Japan Macro Daily(Beta Mode)

BoJ Lifts Rate to 1% as Yen Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 69,902.25 | +0.72% |

| USD/JPY | 161.34 | +0.57% |

| EUR/JPY | 184.94 | -0.70% |

| GBP/JPY | 213.10 | -0.24% |

| Gold | 4,228.60 | -2.99% |

| Brent Crude | 79.33 | -0.28% |

| Bitcoin | 63,008.84 | -3.95% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

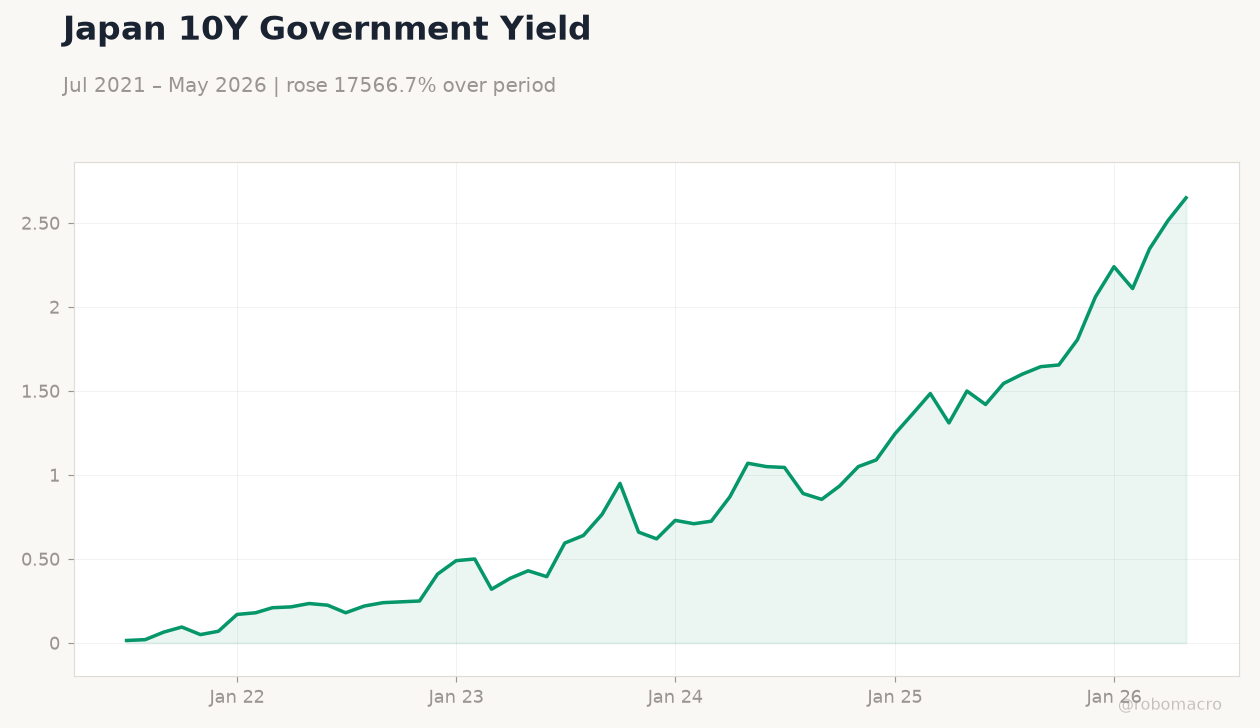

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

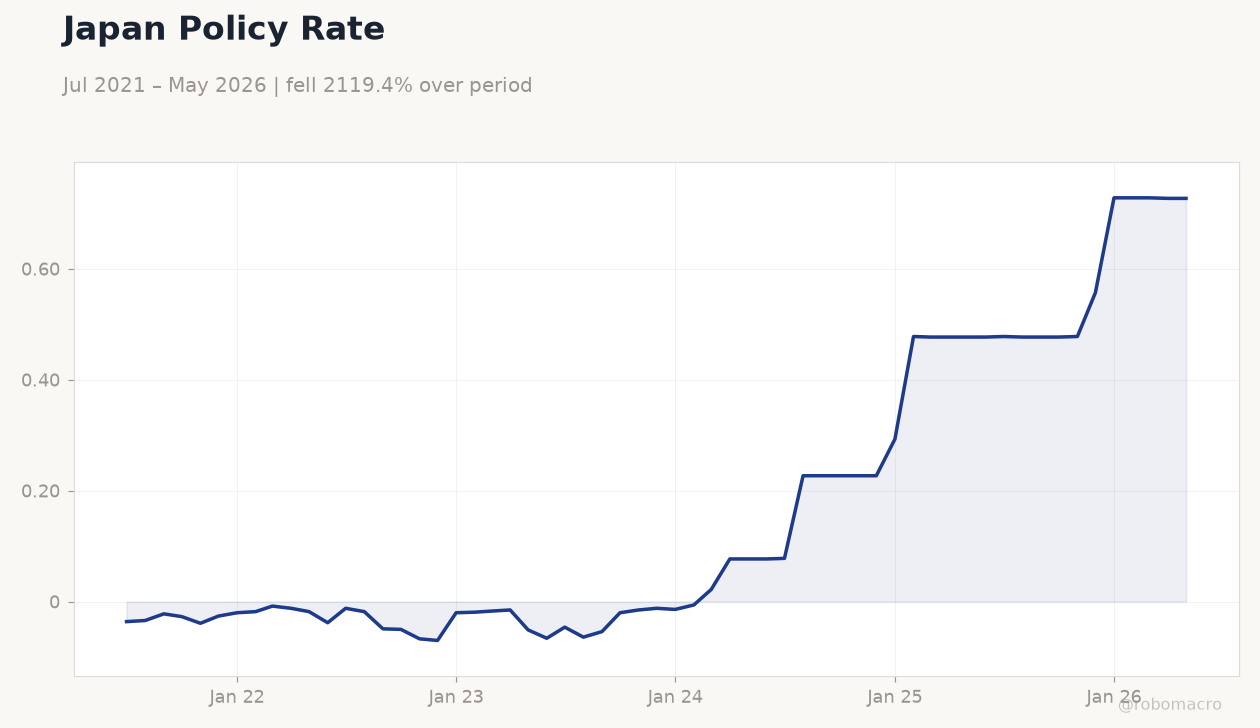

| BoJ Interest Rate Decision | 0.75 | 1 | 1 |

| Trade Balance | 299,300m | -564,600m | -378,700m |

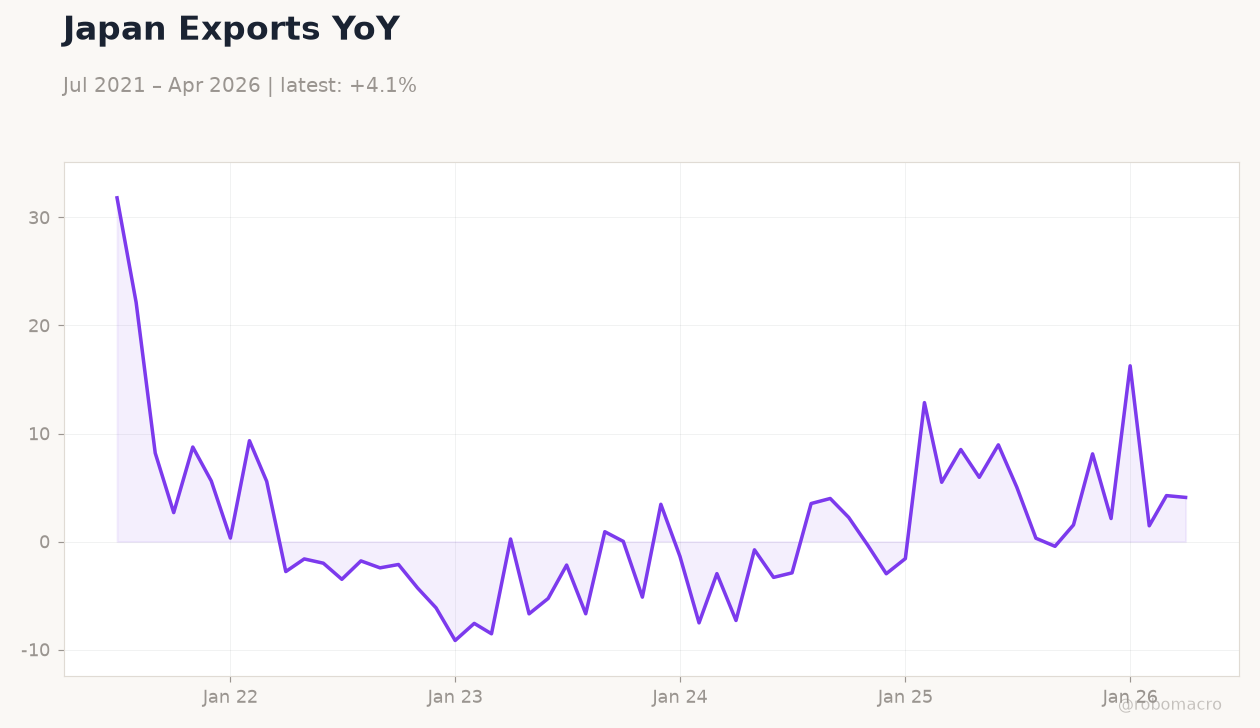

| Exports Year-over-Year | 14.80 | 16.20 | 17 |

| Machinery Orders Month-over-Month | -9.40 | 0.90 | 8.70 |

| Machinery Orders Year-over-Year | 5.90 | 9.30 | 15.60 |

Japan Policy Rate | Type: macro_line | Policy Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Japan Policy Rate | Type: macro_line | Policy Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.40 | - | 15:30 |

| Core Inflation Rate Year-over-Year | 1.40 | 1.40 | 15:30 |

| BoJ Monetary Policy Meeting Minutes | - | - | 15:50 |

- Bank of Japan raises policy rate to 1%, the highest since 1995, confirming further normalisation.

- Trade balance narrows to a JPY 378.7 billion deficit while exports rise 17% year-over-year.

- Yen weakens to 161.34 against the dollar as 10-year JGB yields climb to 2.65%.

Yesterday's Recap

The Bank of Japan delivered its widely expected 25 basis point hike, moving the policy rate from 0.75% to 1%. Trade data showed a smaller-than-forecast deficit of JPY 378.7 billion after imports surged on the weaker currency. Exports expanded 17% year-over-year, beating consensus, while machinery orders jumped 8.7% month-over-month and 15.6% year-over-year.

Equity markets responded positively, with the Nikkei 225 closing 0.72% higher at 69,902.25. The yen extended losses, pushing USD/JPY to 161.34, while the 10-year government bond yield rose sharply to 2.65%. Intervention warnings from officials failed to stem the sell-off in the currency.

The Day Ahead

Markets will focus on the June CPI release due at 15:30 ET, with headline and core inflation both expected near 1.4%. The Bank of Japan will publish the minutes of the latest policy meeting at 15:50 ET, offering fresh insight into the committee’s tolerance for further tightening. Traders will parse any references to additional rate moves or adjustments to yield-curve-control parameters.

Yen volatility is likely to remain elevated ahead of the data and minutes.

Other Economic Notes

The move to a 1% policy rate marks the end of Japan’s ultra-loose era and raises borrowing costs across the economy. Higher yields are attracting foreign inflows into JGBs while pressuring domestic equity valuations. Persistent yen depreciation continues to lift import prices, complicating the inflation outlook and keeping intervention risks alive.

Policymakers now face the dual challenge of supporting growth while anchoring long-term inflation expectations.

Global Macro News

The Federal Reserve’s hawkish stance continues to widen interest-rate differentials, supporting further dollar strength against the yen. Treasury yields remain elevated, reinforcing carry-trade flows out of Japan. European and UK central banks held rates steady this week, limiting additional pressure on cross-yen pairs.

<i>↓ p.2</i>