Japan Macro Daily(Beta Mode)

Nikkei Climbs as PMI Beats Offset Yen Weakness

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 72,353.96 | +1.55% |

| USD/JPY | 161.48 | -0.06% |

| EUR/JPY | 183.82 | -0.43% |

| GBP/JPY | 213.07 | -0.45% |

| Gold | 4,128.30 | -1.28% |

| Brent Crude | 76.88 | -1.31% |

| Bitcoin | 62,400.45 | -2.43% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

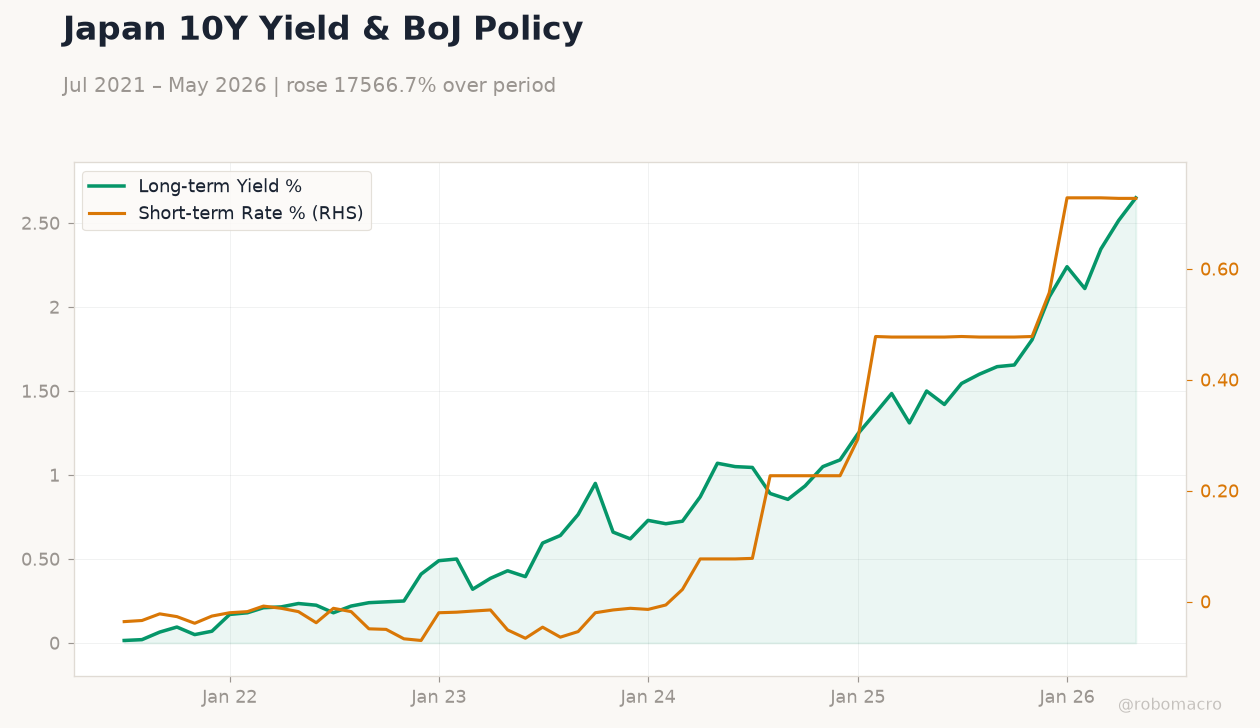

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 54.50 | 54.50 | 54.90 |

| S&P Global Services PMI Flash | 50 | - | 51.80 |

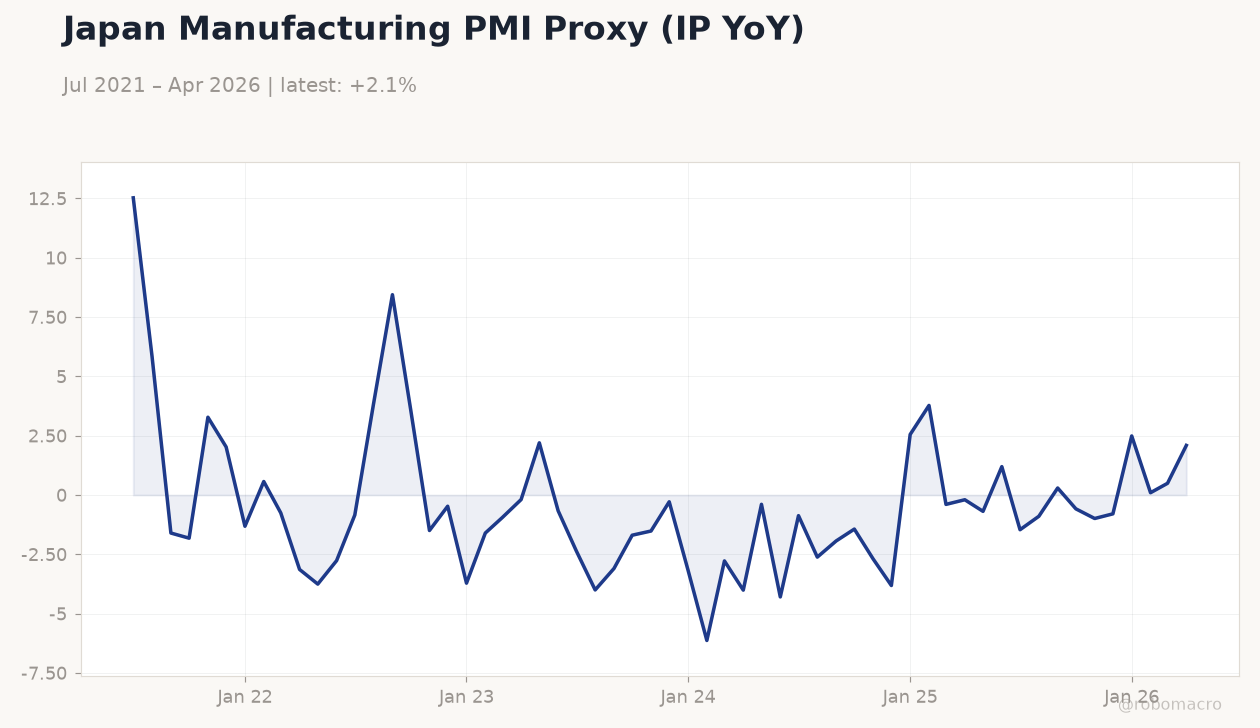

Japan Manufacturing PMI Proxy (IP YoY) | Type: macro_line | Industrial Production YoY %: 2.092 (2026-04-01) | Range: -6.13–12.53 | Trend(6pt): 12.53,8.444,-1.517,2.554,0.4946,2.092

Japan Manufacturing PMI Proxy (IP YoY) | Type: macro_line | Industrial Production YoY %: 2.092 (2026-04-01) | Range: -6.13–12.53 | Trend(6pt): 12.53,8.444,-1.517,2.554,0.4946,2.092

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoJ Summary of Opinions | - | - | 15:50 |

| Wednesday (2026-06-24) | |||

| BoJ Himino Speech | - | - | 22:40 |

| BOJ Gov Ueda Speech | - | - | 12:00 |

| BOJ Tamura Speech | - | - | 17:00 |

| Sunday (2026-06-28) | |||

| Retail Sales Year-over-Year | 2.10 | - | 15:50 |

- Japan’s flash PMIs beat expectations with manufacturing at 54.9 and services at 51.8, reinforcing modest expansion.

- Nikkei 225 rose 1.55% to 72,353.96 while the 10-year JGB yield jumped 5.37% to 2.65%.

- USD/JPY held near 161.48 as markets priced BoJ normalisation risks against persistent US-Japan rate differentials.

Yesterday's Recap

S&P Global Manufacturing PMI Flash rose to 54.9 from 54.5, while Services PMI Flash climbed to 51.8 from 50.0, both exceeding forecasts and pointing to resilient domestic demand. Equity markets responded positively, lifting the Nikkei 225 by 1.55% to close at 72,353.96. The 10-year JGB yield surged 5.37% to 2.65%, reflecting repricing of policy normalisation, while the 2-year yield stayed at 0.73%.

USD/JPY eased just 0.06% to 161.48, with EUR/JPY and GBP/JPY declining 0.43% and 0.45% respectively. Gold fell 1.28% to 4,128.30 and Brent Crude dropped 1.31% to 76.88 amid broader risk-on flows. Bitcoin declined 2.43% to 62,400.45.

The data reinforced views that growth remains steady even as the yen tests multi-decade lows.

The Day Ahead

Markets will focus on the BoJ Summary of Opinions due at 15:50 JST today for fresh insights into rate-hike deliberations. Deputy Governor Himino speaks at 22:40 JST, followed by Governor Ueda at 12:00 JST and board member Tamura at 17:00 JST tomorrow. These high-impact appearances are expected to clarify the timing of further policy adjustments.

Retail Sales data scheduled for 28 June will provide the next consumption gauge. Traders will monitor yen intervention rhetoric alongside the speeches.

Other Economic Notes

The policy rate remains at 0.73%. Yen weakness continues to mask equity gains, with the currency hovering near long-term lows even after recent tightening steps. Intervention risks have risen as officials signal concern over excessive depreciation.

Broader themes include the wide US-Japan rate gap sustaining capital outflows and pressure on USD/JPY above 160.

Global Macro News

Global risk sentiment lifted equities while pressuring commodities, indirectly supporting Japanese exporters. US rate expectations remain elevated, widening the yield differential that keeps the yen vulnerable. European data showed flat German manufacturing PMI, weighing on EUR/JPY.

<i>↓ p.2</i>