Japan Macro Daily(Beta Mode)

BoJ Summary Backs Hikes as Yen Intervention Mounts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 69,788.38 | -3.55% |

| USD/JPY | 161.72 | +0.07% |

| EUR/JPY | 183.78 | -0.05% |

| GBP/JPY | 213.00 | -0.14% |

| Gold | 4,014.60 | -2.79% |

| Brent Crude | 73.11 | -5.15% |

| Bitcoin | 60,880.25 | -2.85% |

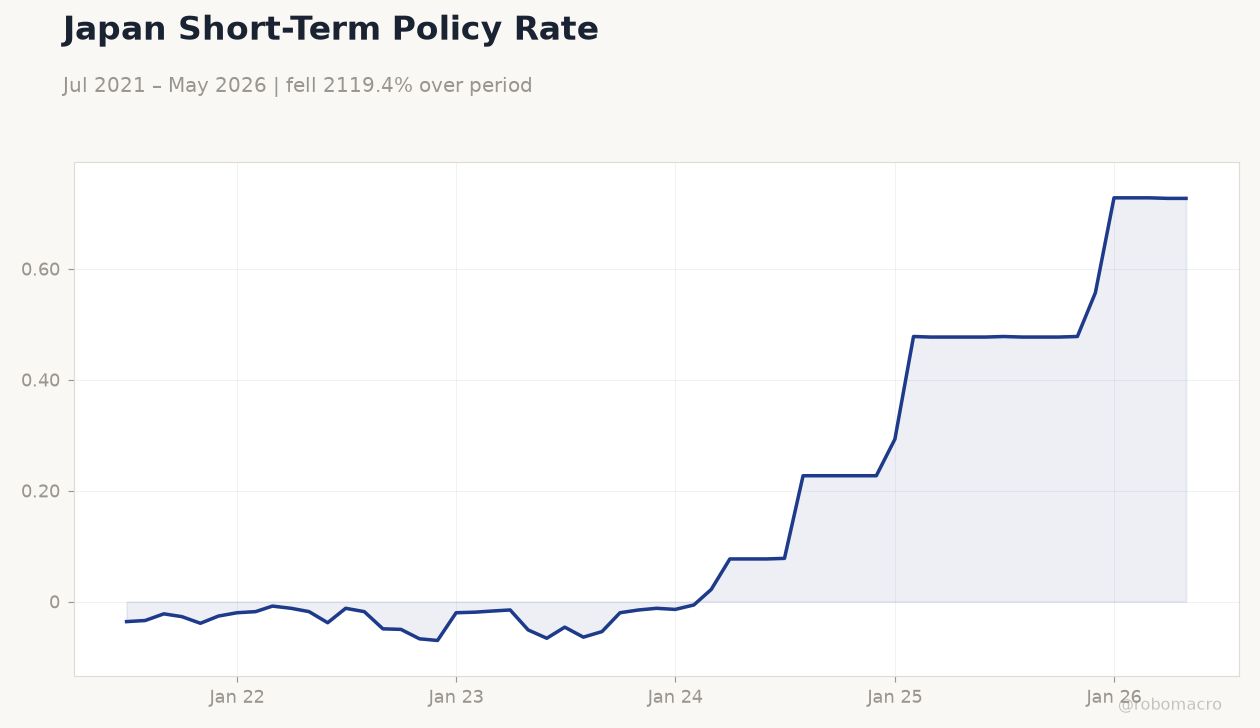

| Japan 2Y Govt Yield | 0.73% | +0.00% |

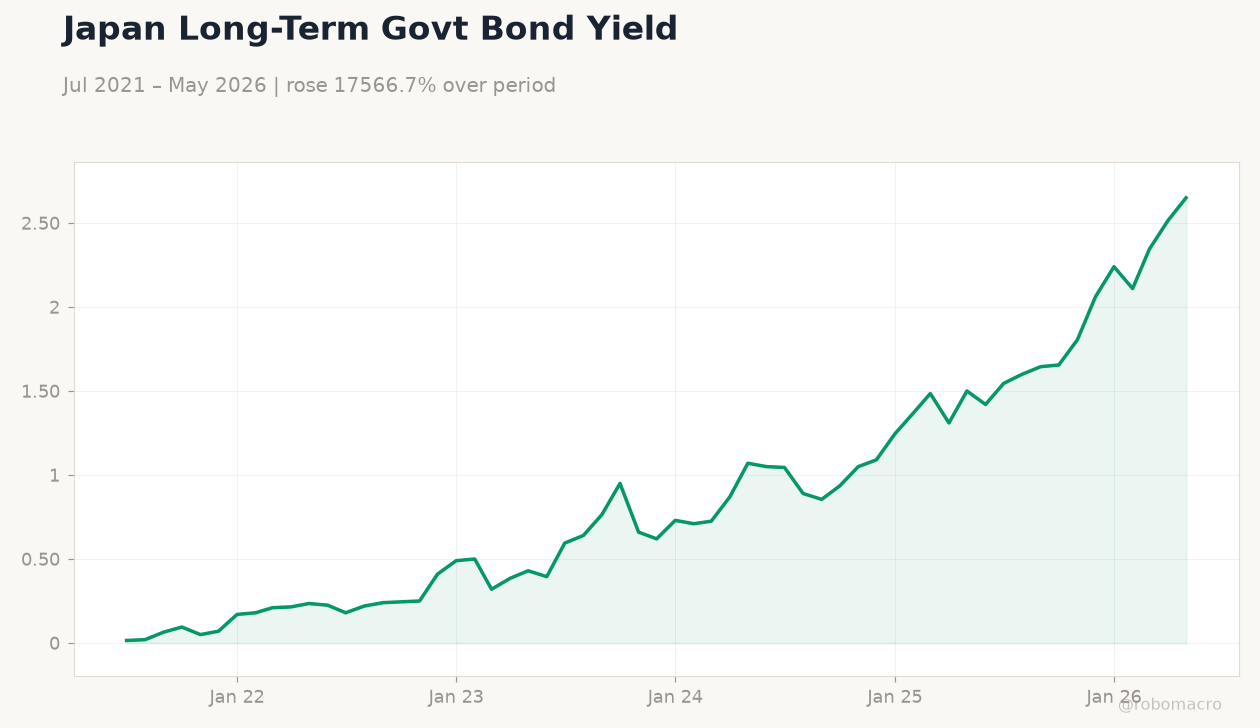

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 54.50 | 54.50 | 54.90 |

| S&P Global Services PMI Flash | 50 | - | 51.80 |

| BoJ Summary of Opinions | - | - | "" |

| BoJ Himino Speech | - | - | - |

| BOJ Gov Ueda Speech | - | - | - |

Japan Short-Term Policy Rate | Type: macro_line | Percent: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Japan Short-Term Policy Rate | Type: macro_line | Percent: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BOJ Tamura Speech | - | - | 17:00 |

| Sunday (2026-06-28) | |||

| Retail Sales Year-over-Year | 2.10 | - | 15:50 |

- BoJ Summary of Opinions shows multiple members urging further rate increases amid rising inflation risks.

- S&P Global manufacturing PMI rose to 54.9 and services PMI to 51.8 in June flash readings.

- Yen intervention confirmed with record spending last month while USD/JPY holds near 161.72.

Yesterday's Recap

Japan released stronger-than-expected June PMI data with manufacturing at 54.9 versus 54.5 prior and services jumping to 51.8 from 50.0. The BoJ published its Summary of Opinions from the latest meeting, highlighting calls for continued policy tightening. Deputy Governor Himino delivered remarks on the same day.

The Nikkei 225 fell 3.55 percent to 69,788.38 while the 10-year JGB yield climbed 5.37 percent to 2.65 percent. USD/JPY edged up 0.07 percent to 161.72 as intervention warnings failed to reverse the pair. The 2-year yield stayed at 0.73 percent, matching the current BoJ policy rate.

Markets absorbed the data without major shifts in terminal rate pricing.

The Day Ahead

BOJ board member Tamura speaks at 17:00 ET today on economic conditions. Retail sales year-over-year data for May arrives Sunday at 15:50 ET. No other major Japanese releases are scheduled through Friday.

Traders will parse Tamura’s tone for clues on the timing of the next rate move. Yen volatility may increase on any fresh intervention signals from officials.

Other Economic Notes

Japan confirmed yen intervention over the past month with record foreign-exchange spending to defend the currency. Authorities are refining management of the intervention war chest to improve effectiveness. The $8 trillion JGB market faces ongoing pressure from carry-trade unwinds that are spilling into U.S.

assets. Corporate earnings and external demand remain key supports for growth despite the stronger yen risks.

Global Macro News

The yen remains capped near 162 as intervention threats limit downside moves according to MUFG. A potential Fed rate hike could push USD/JPY toward 165, former BoJ officials warned. Australian CPI cooling and persistent BoJ hawkishness kept the AUD/JPY pair steady.

<i>↓ p.2</i>