Japan Macro Daily(Beta Mode)

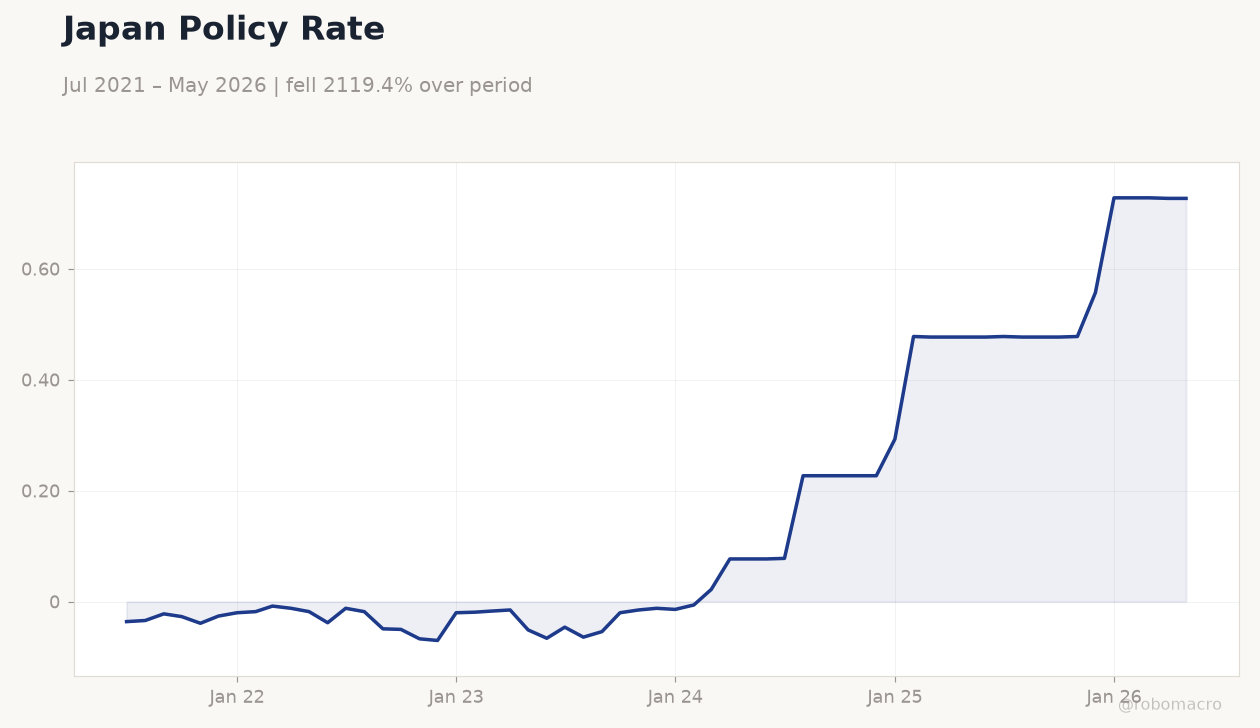

Yen Weakens to 161 Despite BoJ Rate at 0.73%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 71,250.06 | +0.28% |

| USD/JPY | 161.24 | -0.03% |

| EUR/JPY | 184.83 | +0.01% |

| GBP/JPY | 212.64 | -0.14% |

| Gold | 4,172.90 | -1.21% |

| Brent Crude | 80.59 | +0.93% |

| Bitcoin | 63,775.36 | -0.72% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

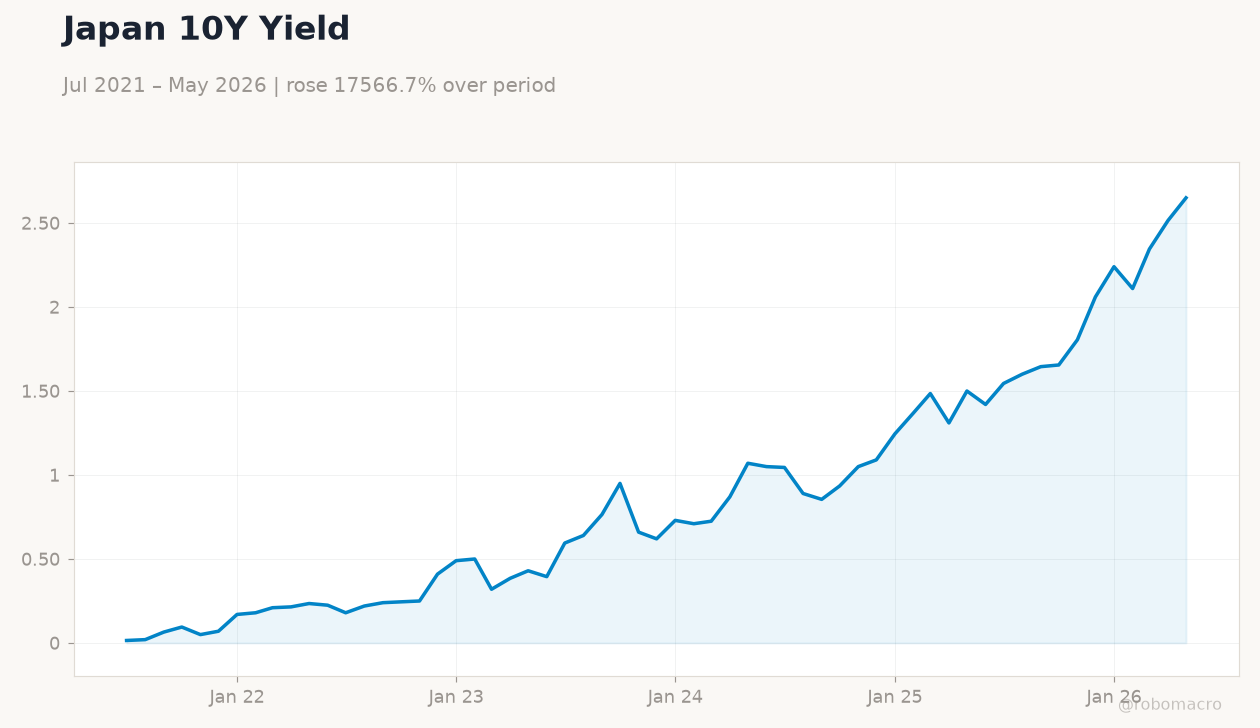

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Japan Policy Rate | Type: macro_line | Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Japan Policy Rate | Type: macro_line | Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-23) | |||

| S&P Global Manufacturing PMI Flash | 54.50 | 54.50 | 20:30 |

| S&P Global Services PMI Flash | 50 | - | 20:30 |

| BoJ Summary of Opinions | - | - | 19:50 |

| Wednesday (2026-06-24) | |||

| BoJ Himino Speech | - | - | 02:40 |

| BOJ Gov Ueda Speech | - | - | 16:00 |

| Thursday (2026-06-25) | |||

| BOJ Tamura Speech | - | - | 21:00 |

| Sunday (2026-06-28) | |||

- USD/JPY holds at 161.24 near 40-year lows despite recent BoJ policy rate at 0.73%

- Nikkei 225 rises 0.28% to 71,250 while 10-year JGB yields jump 5.37% to 2.65%

- Flash PMIs and multiple BoJ speeches headline a data-light week focused on policy signals

Yesterday's Recap

Markets digested fresh evidence that BoJ policy settings have failed to arrest yen depreciation, with USD/JPY closing at 161.24. The Nikkei 225 advanced 0.28% to 71,250.06 as exporters benefited from the weak currency. Ten-year JGB yields surged 5.37% to 2.65%, reflecting repricing of future policy normalisation.

Japan megabanks are set to distribute a record 2 trillion yen in dividends, supporting equity sentiment. No major data prints occurred on 20 June, leaving price action driven by ongoing yen weakness and global dollar strength. Gold fell 1.21% while Brent crude rose 0.93%.

Ueda’s hospital discharge removed one near-term uncertainty around BoJ leadership continuity.

The Day Ahead

June S&P Global Manufacturing and Services PMI flashes are due at 20:30 ET on 22 June, with manufacturing expected to hold at 54.5. The BoJ Summary of Opinions follows on 23 June, offering the first detailed read on the latest policy meeting. Governor Ueda speaks on 24 June alongside Deputy Governor Himino, both events carrying high market impact.

Tamura is also scheduled to address audiences later that day. Retail sales data arrive on 28 June, providing a fresh gauge of consumer momentum. Focus will centre on whether officials flag additional rate adjustments this year.

Other Economic Notes

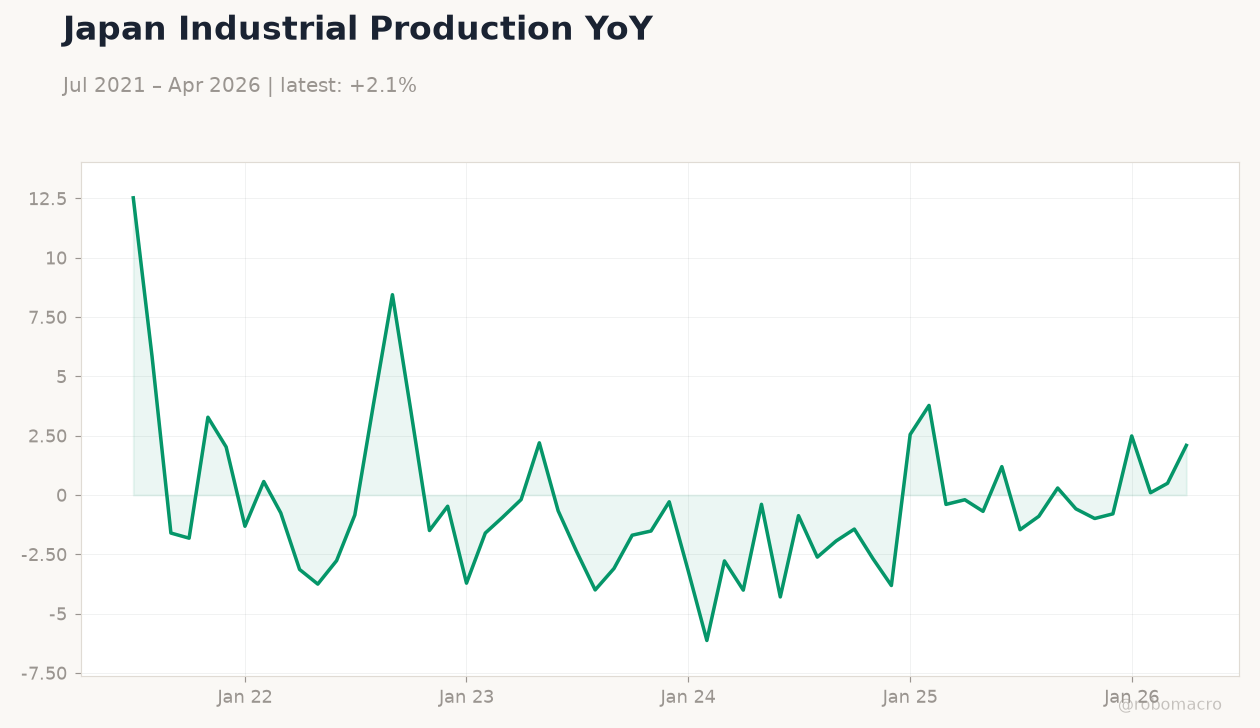

Japan’s inflation remains stable following the latest BoJ policy adjustment, with energy subsidies limiting pass-through to headline prints. Industrial production rebounded in May, confirming a recovery in autos and electronics output. Megabank dividend payouts at record levels underscore healthy corporate balance sheets amid policy normalisation.

Yen depreciation continues to outpace the cumulative effect of interventions and the 0.73% policy rate. Broader price pressures appear contained enough to allow gradual rather than aggressive further adjustments.