Japan Macro Daily(Beta Mode)

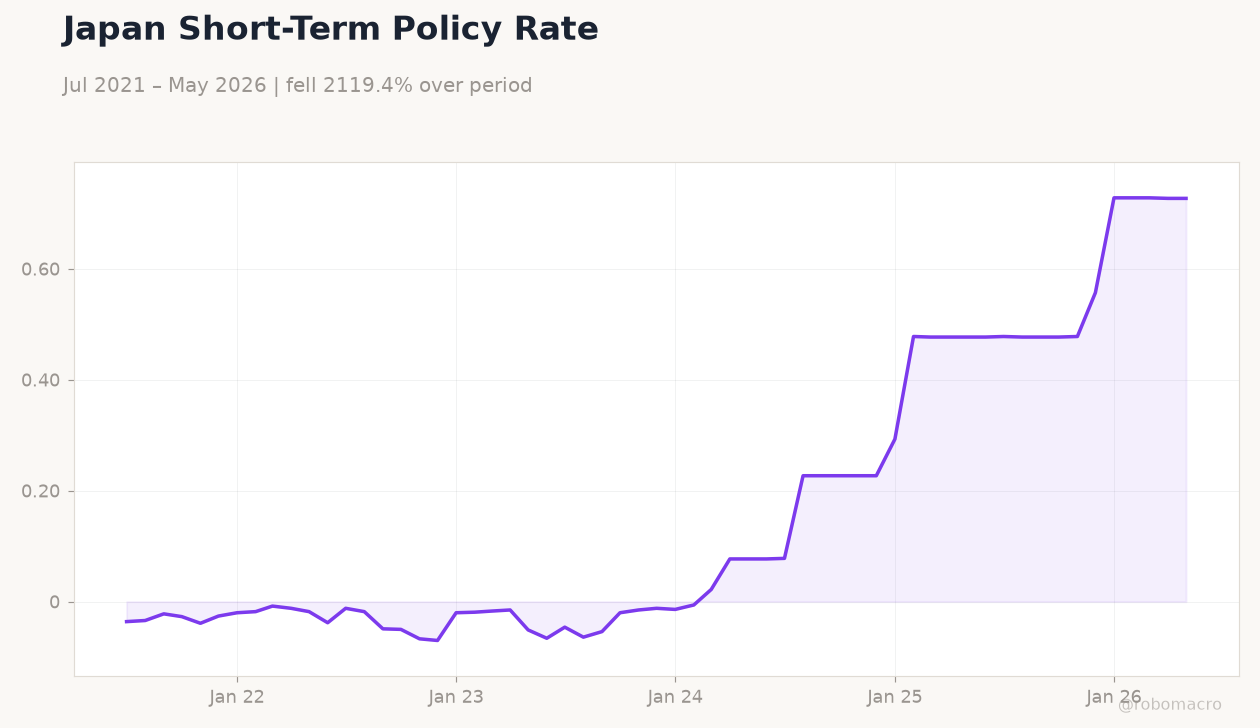

Tamura Signals 2% Neutral Rate

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 69,174.97 | -0.88% |

| USD/JPY | 161.77 | +0.01% |

| EUR/JPY | 184.06 | +0.21% |

| GBP/JPY | 213.51 | +0.26% |

| Gold | 4,040.30 | +1.25% |

| Brent Crude | 75.04 | +1.76% |

| Bitcoin | 59,388.48 | -2.63% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

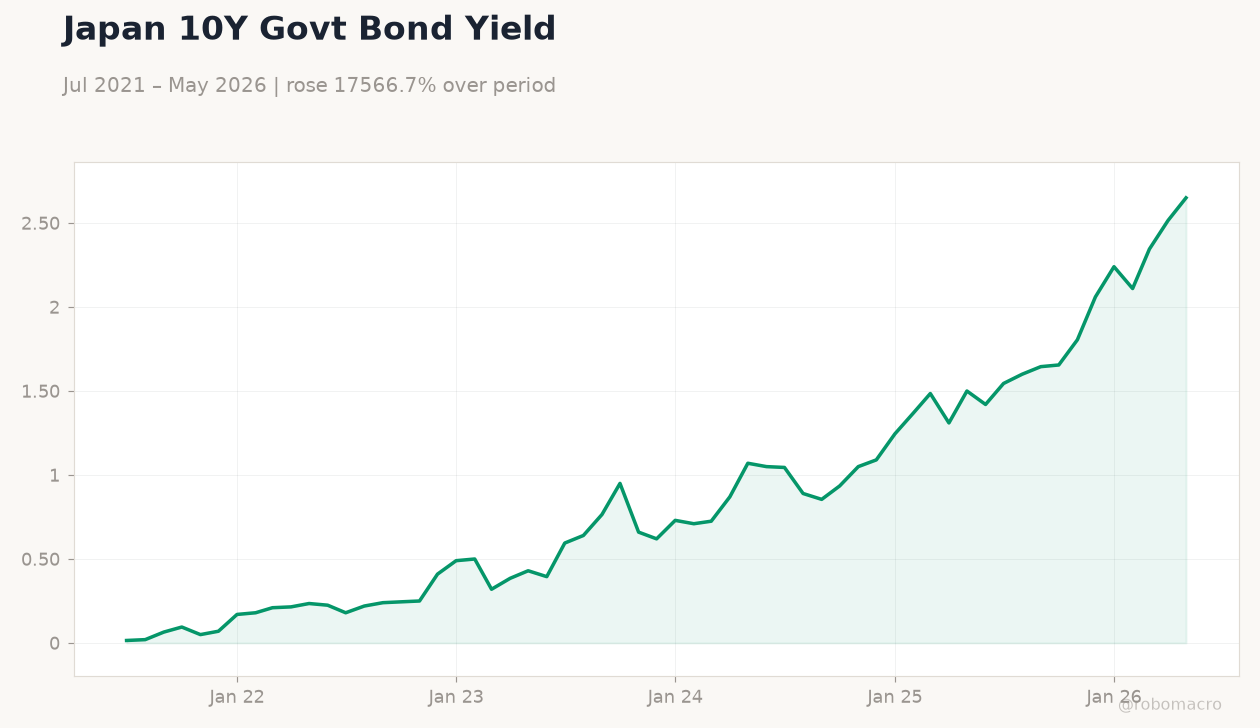

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 54.50 | 54.50 | 54.90 |

| S&P Global Services PMI Flash | 50 | - | 51.80 |

| BoJ Summary of Opinions | - | - | "" |

| BoJ Himino Speech | - | - | - |

| BOJ Gov Ueda Speech | - | - | - |

| BOJ Tamura Speech | - | - | - |

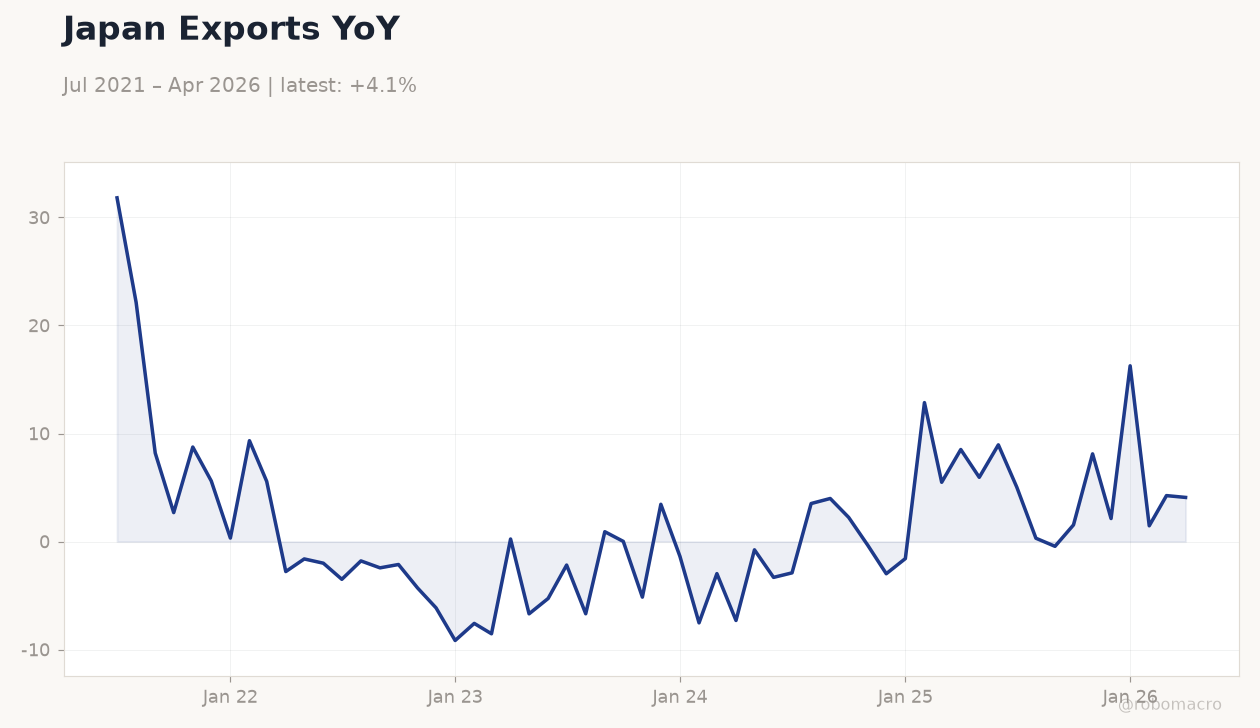

Japan Exports YoY | Type: macro_line | YoY %: 4.085 (2026-04-01) | Range: -9.156–31.82 | Trend(6pt): 31.82,-2.434,-5.144,-1.575,4.253,4.085

Japan Exports YoY | Type: macro_line | YoY %: 4.085 (2026-04-01) | Range: -9.156–31.82 | Trend(6pt): 31.82,-2.434,-5.144,-1.575,4.253,4.085

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Sunday (2026-06-28) | |||

| Retail Sales Year-over-Year | 2.10 | - | 15:50 |

- BoJ board member Tamura stated Japan’s neutral rate stands near 2%, reinforcing expectations for further policy normalisation.

- Manufacturing PMI rose to 54.9 while services PMI climbed to 51.8, showing modest expansion in June.

- Japan 10-year JGB yield rose 5.37% to 2.65% as markets priced in accelerated rate hikes.

Yesterday's Recap

Japan’s June flash PMIs beat expectations, with manufacturing at 54.9 and services at 51.8, pointing to steady private-sector momentum. The BoJ released its Summary of Opinions from the June meeting, highlighting that several members advocated continued rate increases given persistent inflation risks. Board member Himino spoke on 23 June, followed by Governor Ueda and Tamura on 24 June.

Tamura explicitly placed the neutral rate around 2%, a level well above the current 0.73% policy rate. The Nikkei 225 fell 0.88% to 69,174.97 while USD/JPY held at 161.77. The 10-year JGB yield rose sharply to 2.65%, reflecting reduced BoJ bond purchases and bank reluctance to absorb supply.

Yen crosses edged higher against the euro and sterling amid intervention warnings near 162.

The Day Ahead

No major data releases are scheduled for 25 June. Markets will monitor follow-up comments from remaining BoJ speakers and any Ministry of Finance statements on foreign-exchange intervention management. Retail sales for May are due on 28 June and will provide the next direct read on consumer demand.

Traders also await any updates on the government’s 370 trillion yen long-term economic blueprint and its implications for BoJ coordination. Yen volatility is expected to remain elevated given the proximity to the 162 intervention threshold.

Other Economic Notes

Japan’s long-term fiscal plan emphasises monetary policy support for private demand while balancing growth and price stability. Banks have shown hesitation to increase JGB holdings as the BoJ gradually steps back from large-scale purchases, raising term-premium pressure. The combination of fiscal expansion and slower BoJ balance-sheet growth points to structurally higher yields over the medium term.

CPI remains subdued at the verified -0.50% YoY reading, yet BoJ officials continue to focus on upside risks from wages and services prices.