Japan Macro Daily(Beta Mode)

BoJ Lifts Rate to 1% as Nikkei Tops 69,000

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 69,317.50 | +4.99% |

| USD/JPY | 160.34 | +0.07% |

| EUR/JPY | 186.25 | +0.29% |

| GBP/JPY | 215.29 | +0.16% |

| Gold | 4,353.80 | +0.60% |

| Brent Crude | 79.40 | -4.53% |

| Bitcoin | 65,809.34 | -0.72% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

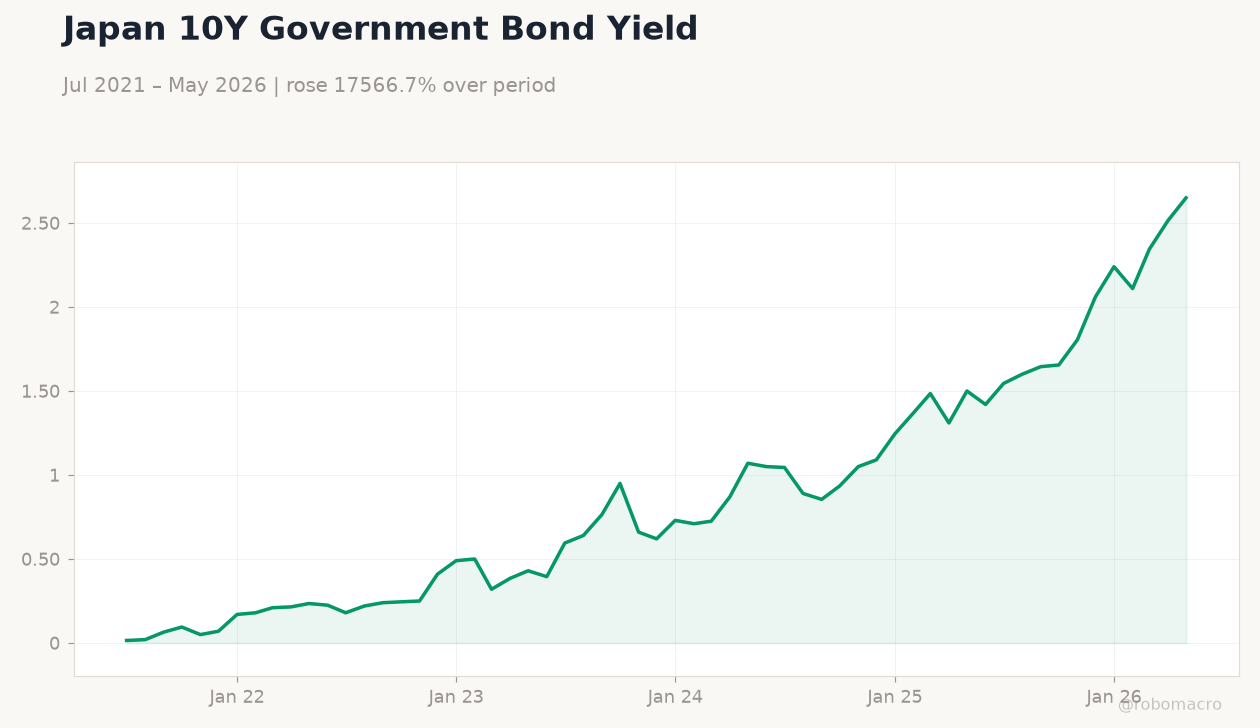

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

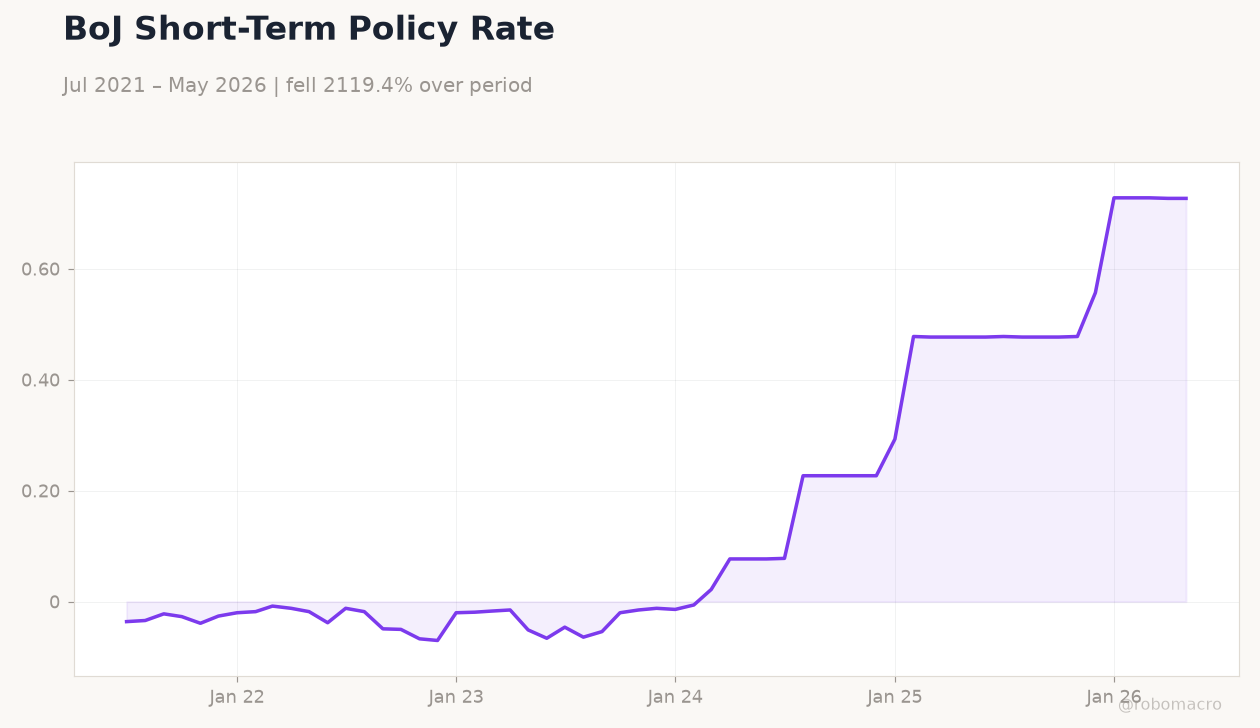

| BoJ Interest Rate Decision | 0.75 | 1 | 1 |

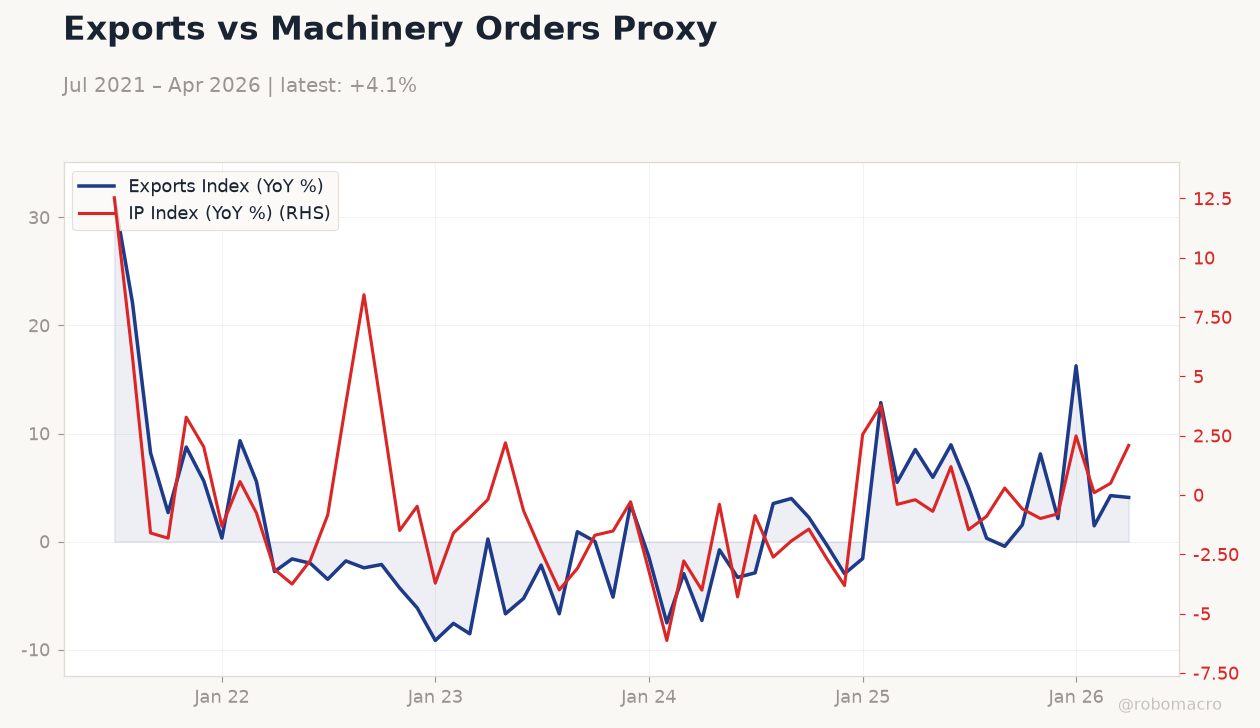

Exports vs Machinery Orders Proxy | Type: macro_line | Exports Index: 4.085 (2026-04-01) | Range: -9.156–31.82 | Trend(6pt): 31.82,-2.434,-5.144,-1.575,4.253,4.085 | IP Index: 2.092 (2026-04-01) | Range: -6.13–12.53 | Trend(6pt): 12.53,8.444,-1.517,2.554,0.4946,2.092

Exports vs Machinery Orders Proxy | Type: macro_line | Exports Index: 4.085 (2026-04-01) | Range: -9.156–31.82 | Trend(6pt): 31.82,-2.434,-5.144,-1.575,4.253,4.085 | IP Index: 2.092 (2026-04-01) | Range: -6.13–12.53 | Trend(6pt): 12.53,8.444,-1.517,2.554,0.4946,2.092

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 301,900m | -564,600m | 15:50 |

| Exports Year-over-Year | 14.80 | 16.20 | 15:50 |

| Machinery Orders Month-over-Month | -9.40 | 0.90 | 15:50 |

| Machinery Orders Year-over-Year | 5.90 | 9.30 | 15:50 |

| Thursday (2026-06-18) | |||

| Inflation Rate Year-over-Year | 1.40 | - | 15:30 |

| Core Inflation Rate Year-over-Year | 1.40 | 1.40 | 15:30 |

| BoJ Monetary Policy Meeting Minutes | - | - | 15:50 |

- BoJ raises policy rate to 1%, the highest level since 1995, citing persistent inflation risks

- Nikkei 225 surges 4.99% to close above 69,000 for the first time on yen carry-trade revival

- Japan 10Y yield jumps 5.37% to 2.65% while USD/JPY holds steady near 160.34

Yesterday's Recap

The Bank of Japan delivered a 25 bp hike, lifting the policy rate from 0.75% to 1.0% and marking the highest level in three decades. Equity markets responded sharply, with the Nikkei 225 advancing 4.99% to 69,317.50 as short yen positions expanded to nine-year highs. The 10-year JGB yield climbed 5.37% to 2.65%, reflecting repricing of normalisation prospects, while the 2-year yield remained anchored at 0.73%.

USD/JPY edged 0.07% higher to 160.34, with cross-yen pairs showing modest gains amid thin follow-through. Brent crude fell 4.53% to 79.40 as risk sentiment rotated toward equities. Bitcoin declined 0.72% to 65,809.34 despite the broader risk-on tone.

The move aligns with the prior BoJ rate at 0.75% before the June adjustment.

The Day Ahead

Trade balance, exports, and machinery orders data release at 15:50 ET today, with consensus pointing to a swing to a 564.6 bn yen deficit and exports rising 16.2% y/y. Machinery orders are expected to rebound 0.9% m/m after last month’s 9.4% drop. Thursday brings May inflation prints and the June BoJ policy meeting minutes, both carrying high market impact.

The minutes will clarify the committee’s assessment of wage and price dynamics following the latest tightening step. No senior BoJ speakers are scheduled before the releases.

Other Economic Notes

Yen short positioning has reached elevated levels, reviving carry-trade flows that support domestic equities but keep external balances under pressure. Services activity rebounded last month, reinforcing the case for further gradual tightening. Corporate share buybacks, including Toshiba’s 120 bn yen programme, provide additional equity support amid policy normalisation.

Fiscal consolidation signals from the Ishiba administration remain loosely coordinated with monetary tightening.