Japan Macro Daily(Beta Mode)

Soft CPI Dents BoJ Hike Hopes, Yen Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 63,339.07 | +2.68% |

| USD/JPY | 158.82 | -0.13% |

| EUR/JPY | 184.88 | +0.07% |

| GBP/JPY | 213.74 | +0.07% |

| Gold | 4,523.20 | -0.37% |

| Brent Crude | 100.21 | -2.31% |

| Bitcoin | 76,554.00 | -0.16% |

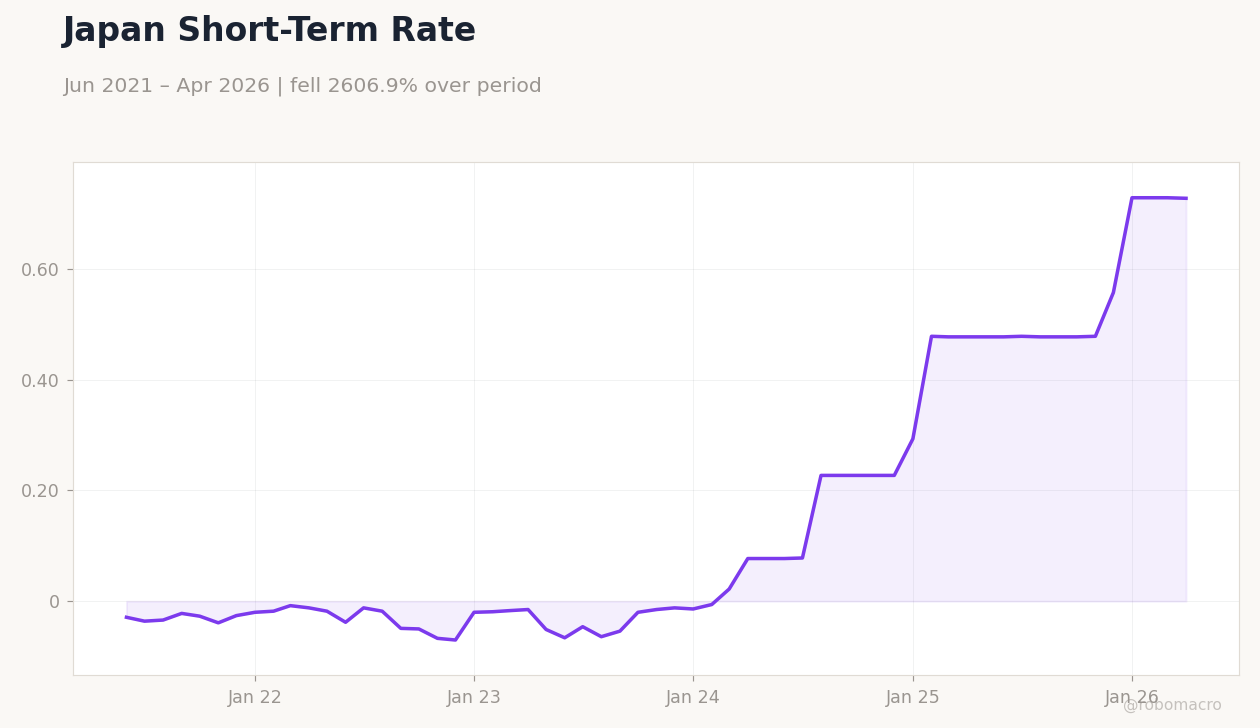

| Japan 2Y Govt Yield | 0.73% | -0.14% |

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

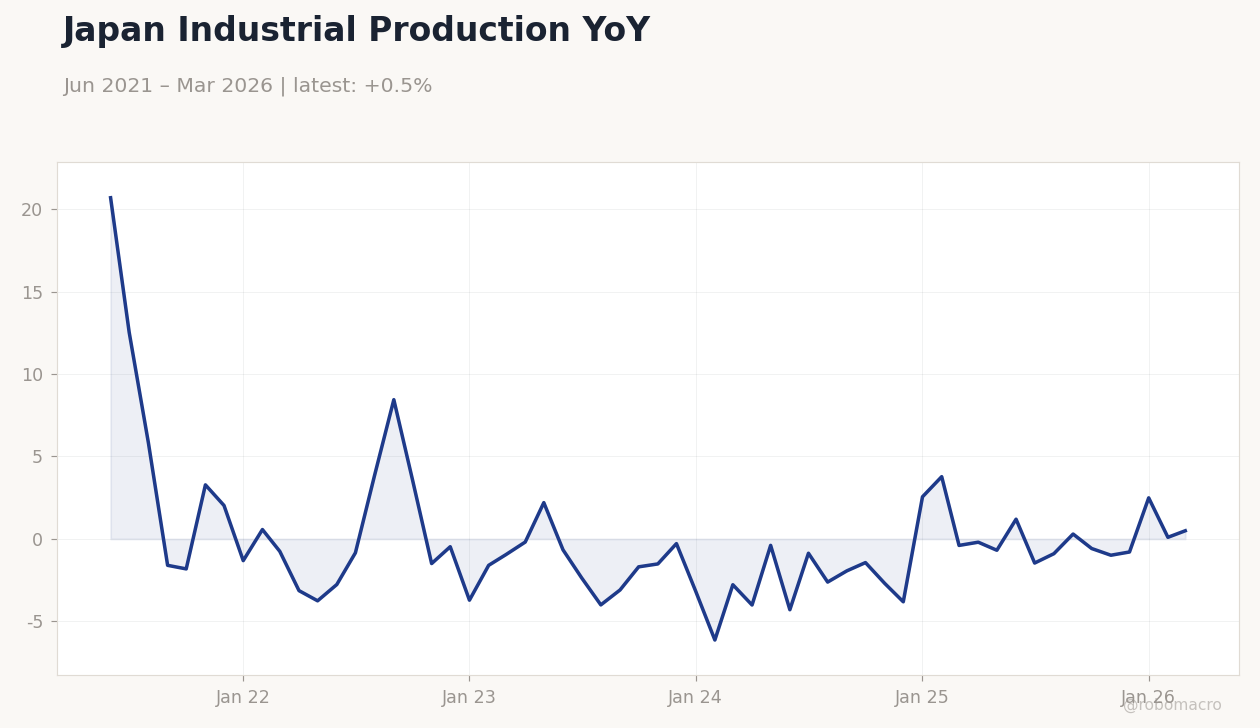

Japan Industrial Production YoY | Type: macro_line | IP YoY %: 0.4946 (2026-03-01) | Range: -6.13–20.69 | Trend(6pt): 20.69,3.865,-1.693,-3.813,0.09833,0.4946

Japan Industrial Production YoY | Type: macro_line | IP YoY %: 0.4946 (2026-03-01) | Range: -6.13–20.69 | Trend(6pt): 20.69,3.865,-1.693,-3.813,0.09833,0.4946

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-28) | |||

| Housing Starts Year-over-Year | -29.30 | 15.50 | 01:00 |

| Headline Unemployment Rate | 2.70 | 2.70 | 19:30 |

| Industrial Production Month-over-Month Preliminary | -0.40 | -1 | 19:50 |

| Retail Sales Year-over-Year | 1.70 | 1.30 | 19:50 |

| Friday (2026-05-29) | |||

| Consumer Confidence Index | 32.20 | 32 | 01:00 |

| Sunday (2026-05-31) | |||

| Capital Spending Year-over-Year | 6.50 | - | 19:50 |

- Japan April CPI slows more than expected to a four-year low, reducing near-term rate-hike odds

- Nikkei 225 climbs 2.68% to 63,339.07 while USD/JPY eases 0.13% to 158.82

- 10-year JGB yield surges 7.25% to 2.52% as the curve steepens on mixed policy signals

Yesterday's Recap

Equity markets advanced as the Nikkei 225 closed at 63,339.07, up 2.68%, supported by semiconductor strength and a softer yen. USD/JPY finished at 158.82 after a 0.13% decline, while EUR/JPY and GBP/JPY posted modest gains of 0.07%. The 2-year JGB yield held at 0.73% and the 10-year yield jumped to 2.52%, reflecting volatility after softer inflation data.

April national CPI slowed more than forecast, hitting a four-year low and prompting analysts to trim expectations for near-term BoJ tightening. Gold fell 0.37% to 4,523.20 and Brent crude dropped 2.31% to 100.21 amid softer demand signals. No major data releases occurred on 23 May, leaving market focus on the inflation print and PM Takaichi’s meeting with Governor Ueda.

The Day Ahead

Housing starts YoY, unemployment rate, industrial production MoM, and retail sales YoY are scheduled for release on 28 May. Consumer confidence will follow on 29 May and capital spending data on 31 May. Markets will scrutinise the production and sales figures for signs of underlying demand weakness after the soft CPI outcome.

Any further downside surprises could reinforce views that the BoJ will maintain its gradual approach. USD/JPY remains sensitive to intervention rhetoric near the 160 handle ahead of the releases.

Other Economic Notes

Energy price risks continue to cloud the inflation outlook even as headline readings ease. Wage growth remains a key threshold cited by officials before further policy steps. Corporate capital expenditure trends will be watched closely for evidence that domestic demand can sustain price pressures.

Broader fiscal-monetary coordination under the new administration adds another layer to normalisation timing.

Global Macro News

The Australian dollar faces headwinds from rate repricing that weigh on the yen according to Rabobank. UOB notes the yen’s negative bias versus the dollar is fading, reducing one-sided pressure. Intervention risk rises as USD/JPY approaches 160, with OCBC and Societe Generale highlighting official sensitivity at that level.

<i>↓ p.2</i>