Japan Macro Daily(Beta Mode)

GDP Beat Fuels BoJ Hike Bets, Yields Jump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 60,815.95 | -0.97% |

| USD/JPY | 158.99 | +0.10% |

| EUR/JPY | 184.52 | -0.34% |

| GBP/JPY | 213.12 | +0.81% |

| Gold | 4,486.40 | -1.45% |

| Brent Crude | 111.04 | -0.95% |

| Bitcoin | 76,928.37 | -0.03% |

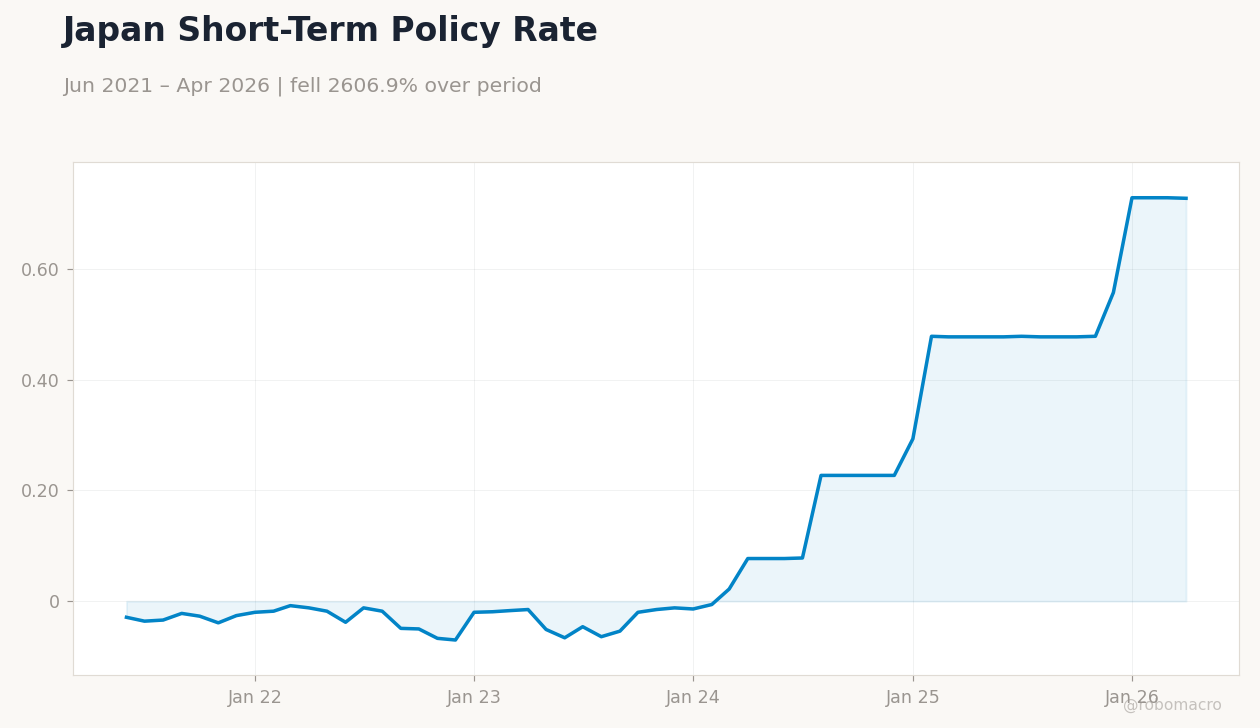

| Japan 2Y Govt Yield | 0.73% | -0.14% |

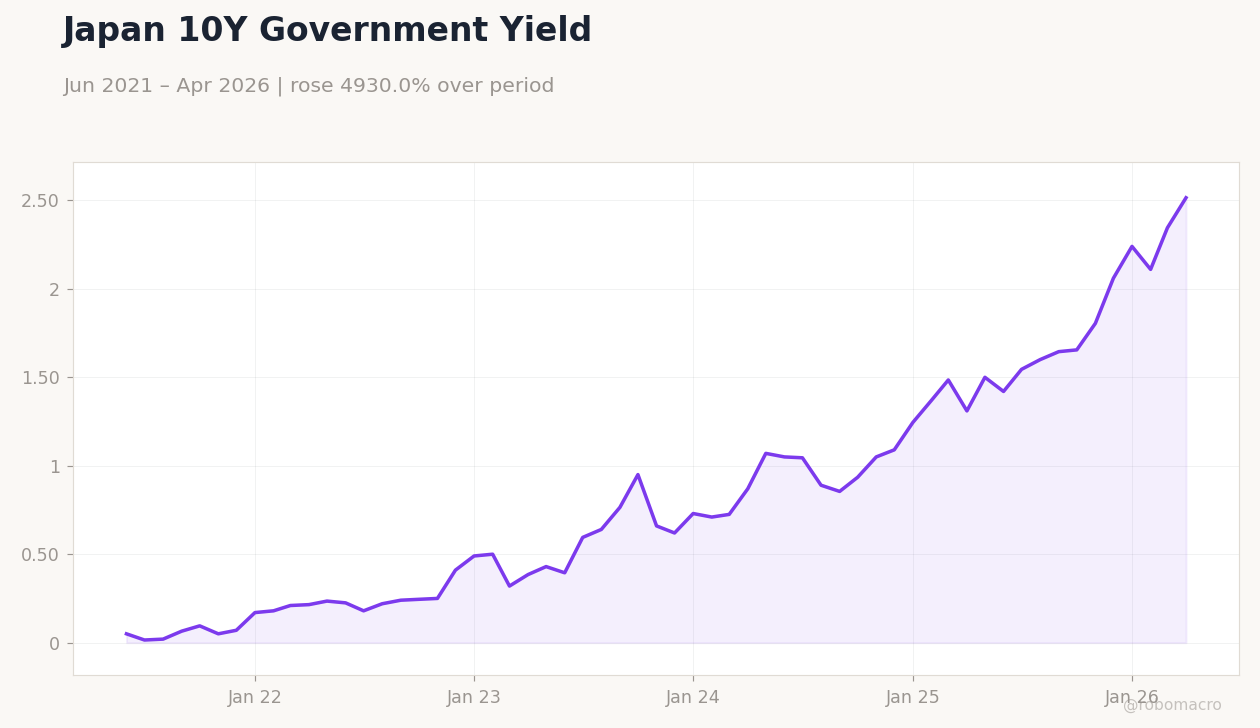

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

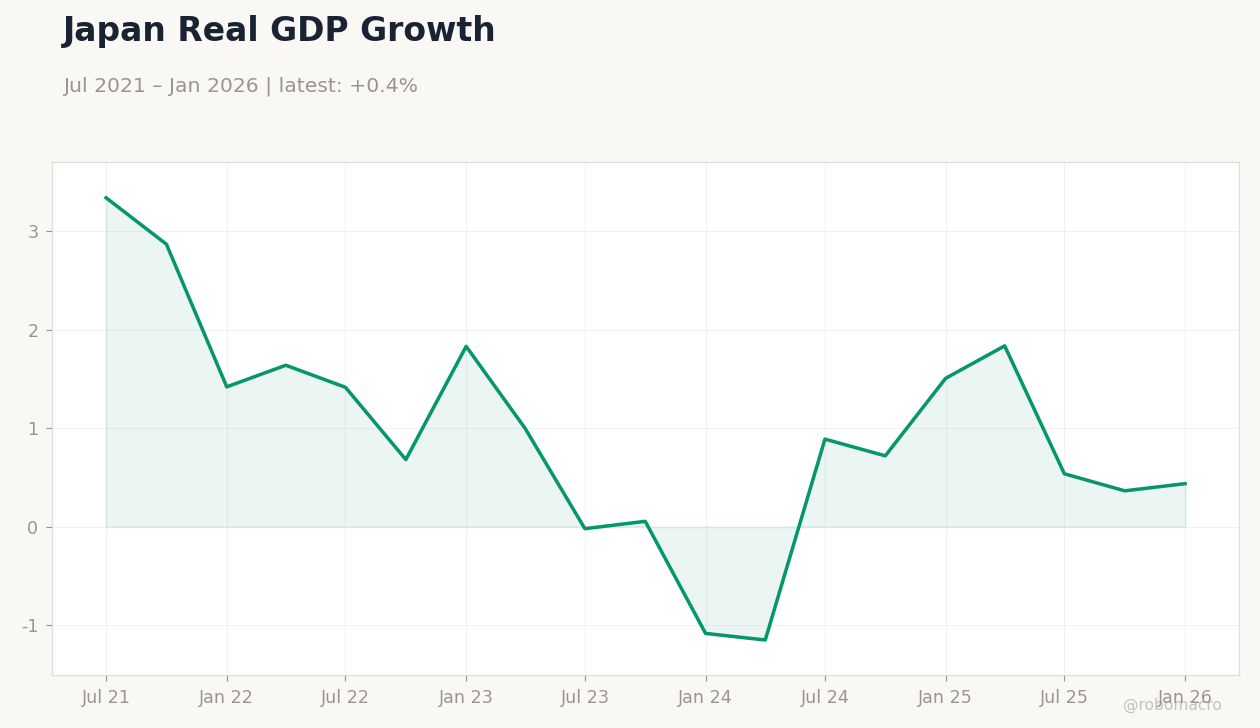

| GDP Growth Quarter-over-Quarter Preliminary | 0.20 | 0.40 | 0.50 |

| GDP Growth Annualized Prel | 0.80 | 1.70 | 2.10 |

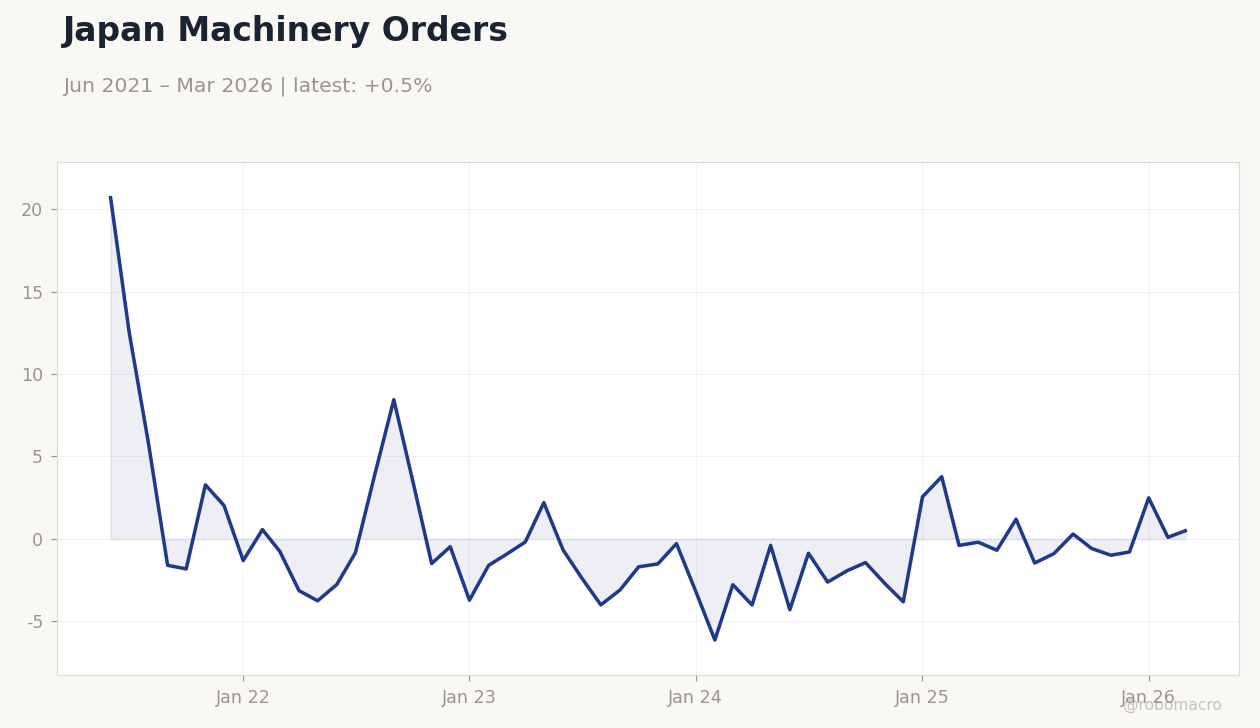

Japan Machinery Orders | Type: macro_line | Machinery Orders YoY %: 0.4946 (2026-03-01) | Range: -6.13–20.69 | Trend(6pt): 20.69,3.865,-1.693,-3.813,0.09833,0.4946

Japan Machinery Orders | Type: macro_line | Machinery Orders YoY %: 0.4946 (2026-03-01) | Range: -6.13–20.69 | Trend(6pt): 20.69,3.865,-1.693,-3.813,0.09833,0.4946

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-05-20) | |||

| Trade Balance | 667,000m | -29,700m | 15:50 |

| Exports Year-over-Year | 11.70 | 9.30 | 15:50 |

| Machinery Orders Month-over-Month | 13.60 | -8.10 | 15:50 |

| Machinery Orders Year-over-Year | 24.70 | 4.50 | 15:50 |

| S&P Global Manufacturing PMI Flash | 55.10 | 54.50 | 16:30 |

| S&P Global Services PMI Flash | 51 | - | 16:30 |

| BoJ Koeda Speech | - | - | 17:30 |

| Thursday (2026-05-21) | |||

| Inflation Rate Year-over-Year | 1.50 | - | 15:30 |

- Japan Q1 GDP growth beat expectations at 0.5% QoQ and 2.1% annualized, driven by consumption and exports.

- Nikkei 225 fell 0.97% while 10-year JGB yields jumped 7.25% to 2.52% on inflation concerns.

- BoJ policy rate holds at 0.73% with markets pricing higher odds of near-term normalisation.

Yesterday's Recap

Japan released stronger-than-expected Q1 GDP figures, with quarter-over-quarter growth at 0.5% versus 0.4% consensus and annualized growth reaching 2.1% against 1.7% expected. The beat reflected resilient private consumption and solid export performance. Equity markets reacted negatively, sending the Nikkei 225 down 0.97% to 60,815.95.

The yen remained largely steady against the dollar, with USD/JPY rising just 0.10% to 158.99 despite the positive data. JGB yields surged, with the 10-year yield climbing sharply to 2.52% amid fresh oil-driven inflation fears. News flow highlighted that the growth surprise has increased the likelihood of an earlier Bank of Japan rate hike.

The Day Ahead

Attention turns to Wednesday’s high-impact trade balance release, expected to swing to a deficit of 29.7 billion yen. Export growth is forecast to slow to 9.3% year-over-year from 11.7%. Machinery orders are projected to contract 8.1% month-over-month after a strong prior reading.

Flash S&P Global manufacturing and services PMIs will provide fresh activity signals, with manufacturing expected at 54.5. BoJ board member Koeda is scheduled to speak at 17:30 JST, offering potential policy clues. Core inflation data due Thursday will further shape rate expectations.

Other Economic Notes

Oil price volatility has reignited inflation concerns, pressuring JGBs lower and complicating the BoJ’s yield curve control efforts. The ruling LDP is advancing proposals for tokenized deposits and yen stablecoins, aiming to modernize payment infrastructure. Broader fiscal dynamics remain in focus as authorities weigh growth support against rising debt-service costs.

Recent verbal intervention warnings have so far failed to reverse yen depreciation pressures.

Global Macro News

The Australian dollar slipped against the yen following the strong Japanese GDP print. The euro struggled versus the yen even as the ECB maintained a hawkish tone. <i>↓ p.2</i>