Japan Macro Daily(Beta Mode)

Yen Slides on Soft CPI as Nikkei Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 63,339.07 | +2.68% |

| USD/JPY | 158.90 | -0.03% |

| EUR/JPY | 184.92 | -0.07% |

| GBP/JPY | 214.59 | +0.15% |

| Gold | 4,523.20 | +0.05% |

| Brent Crude | 100.21 | -3.22% |

| Bitcoin | 77,255.79 | +0.36% |

| Japan 2Y Govt Yield | 0.73% | -0.14% |

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan 10Y Yield vs Policy Rate | Type: macro_line | 10Y %: 2.515 (2026-04-01) | Range: 0.015–2.515 | Trend(6pt): 0.05,0.22,0.95,1.09,2.11,2.515 | Policy Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.029,-0.018,-0.02,0.227,0.728,0.727

Japan 10Y Yield vs Policy Rate | Type: macro_line | 10Y %: 2.515 (2026-04-01) | Range: 0.015–2.515 | Trend(6pt): 0.05,0.22,0.95,1.09,2.11,2.515 | Policy Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.029,-0.018,-0.02,0.227,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-28) | |||

| Housing Starts Year-over-Year | -29.30 | 15.50 | 01:00 |

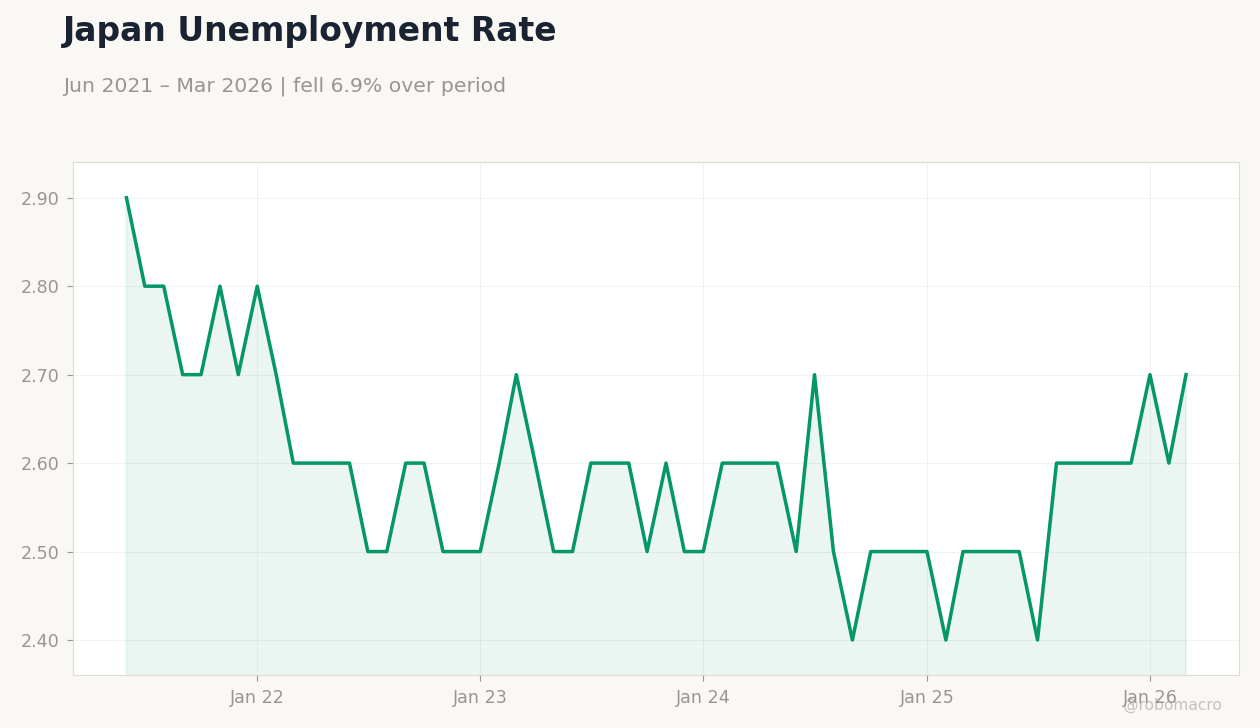

| Headline Unemployment Rate | 2.70 | 2.70 | 19:30 |

| Industrial Production Month-over-Month Preliminary | -0.40 | -0.90 | 19:50 |

| Retail Sales Year-over-Year | 1.70 | 1.30 | 19:50 |

| Friday (2026-05-29) | |||

| Consumer Confidence Index | 32.20 | 32 | 01:00 |

| Sunday (2026-05-31) | |||

| Capital Spending Year-over-Year | 6.50 | - | 19:50 |

- Soft April CPI at 1.4% four-year low dents BoJ hike expectations and weakens yen

- Nikkei 225 surges 2.68% to 63,339.07 on risk-on flows and earnings

- Japan 10Y yield jumps 7.25% to 2.52% while BoJ policy rate holds at 0.73%

Yesterday's Recap

Japanese markets reacted to softer-than-expected April national CPI that printed at a four-year low of 1.4% y/y. The Nikkei 225 advanced 2.68% to close at 63,339.07 amid solid corporate earnings and equity inflows. USD/JPY settled at 158.90 after a modest 0.03% decline as the yen found limited support from falling oil prices.

The 2-year JGB yield eased 0.14% to 0.73% while the 10-year yield rose sharply to 2.52%. News that intervention requires BoJ backing, according to HSBC, kept traders cautious on unilateral yen support. Retail sales and industrial production prints scheduled for later this week drew early positioning.

No major data releases occurred on 24 May.

The Day Ahead

Housing starts y/y, unemployment rate, industrial production m/m and retail sales y/y are due on 28 May. Consumer confidence will print on 29 May and capital spending data follows on 31 May. Markets will focus on whether retail sales beat the 1.3% consensus to reinforce domestic demand.

Any upside surprise in industrial production could lift USD/JPY above 159.00. BoJ speakers remain absent until early June, leaving data as the main driver. Yen volatility is expected to stay elevated ahead of the releases.

Other Economic Notes

Persistent yen softness continues to reflect the gap between BoJ policy rate at 0.73% and higher US yields. Energy price declines are easing import costs and providing modest relief to the trade balance. PM Takaichi’s call for appropriate monetary policy underscores political pressure on the BoJ to balance growth and inflation.

Equity strength above 63,000 signals investor confidence in corporate Japan despite currency swings. Broader themes point to gradual policy normalisation without abrupt tightening.

Global Macro News

Brent crude fell 3.22% to 100.21, supporting the yen via lower import bills. Gold held near 4,523.20 with minimal moves as risk appetite favoured equities. Bitcoin rose 0.36% to 77,255.79, tracking broader risk-on sentiment.

<i>↓ p.2</i>