Japan Macro Daily(Beta Mode)

Koeda Signals Hike Risk as GDP Beats Forecasts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 59,804.41 | -1.23% |

| USD/JPY | 158.96 | -0.05% |

| EUR/JPY | 184.65 | +0.03% |

| GBP/JPY | 213.34 | -0.04% |

| Gold | 4,541.50 | +0.23% |

| Brent Crude | 104.93 | -0.09% |

| Bitcoin | 77,668.81 | +0.27% |

| Japan 2Y Govt Yield | 0.73% | -0.14% |

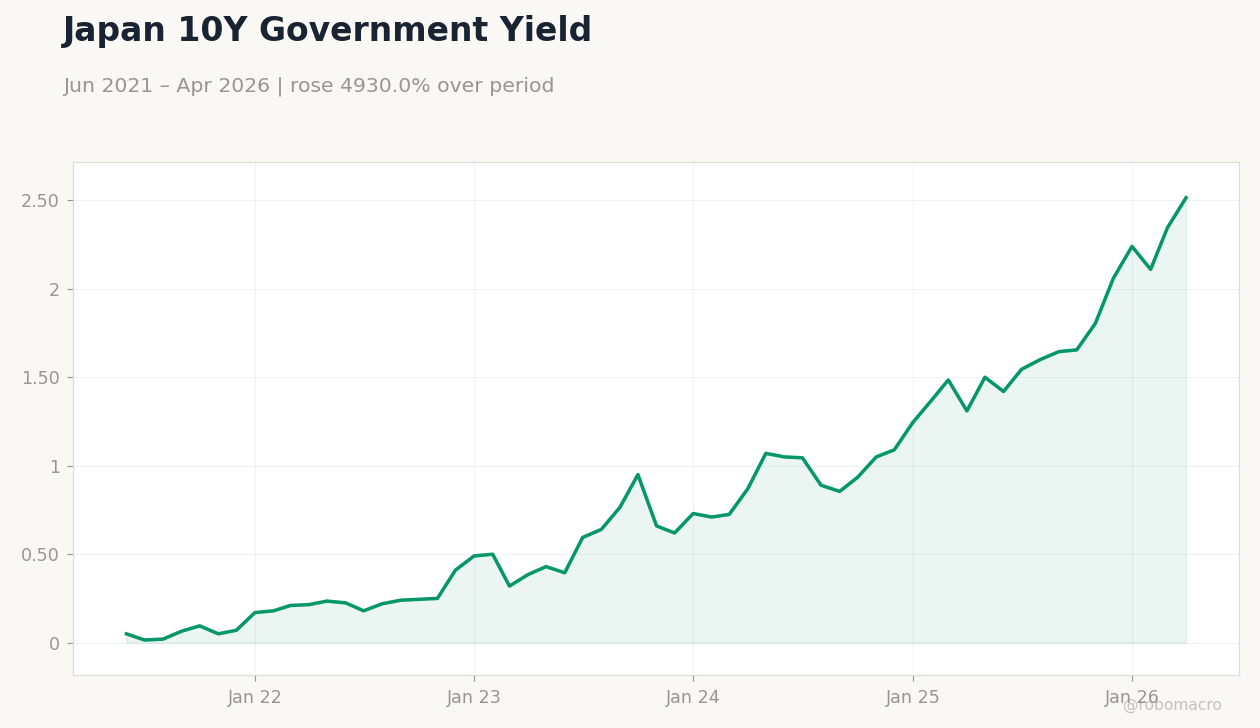

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter Preliminary | 0.20 | 0.40 | 0.50 |

| GDP Growth Annualized Prel | 0.80 | 1.70 | 2.10 |

| Trade Balance | 643,000m | -29,700m | 301,900m |

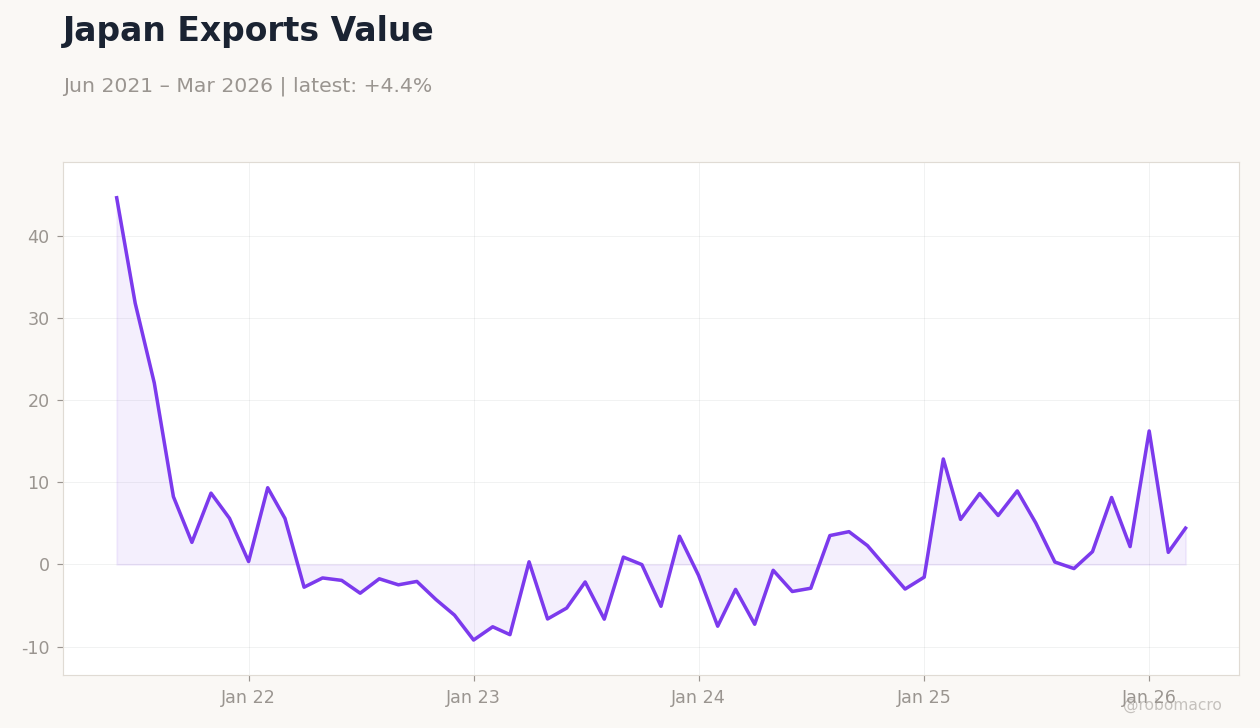

| Exports Year-over-Year | 11.50 | 9.30 | 14.80 |

| Machinery Orders Month-over-Month | 13.60 | -8.10 | -9.40 |

| Machinery Orders Year-over-Year | 24.70 | 4.50 | 5.90 |

| S&P Global Manufacturing PMI Flash | 55.10 | 54.50 | 54.50 |

| S&P Global Services PMI Flash | 51 | - | 50 |

| BoJ Koeda Speech | - | - | - |

Japan Short-Term Policy Rate | Type: macro_line | Short-term Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.029,-0.018,-0.02,0.227,0.728,0.727

Japan Short-Term Policy Rate | Type: macro_line | Short-term Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.029,-0.018,-0.02,0.227,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.50 | - | 15:30 |

| Core Inflation Rate Year-over-Year | 1.80 | 1.70 | 15:30 |

- GDP growth beat expectations with QoQ at 0.5% and annualized at 2.1%

- Trade balance swung to 301.9 billion yen surplus while exports rose 14.8%

- BoJ board member Koeda highlighted rising cost pressures and underlying inflation near 2%

Yesterday's Recap

Japan released stronger-than-expected GDP figures for the first quarter, with quarter-over-quarter growth at 0.5% versus the 0.4% consensus and annualized growth reaching 2.1% against 1.7% expected. The trade balance printed a 301.9 billion yen surplus, far exceeding forecasts of a 29.7 billion yen deficit, while exports grew 14.8% year-over-year. Machinery orders declined 9.4% month-over-month but rose 5.9% year-over-year, showing mixed capital spending signals.

S&P Global manufacturing PMI held at 54.5 and services PMI eased to 50.0. Board member Koeda delivered a speech in Fukuoka stressing the need for monetary policy to address persistent inflation. Markets reacted with the Nikkei 225 falling 1.23% to 59,804.41 and the 10-year JGB yield jumping 7.25% to 2.52%.

USD/JPY remained near 158.96 as the yen absorbed the data without sharp moves.

The Day Ahead

Markets await the May nationwide CPI release due at 15:30 JST, which will update the inflation trajectory ahead of potential BoJ adjustments. Core CPI is expected to print 1.7% year-over-year. No additional BoJ speakers are scheduled, leaving focus on the data print itself.

Traders will also monitor any follow-through from Koeda’s remarks on cost pressures. The outcome could shift OIS pricing for a July policy move.

Other Economic Notes

Stronger GDP and export readings reinforce the case for gradual policy normalization at the Bank of Japan. Persistent cost pressures from global commodity trends continue to lift underlying inflation measures toward the 2% target. Machinery orders weakness may temper optimism on business investment in coming quarters.

Yen stability near 159 reflects a balance between domestic hawkish signals and external dollar strength. The policy rate stands at the verified 0.73% level.

Global Macro News

Strong US manufacturing PMI data lifted the dollar and weighed on the yen across G10 crosses. British pound traded cautiously versus the yen ahead of UK retail sales and Japan CPI prints. <i>↓ p.2</i>