Japan Macro Daily(Beta Mode)

BoJ Lifts Rate to 1% as Exports Beat Forecasts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 69,404.50 | +0.13% |

| USD/JPY | 160.63 | +0.25% |

| EUR/JPY | 184.70 | -0.54% |

| GBP/JPY | 213.52 | -0.85% |

| Gold | 4,275.30 | -1.28% |

| Brent Crude | 78.63 | -0.42% |

| Bitcoin | 64,381.93 | -1.86% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

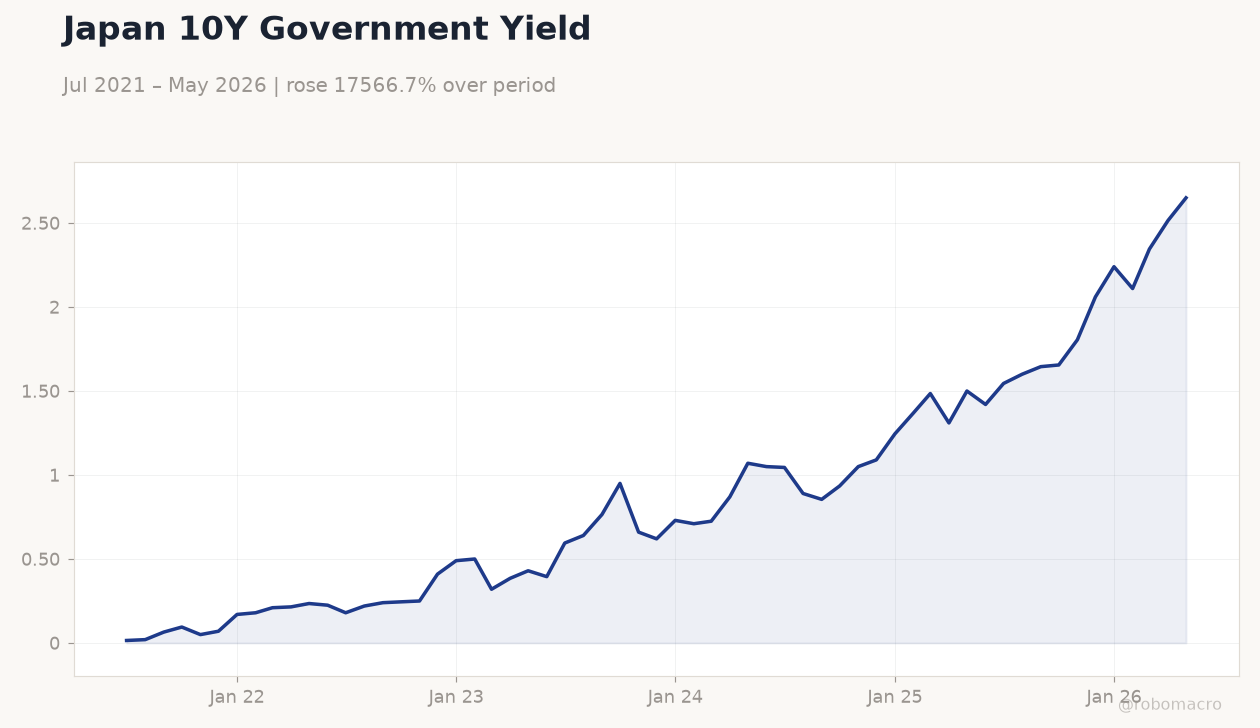

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

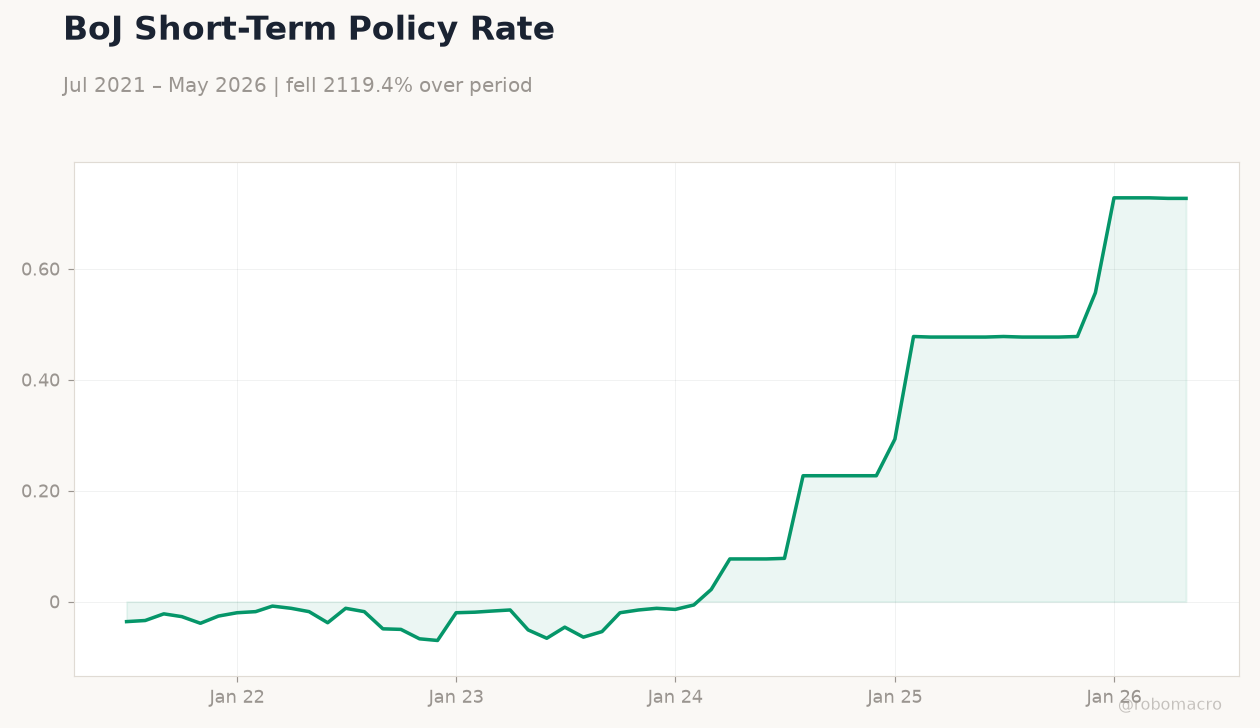

| BoJ Interest Rate Decision | 0.75 | 1 | 1 |

| Trade Balance | 299,300m | -564,600m | -378,700m |

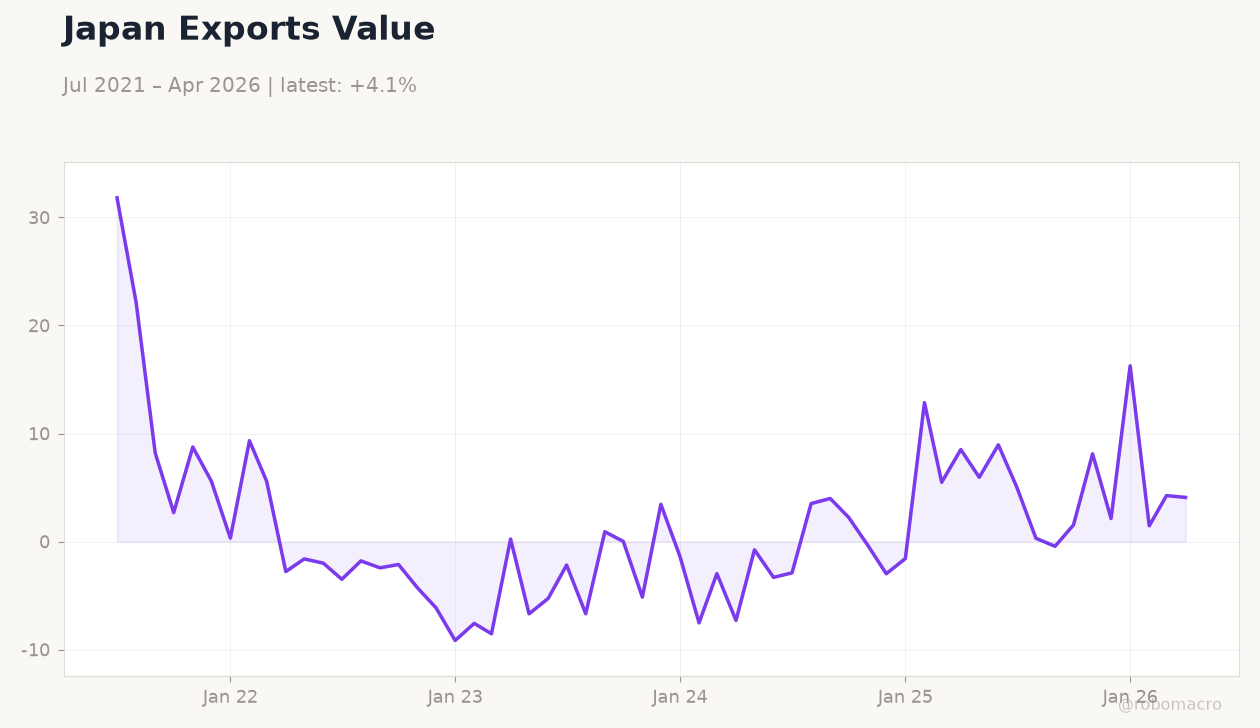

| Exports Year-over-Year | 14.80 | 16.20 | 17 |

| Machinery Orders Month-over-Month | -9.40 | 0.90 | 8.70 |

| Machinery Orders Year-over-Year | 5.90 | 9.30 | 15.60 |

Japan 10Y Government Yield | Type: macro_line | %: 2.65 (2026-05-01) | Range: 0.015–2.65 | Trend(6pt): 0.015,0.24,0.66,1.245,2.345,2.65

Japan 10Y Government Yield | Type: macro_line | %: 2.65 (2026-05-01) | Range: 0.015–2.65 | Trend(6pt): 0.015,0.24,0.66,1.245,2.345,2.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-06-18) | |||

| Inflation Rate Year-over-Year | 1.40 | - | 15:30 |

| Core Inflation Rate Year-over-Year | 1.40 | 1.40 | 15:30 |

| BoJ Monetary Policy Meeting Minutes | - | - | 15:50 |

- BoJ lifts policy rate to 1.0%, the highest level since 1995, on elevated inflation risks

- Exports rise 17% YoY while trade balance narrows to -378.7 billion yen, beating consensus

- Nikkei 225 edges up 0.13% to 69,404.50 as 10-year JGB yield climbs 5.37% to 2.65%

Yesterday's Recap

The Bank of Japan raised its policy rate by 25 basis points to 1.0% at the June meeting, aligning with consensus and marking the highest level in three decades. Trade data released the same day showed exports expanding 17% year-over-year, above the 16.2% forecast, while the trade balance came in at -378.7 billion yen versus the expected -564.6 billion yen. Machinery orders posted sharp rebounds, rising 8.7% month-over-month and 15.6% year-over-year.

The Nikkei 225 closed 0.13% higher at 69,404.50, with USD/JPY advancing 0.25% to 160.63. The 10-year JGB yield surged 5.37% to 2.65% while the 2-year yield held steady at 0.73%. Market reaction showed limited yen strength despite the hawkish policy shift, as participants focused on the upcoming FOMC decision.

The Day Ahead

June national CPI figures and core inflation data are scheduled for release at 15:30 ET, with markets expecting core inflation to hold at 1.4% year-over-year. The Bank of Japan will also publish minutes from its latest monetary policy meeting at 15:50 ET, offering further detail on the committee’s assessment of inflation risks. Traders will monitor any revisions to the BoJ’s growth and price forecasts.

Yen volatility may increase ahead of the FOMC outcome later in the global session. Domestic equity futures point to a cautious open following the record close.

Other Economic Notes

Strong machinery orders signal improving capital expenditure momentum that could support the BoJ’s inflation outlook. Persistent yen weakness near 160.63 continues to import price pressures, reinforcing the case for gradual policy normalisation. The government’s alignment with the central bank on the rate path reduces political friction around further tightening steps.

Export resilience offsets some concerns over global demand slowdowns, keeping the external sector supportive of growth.

Global Macro News

The yen gained modestly against the euro and pound but remained under pressure versus the dollar despite the BoJ move, reflecting expectations of steady Fed policy. <i>↓ p.2</i>