Japan Macro Daily(Beta Mode)

Yen Nears 39-Year Low Despite BoJ Hike

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 71,250.06 | +0.28% |

| USD/JPY | 161.50 | +0.13% |

| EUR/JPY | 184.51 | -0.29% |

| GBP/JPY | 213.95 | +0.48% |

| Gold | 4,210.10 | -0.33% |

| Brent Crude | 77.96 | -2.37% |

| Bitcoin | 64,378.60 | +1.80% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

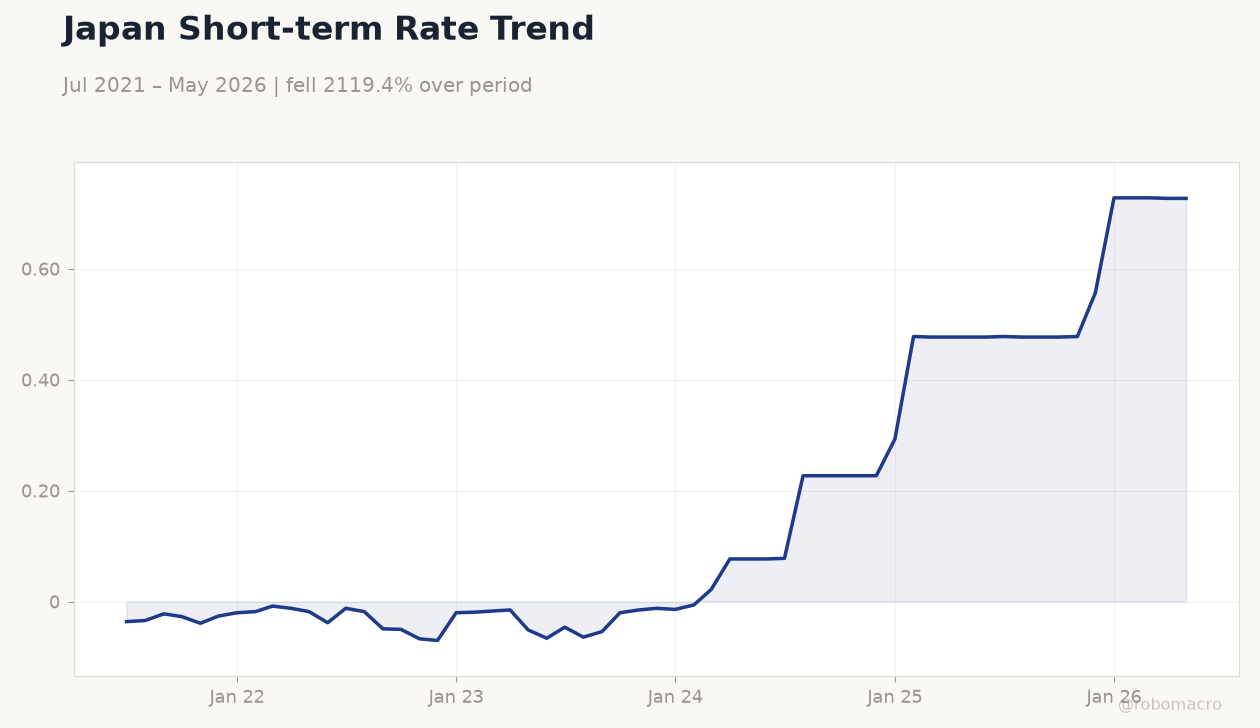

Japan Short-term Rate Trend | Type: macro_line | Policy rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Japan Short-term Rate Trend | Type: macro_line | Policy rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 54.50 | 54.50 | 16:30 |

| S&P Global Services PMI Flash | 50 | - | 16:30 |

| Tuesday (2026-06-23) | |||

| BoJ Summary of Opinions | - | - | 15:50 |

| Wednesday (2026-06-24) | |||

| BoJ Himino Speech | - | - | 22:40 |

| BOJ Gov Ueda Speech | - | - | 12:00 |

| BOJ Tamura Speech | - | - | 17:00 |

| Sunday (2026-06-28) | |||

| Retail Sales Year-over-Year | 2.10 | - | 15:50 |

- Yen approaches four-decade low at 161.50 versus dollar after latest BoJ tightening

- Nikkei 225 gains 0.28% while 10-year JGB yield rises 5.37% to 2.65%

- Markets watch today’s PMI flashes and upcoming BoJ Summary of Opinions

Yesterday's Recap

Japanese markets closed with the Nikkei 225 advancing 0.28% to 71,250.06 amid continued yen depreciation. USD/JPY climbed 0.13% to 161.50, extending its move toward levels last seen in the mid-1980s. The 10-year JGB yield increased sharply by 5.37% to 2.65%, reflecting ongoing repricing after the BoJ’s recent policy adjustment.

EUR/JPY fell 0.29% while GBP/JPY rose 0.48%, highlighting uneven cross-currency flows. No major data releases occurred on 21 June, leaving price action driven by overnight global positioning and intervention rhetoric from Tokyo officials. Japan megabanks are set to distribute a record 2 trillion yen in dividends, supporting equity sentiment.

Gold and Brent crude declined 0.33% and 2.37% respectively, offering little safe-haven support to the yen.

The Day Ahead

S&P Global Manufacturing and Services PMI flashes are scheduled for release at 16:30 ET today, with manufacturing expected to hold at 54.5. The BoJ will publish its Summary of Opinions tomorrow at 15:50 ET, providing the first detailed read on the latest policy meeting. Governor Ueda is slated to speak on 24 June, followed by Deputy Governor Himino and board member Tamura later that day.

Retail sales data arrive on 28 June. Traders will monitor any fresh verbal intervention signals from Finance Ministry officials given the yen’s proximity to historic lows.

Other Economic Notes

Japan’s CPI stood at -0.50% YoY. The verified BoJ policy rate stands at 0.73%. Former policymakers now project as many as two additional hikes by March 2027.

Record dividend payouts from major banks are expected to underpin domestic equity demand through the summer. Yen volatility continues to complicate carry-trade strategies involving the Australian dollar.

Global Macro News

The yen’s slide to near 39-year lows has prompted repeated warnings of possible intervention from Japanese authorities. Carry trades funded in yen have supported the Australian dollar, which posted gains against the Japanese currency. Global risk sentiment remains mixed as Bitcoin rises 1.80% while energy prices fall.

<i>↓ p.2</i>