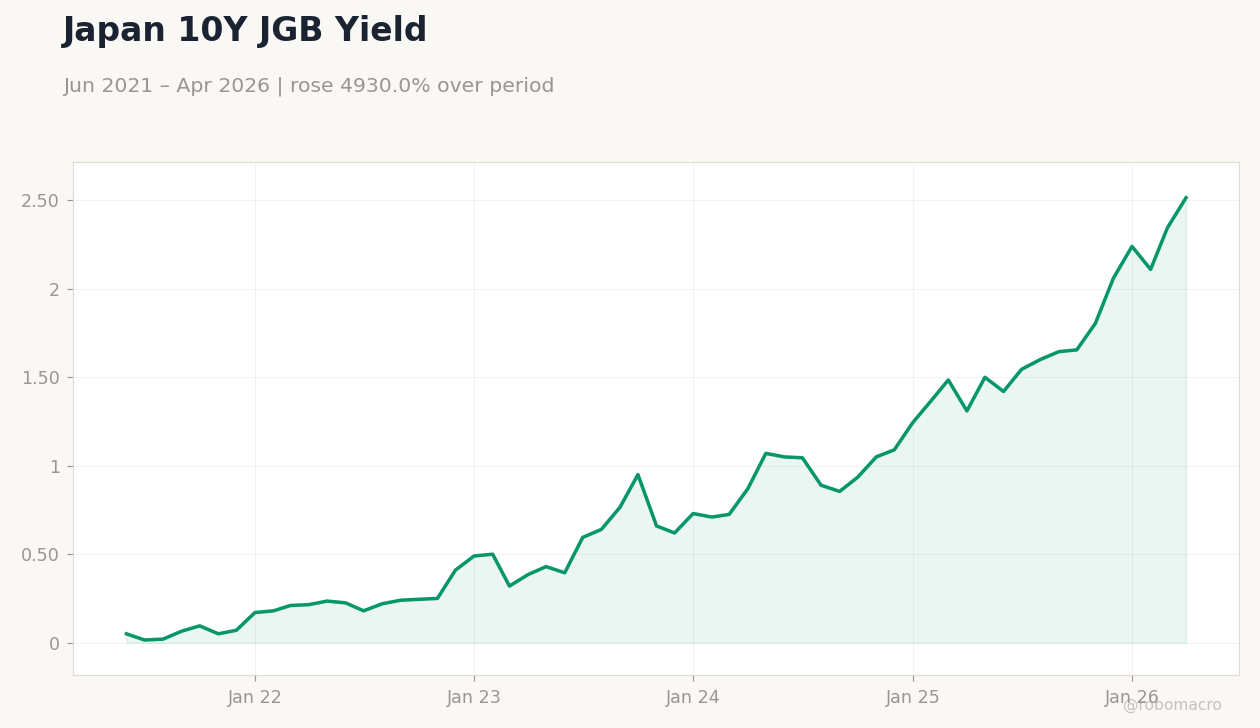

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan Short-Term Policy Rate | Type: macro_line | Policy Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.029,-0.018,-0.02,0.227,0.728,0.727

Japan Short-Term Policy Rate | Type: macro_line | Policy Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.029,-0.018,-0.02,0.227,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter Preliminary | 0.30 | 0.40 | 15:50 |

| GDP Growth Annualized Prel | 1.30 | 1.70 | 15:50 |

| Wednesday (2026-05-20) | |||

| Trade Balance | 667,000m | -29,700m | 15:50 |

| Exports Year-over-Year | 11.70 | 9.30 | 15:50 |

| Machinery Orders Month-over-Month | 13.60 | -8.10 | 15:50 |

| Machinery Orders Year-over-Year | 24.70 | 4.50 | 15:50 |

| S&P Global Manufacturing PMI Flash | 55.10 | 54.50 | 16:30 |

| S&P Global Services PMI Flash | 51 | - | 16:30 |

| BoJ Koeda Speech | - | - | 17:30 |

- Japan GDP growth expected at 0.4% QoQ and 1.7% annualized, with markets watching for signs of sustained expansion.

- Yen hovers near intervention levels at 158.75 versus the dollar amid rising JGB yield volatility.

- BoJ rate-hike expectations firm for June as sticky inflation and bond-market concerns dominate.

Yesterday's Recap

Japanese markets closed lower on Monday with the Nikkei 225 falling 1.99% to 61,409.29 as investors positioned ahead of the GDP release. The 10-year JGB yield jumped 7.25% to 2.52%, reflecting fresh inflation fears tied to oil prices and reduced demand for long-duration bonds. USD/JPY eased 0.06% to 158.75 while cross rates such as EUR/JPY rose 0.32% to 185.07.

Traders interpreted sporadic yen spikes as possible official warning shots ahead of any formal intervention. No major data prints occurred, leaving sentiment driven by global dollar strength and domestic bond-market turbulence. The 2-year JGB yield slipped 0.14% to 0.73%, highlighting a steepening curve.

The Day Ahead

Japan releases preliminary GDP growth figures at 15:50 JST today, with consensus pointing to a 0.4% quarter-over-quarter gain and 1.7% annualized expansion. Attention will focus on whether domestic demand and net exports can sustain the modest recovery. Wednesday brings the trade balance, exports, and machinery orders, followed by S&P Global flash PMIs for manufacturing and services.

BoJ Deputy Governor Koeda is scheduled to speak at 17:30 JST, offering potential clues on policy timing. Core inflation data on Thursday will further inform the normalization path.

Other Economic Notes

Oil-price volatility continues to stoke inflation concerns, pressuring JGBs and supporting expectations for earlier BoJ tightening. Corporate bond issuance remains active, highlighted by Alphabet’s record yen-denominated sale by a foreign issuer. Fiscal policy debates intensify around cash-register efficiency and debt sustainability, adding to market sensitivity around yield movements.

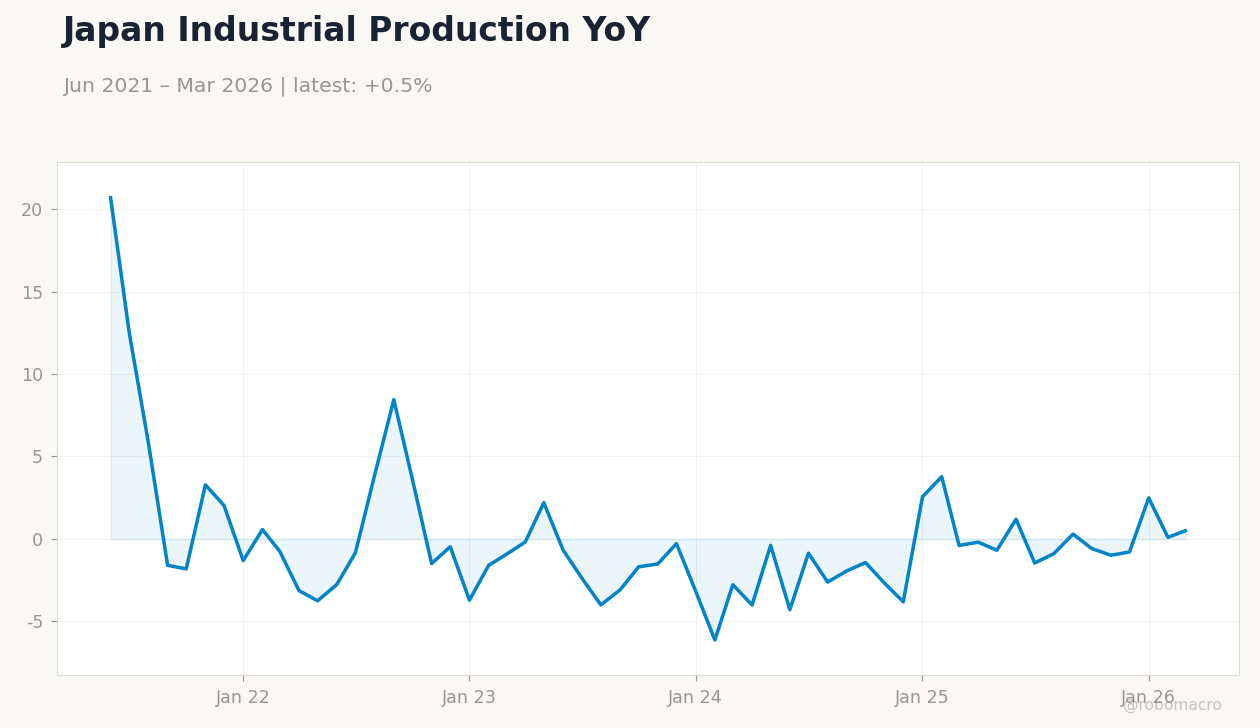

Broader data show industrial production beating forecasts last month, reinforcing the case for gradual policy adjustment.

Global Macro News

Hawkish Federal Reserve bets have lifted the dollar and weighed on the yen despite softer oil prices. Traders assess Japan’s remaining intervention capacity as USD/JPY approaches levels that previously triggered official action. <i>↓ p.2</i>