Japan Macro Daily(Beta Mode)

Japan GDP Beat Fuels BOJ Rate-Hike Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 66,588.12 | -1.31% |

| USD/JPY | 160.16 | +0.11% |

| EUR/JPY | 184.73 | -0.56% |

| GBP/JPY | 213.66 | -0.50% |

| Gold | 4,348.30 | +0.26% |

| Brent Crude | 94.33 | +1.33% |

| Bitcoin | 63,312.56 | +0.12% |

| Japan 2Y Govt Yield | 0.73% | -0.14% |

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Current Account Balance | 4,682,000m | 3,137,000m | 3,907,000m |

| GDP Growth Annualized Final | 0.70 | 1.30 | 1.80 |

| GDP Growth Quarter-over-Quarter Final Estimate | 0.20 | 0.30 | 0.50 |

Japan 10Y Yield (3y) | Type: macro_line | Long-term Yield %: 2.515 (2026-04-01) | Range: 0.015–2.515 | Trend(6pt): 0.015,0.24,0.66,1.245,2.345,2.515

Japan 10Y Yield (3y) | Type: macro_line | Long-term Yield %: 2.515 (2026-04-01) | Range: 0.015–2.515 | Trend(6pt): 0.015,0.24,0.66,1.245,2.345,2.515

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Q1 GDP annualized final rose 1.8% versus 1.3% consensus, with quarter-over-quarter growth at 0.5%.

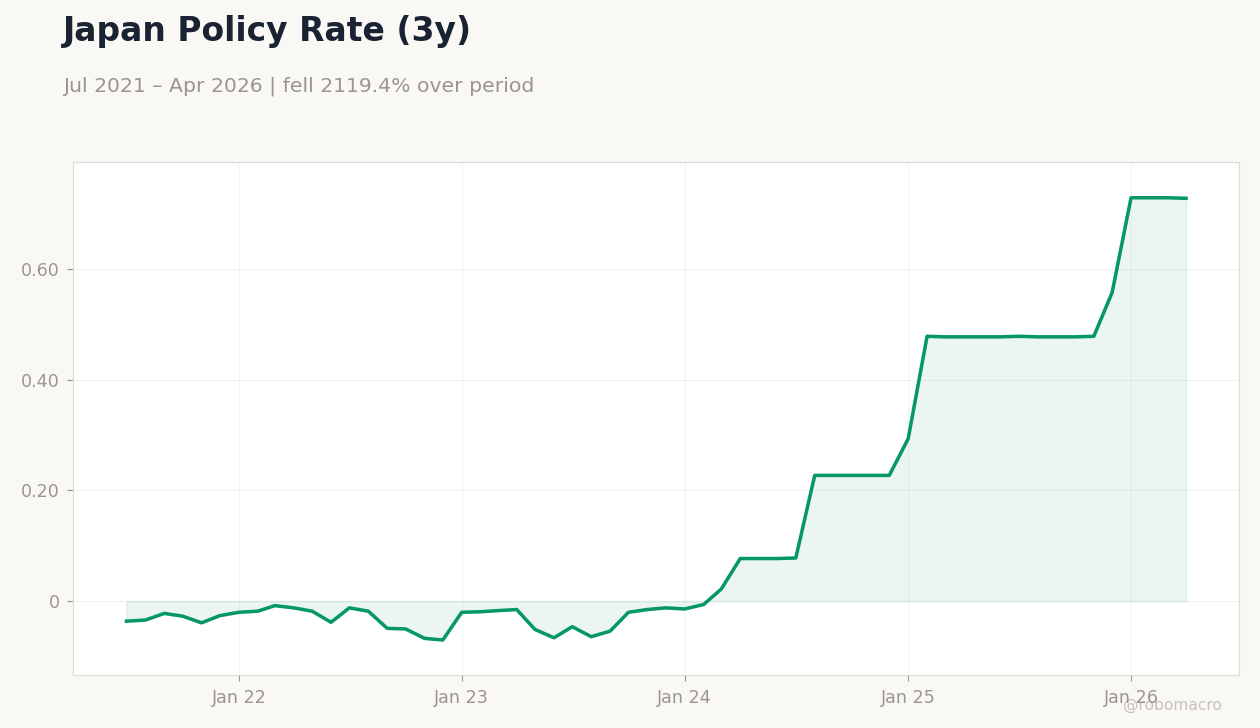

- Real wages advanced for a fourth straight month, reinforcing expectations for further Bank of Japan tightening.

- Nikkei 225 fell 1.31% while the 10-year JGB yield climbed 7.25% to 2.52%.

Yesterday's Recap

Japan’s Q1 GDP growth beat forecasts on stronger domestic demand and exports, lifting annualized final reading to 1.8% and quarter-over-quarter pace to 0.5%. The current account surplus printed at 3.907 trillion yen, exceeding consensus. Equity markets sold off as the Nikkei 225 dropped 1.31% to 66,588.12 amid profit-taking in technology shares.

The 10-year government bond yield surged 7.25% to 2.52%, reflecting repricing of rate-hike odds. USD/JPY edged 0.11% higher to 160.16 while EUR/JPY declined 0.56%. Real wage data released alongside GDP showed continued gains, supporting household spending.

Market participants interpreted the figures as validation for policy normalization despite lingering external risks.

The Day Ahead

No major Japanese data releases are scheduled for the next two sessions. Attention turns to the Bank of Japan’s June policy meeting and any fresh Summary of Opinions. Traders will monitor yen intervention signals from officials after recent Treasury sales reports.

Global risk sentiment and U.S. Treasury moves may influence JGB curves and currency flows. Bank lending figures already released showed stronger-than-expected credit growth, adding to hawkish sentiment.

Other Economic Notes

Rising real wages for four consecutive months provide the wage-price momentum the Bank of Japan has sought before further tightening. Cash earnings rebounded, aligning with former Governor Kuroda’s recent comments that wages now outpace prices. Oil price increases flagged by BofA could lift headline inflation and reinforce the case for additional rate adjustments.

The $8 trillion JGB market remains sensitive to any shift in yield-curve control parameters.

Global Macro News

Reports indicate Japan sold U.S. Treasuries to finance yen intervention, pressuring global bond markets. The yen’s failure to strengthen despite positive domestic data has revived concerns over carry-trade unwinds.

<i>↓ p.2</i>