Japan Macro Daily(Beta Mode)

Rising Wages Bolster BOJ Hike Case Ahead of GDP

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 66,588.12 | -1.31% |

| USD/JPY | 160.26 | +0.17% |

| EUR/JPY | 184.50 | -0.68% |

| GBP/JPY | 213.51 | -0.57% |

| Gold | 4,365.30 | -2.47% |

| Brent Crude | 93.09 | -2.04% |

| Bitcoin | 61,870.70 | +1.65% |

| Japan 2Y Govt Yield | 0.73% | -0.14% |

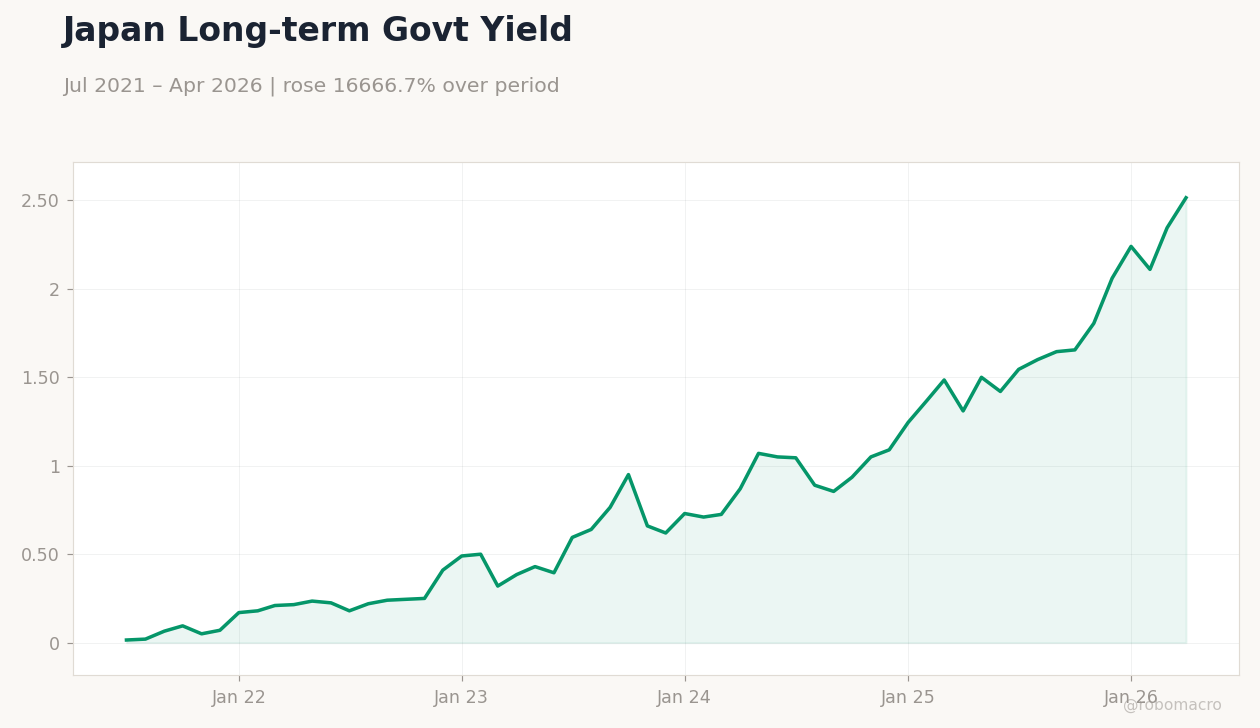

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan Short-term Policy Rate | Type: macro_line | Policy Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Japan Short-term Policy Rate | Type: macro_line | Policy Rate %: 0.727 (2026-04-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Balance | 4,682,000m | 3,137,000m | 19:50 |

| GDP Growth Annualized Final | 0.80 | 1.30 | 19:50 |

| GDP Growth Quarter-over-Quarter Final Estimate | 0.20 | 0.30 | 19:50 |

- Real wages rose for a fourth straight month, reinforcing the case for Bank of Japan policy normalisation.

- Final GDP figures and current account data due tonight will test growth resilience amid yen intervention.

- JGB 10-year yields jumped 7.25% while the Nikkei fell 1.31% as intervention funding concerns weighed.

Yesterday's Recap

Equity markets closed lower with the Nikkei 225 at 66,588.12, down 1.31%, as investors digested reports of Japanese sales of U.S. Treasuries to finance yen intervention. The 10-year JGB yield surged to 2.52% while the 2-year yield eased to 0.73%.

USD/JPY edged up 0.17% to 160.26 despite intervention headlines, reflecting persistent dollar strength. Real wage data showed a fourth consecutive monthly gain, providing fresh support for rate-hike expectations. No major data releases occurred yesterday, leaving markets focused on tonight’s releases and ongoing carry-trade adjustments.

Gold and Brent crude both declined more than 2% on softer global demand signals.

The Day Ahead

Final GDP growth annualised and quarter-over-quarter estimates are scheduled for release at 19:50 alongside the current account balance. Consensus forecasts point to annualised growth rising to 1.3% from 0.8% previously, with the quarter-on-quarter print expected at 0.3%. The current account is projected to narrow sharply to 3.137 trillion yen.

Markets will scrutinise the figures for evidence that consumption and exports remain on track. No Bank of Japan speakers are listed, keeping attention on data outcomes and any follow-up intervention signals.

Other Economic Notes

Rising real wages are viewed as critical validation for further policy tightening, with former Governor Kuroda noting wages now outpace prices. Analysts at Mitsubishi UFJ flagged the possibility of a larger-than-expected rate increase if yen weakness persists. Industrial production and household spending trends remain secondary to the wage and intervention narrative.

Broader concerns centre on whether delayed normalisation risks returning the economy to stagnation.

Global Macro News

U.S. jobs data reinforced dollar resilience, pushing the yen back toward pre-intervention levels in recent sessions. <i>↓ p.2</i>