Japan Macro Daily(Beta Mode)

Ueda Flags Oil Shock as Yen Nears Intervention

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 64,999.41 | +0.01% |

| USD/JPY | 159.19 | -0.03% |

| EUR/JPY | 185.47 | +0.09% |

| GBP/JPY | 214.05 | -0.01% |

| Gold | 4,526.00 | +1.77% |

| Brent Crude | 92.69 | -1.70% |

| Bitcoin | 73,489.15 | -1.15% |

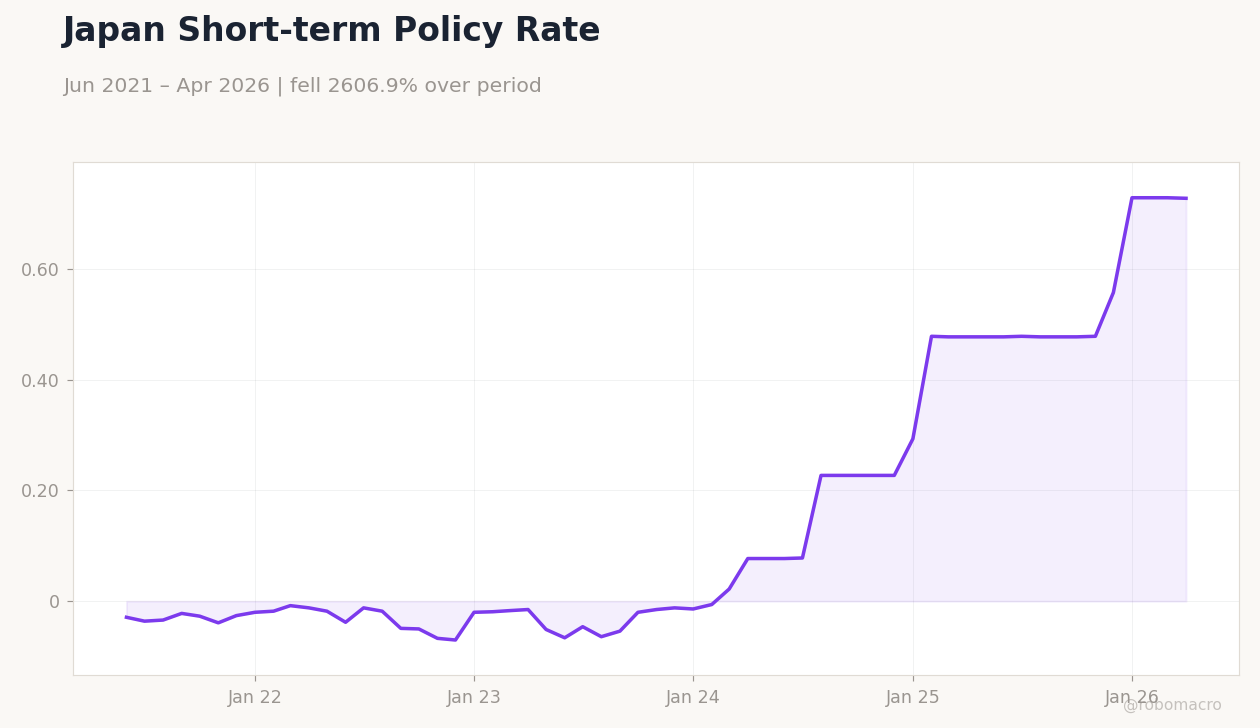

| Japan 2Y Govt Yield | 0.73% | -0.14% |

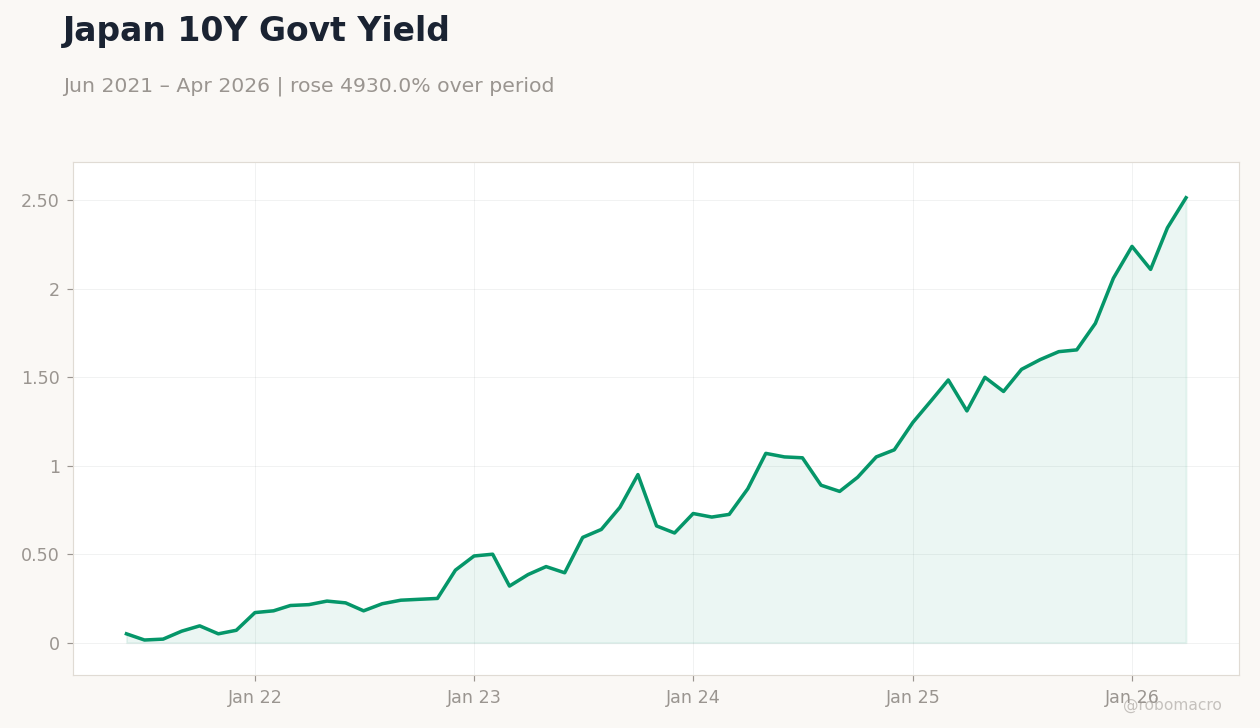

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoJ Gov Ueda Speech | - | - | - |

Brent Crude Oil Price | Type: macro_line | USD/bbl: 102.8 (2026-05-26) | Range: 59.93–138.2 | Trend(5pt): 70.03,98.81,79.82,74.89,102.8

Brent Crude Oil Price | Type: macro_line | USD/bbl: 102.8 (2026-05-26) | Range: 59.93–138.2 | Trend(5pt): 70.03,98.81,79.82,74.89,102.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 2.70 | 2.70 | 15:30 |

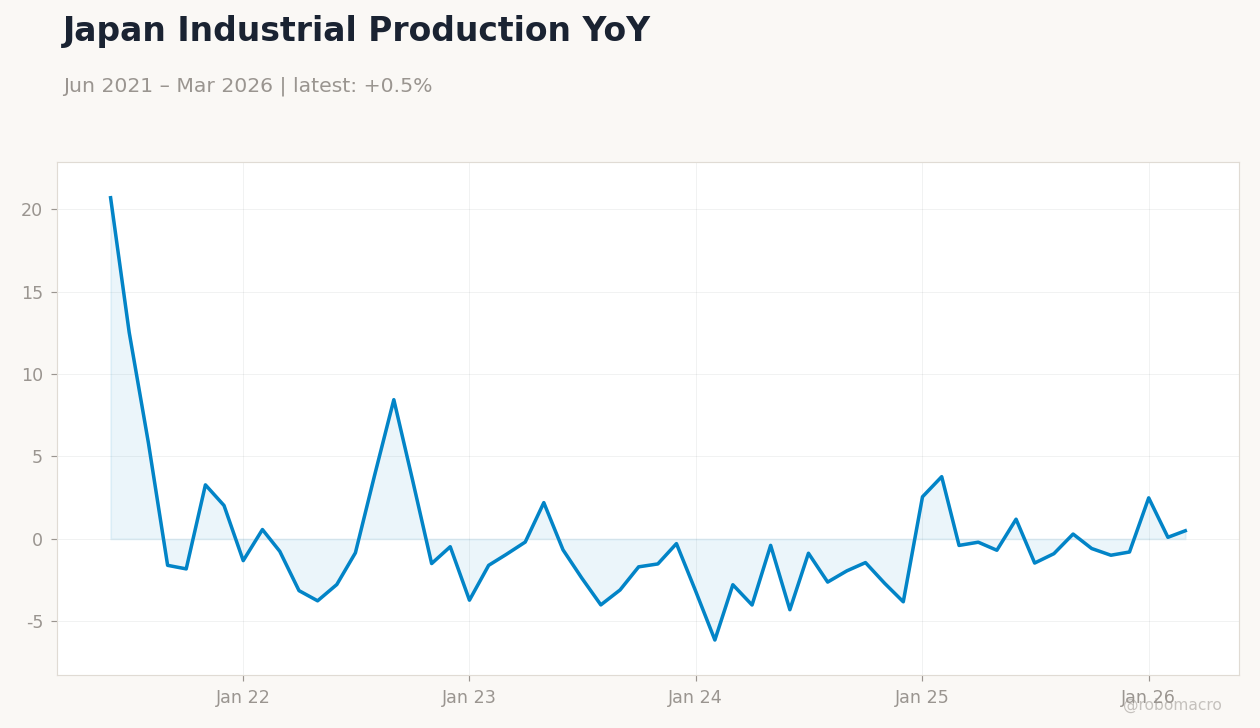

| Industrial Production Month-over-Month Preliminary | -0.40 | -0.90 | 15:50 |

| Retail Sales Year-over-Year | 1.70 | 1.30 | 15:50 |

| Friday (2026-05-29) | |||

| Consumer Confidence Index | 32.20 | 32 | 21:00 |

| Housing Starts Year-over-Year | -29.30 | 15.50 | 21:00 |

| Sunday (2026-05-31) | |||

| Capital Spending Year-over-Year | 6.50 | - | 15:50 |

- BoJ Governor Ueda highlighted oil price risks to inflation and growth, keeping rate hike speculation alive despite soft data.

- USD/JPY held near 159.19 with intervention data due, while Nikkei 225 closed flat at 64,999.41 amid mixed global flows.

- Japan 10Y yields jumped 7.25% to 2.52% as markets priced further policy normalisation ahead of today’s labour and output prints.

Yesterday's Recap

BoJ Governor Ueda warned of an oil price shock hitting Japanese households and firms, stressing the need to monitor second-round effects on wages and prices. The yen traded at 159.19 against the dollar with limited movement after the speech. Nikkei 225 finished almost unchanged at 64,999.41 after briefly topping 66,000 earlier in the session.

The 2-year JGB yield eased 0.14% to 0.73% while the 10-year yield surged to 2.52%. Markets absorbed the governor’s remarks without shifting the policy rate outlook materially. Intervention data releases scheduled for later this week kept traders cautious around the 160 level.

No other domestic indicators were published.

The Day Ahead

Headline unemployment is due at 15:30 ET with consensus at 2.7%, matching the prior print. Industrial production and retail sales follow at 15:50 ET, expected to show contraction of 0.9% m/m and 1.3% y/y respectively. Consumer confidence and housing starts print at 21:00 ET, with housing starts forecast to rebound sharply.

These releases will shape views on consumer resilience ahead of the next BoJ policy meeting. Traders will also watch for any Ministry of Finance comments on yen levels. No BoJ speakers are scheduled.

Other Economic Notes

Japan plans to issue bridging bonds to finance targeted investment schemes, adding to fiscal financing needs. Persistent yen weakness near 160 continues to fuel speculation over fresh intervention of up to 10 trillion yen. JGB yield curve steepening reflects markets adjusting to gradual policy normalisation.

Corporate earnings revisions, led by autos, have supported equity valuations despite macro uncertainty.

Global Macro News

US-Iran truce headlines lifted the yen by pressuring the dollar across G10 pairs. Brent crude fell 1.70% to 92.69 as higher OPEC+ supply signals weighed on energy prices. Gold rose 1.77% to 4,526 amid safe-haven demand.

<i>↓ p.2</i>