Japan Macro Daily(Beta Mode)

Ueda's Hospitalization Clouds BoJ June Meeting

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 65,416.63 | +2.17% |

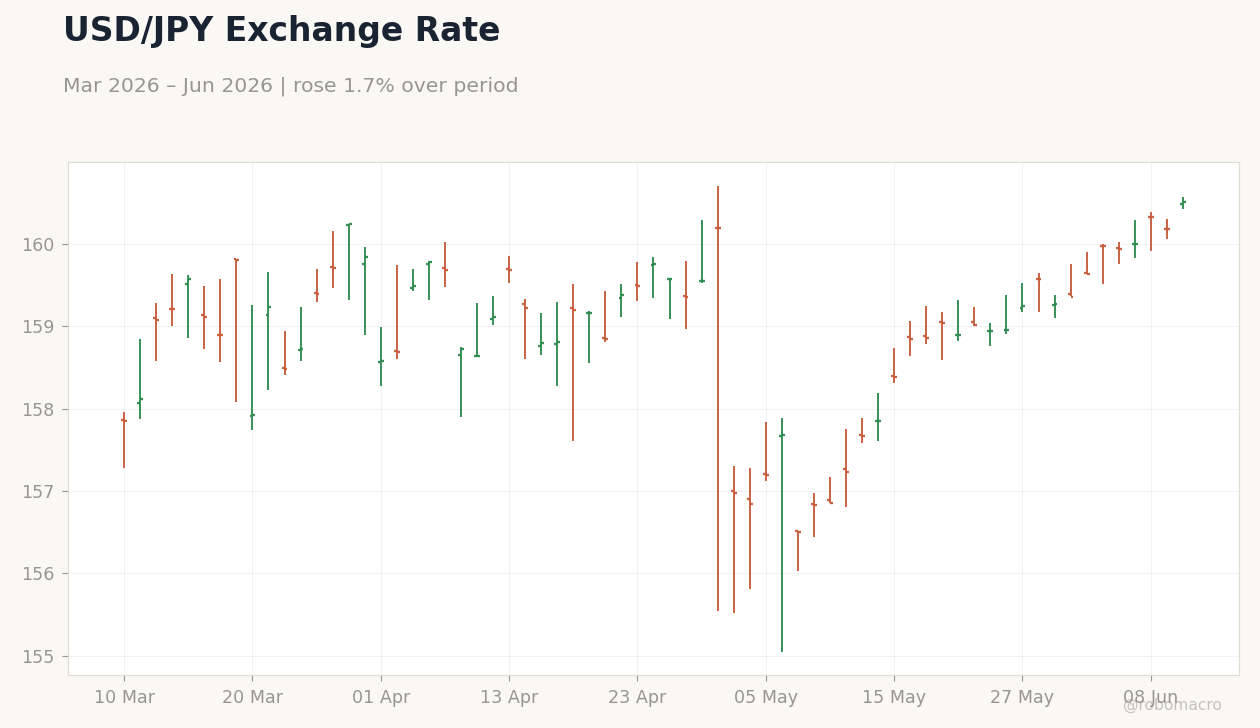

| USD/JPY | 160.53 | +0.22% |

| EUR/JPY | 185.09 | +0.24% |

| GBP/JPY | 214.38 | +0.38% |

| Gold | 4,094.10 | -3.89% |

| Brent Crude | 94.71 | +3.56% |

| Bitcoin | 61,165.98 | -0.78% |

| Japan 2Y Govt Yield | 0.73% | -0.14% |

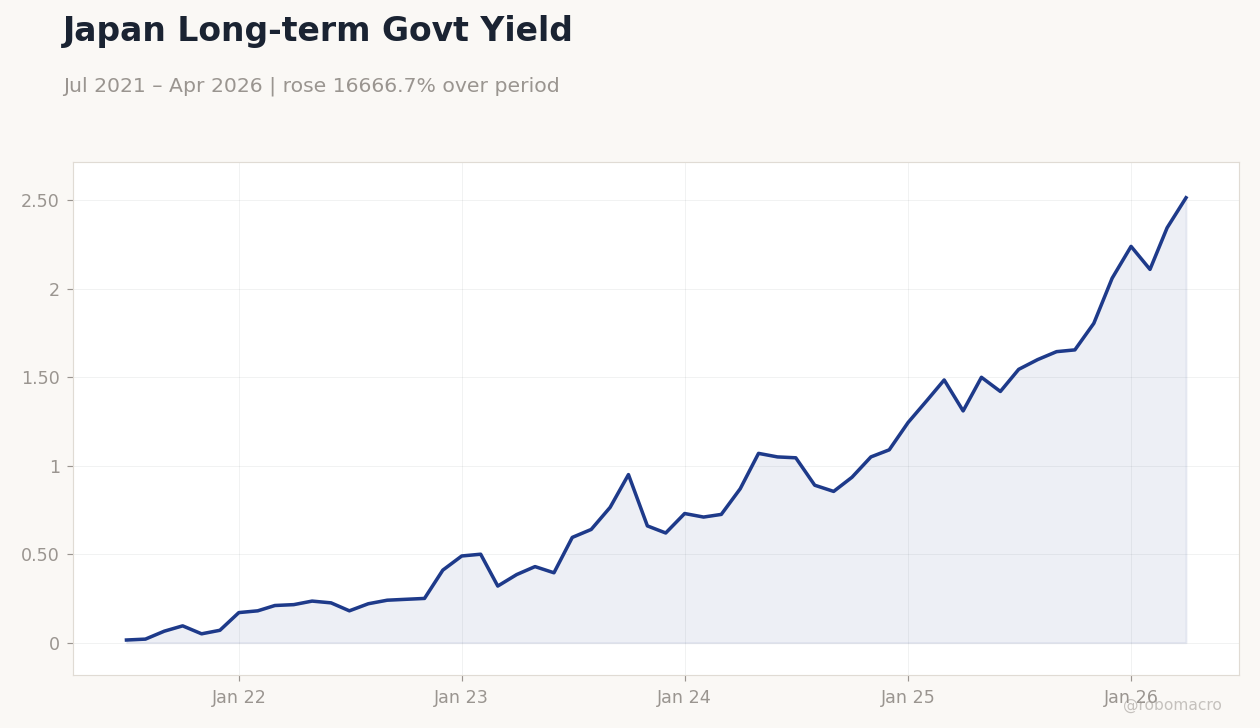

| Japan 10Y Govt Yield | 2.52% | +7.25% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan Long-term Govt Yield | Type: macro_line | 10Y Yield %: 2.515 (2026-04-01) | Range: 0.015–2.515 | Trend(6pt): 0.015,0.24,0.66,1.245,2.345,2.515

Japan Long-term Govt Yield | Type: macro_line | 10Y Yield %: 2.515 (2026-04-01) | Range: 0.015–2.515 | Trend(6pt): 0.015,0.24,0.66,1.245,2.345,2.515

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BoJ Governor Ueda hospitalized, expected to miss June policy meeting amid yen at 160.53.

- Nikkei 225 rises 2.17% to 65,416.63 while 10-year JGB yield jumps 7.25% to 2.52%.

- Markets price continued BoJ tightening bets despite policy uncertainty from leadership absence.

Yesterday's Recap

Markets digested news that Bank of Japan Governor Kazuo Ueda was hospitalized and will miss the June monetary policy meeting. USD/JPY climbed 0.22% to 160.53 while EUR/JPY and GBP/JPY posted modest gains. The Nikkei 225 advanced 2.17% to 65,416.63 on risk appetite and yen softness.

Japan 10-year government yields surged 7.25% to 2.52% whereas the 2-year yield eased 0.14% to 0.73%. Brent crude rose 3.56% to 94.71 while gold fell 3.89%. No economic data were released.

Renewed warnings from Tokyo failed to arrest yen depreciation. Prime Minister statements stressed defending the yen via economic strengthening rather than fresh intervention. PPI surprises lifted tightening probabilities and supported yen-upside scenarios.

Scotiabank flagged persistent bearish yen pressure even after any future hike. Citi highlighted expectations for a near-term adjustment on yen weakness.

The Day Ahead

Attention centers on the June BoJ meeting now in doubt without Governor Ueda. Traders will monitor any statements from Deputy Governor or other board members. Yen intervention rhetoric from the Prime Minister may continue to influence flows.

Global risk sentiment and U.S. data releases could affect USD/JPY direction. JGB purchase operations remain on schedule and may anchor longer-term yields.

Economic securitization tied to regional tensions adds fiscal pressure on public finances. Markets await clarity on whether the leadership gap delays normalization steps.

Other Economic Notes

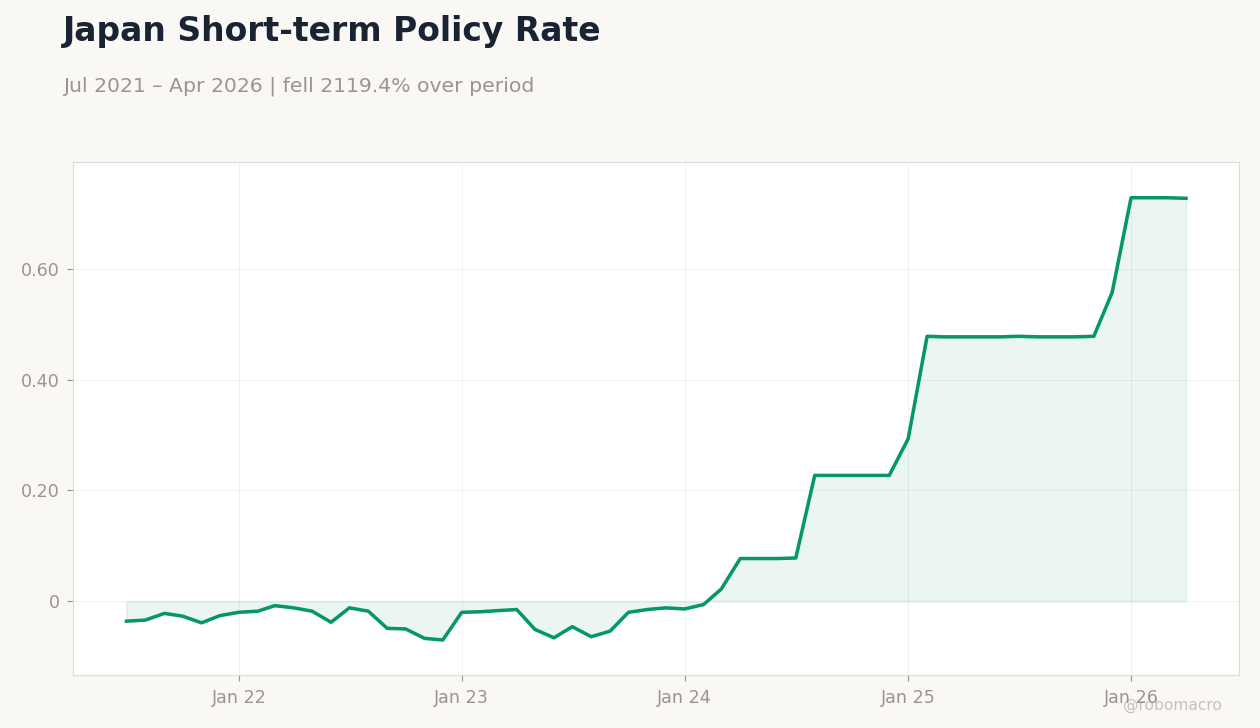

Persistent yen weakness at 160.53 raises imported inflation risks despite the verified BoJ policy rate of 0.73%. Former officials continue to flag possible rate adjustments later in the year. Toyota’s May global vehicle sales beat estimates, signaling resilient demand.

No senior BoJ speakers are scheduled. The verified Japan CPI YoY figure remains the older benchmark at -0.50%. Finance Ministry comments reiterated that excessive yen moves are undesirable.