Japan Macro Daily(Beta Mode)

Yen Weakens to 40-Year Low on Dollar Strength

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 69,360.88 | -4.15% |

| USD/JPY | 161.91 | +0.07% |

| EUR/JPY | 184.97 | +0.62% |

| GBP/JPY | 214.71 | +0.63% |

| Gold | 4,028.50 | -1.23% |

| Brent Crude | 73.56 | +2.18% |

| Bitcoin | 60,296.62 | +1.28% |

| Japan 2Y Govt Yield | 0.73% | +0.00% |

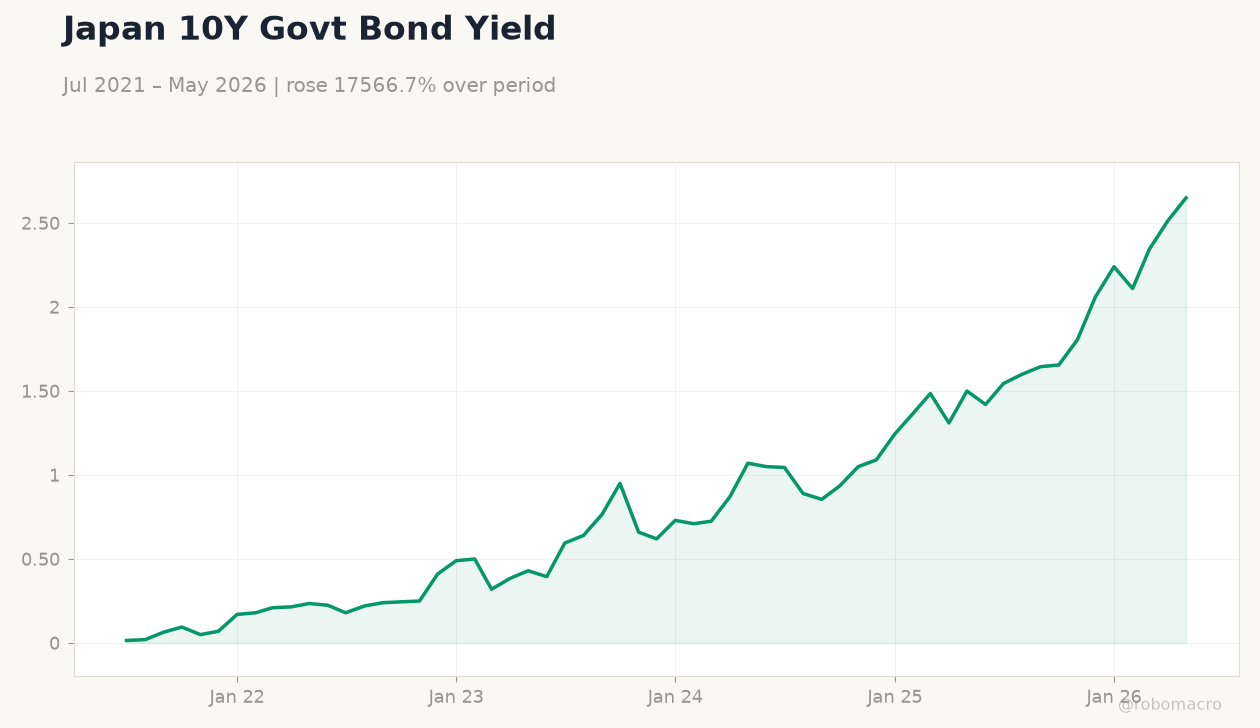

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

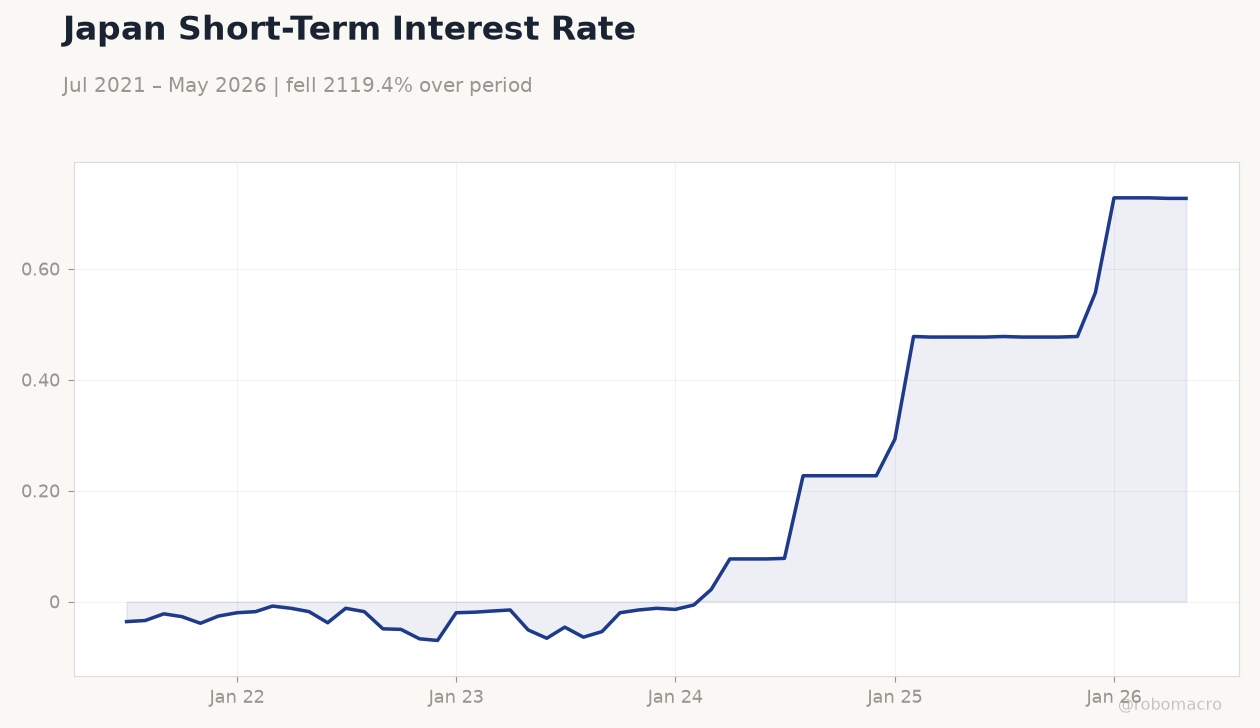

Japan Short-Term Interest Rate | Type: macro_line | Short-Term Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Japan Short-Term Interest Rate | Type: macro_line | Short-Term Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(6pt): -0.036,-0.049,-0.015,0.293,0.728,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

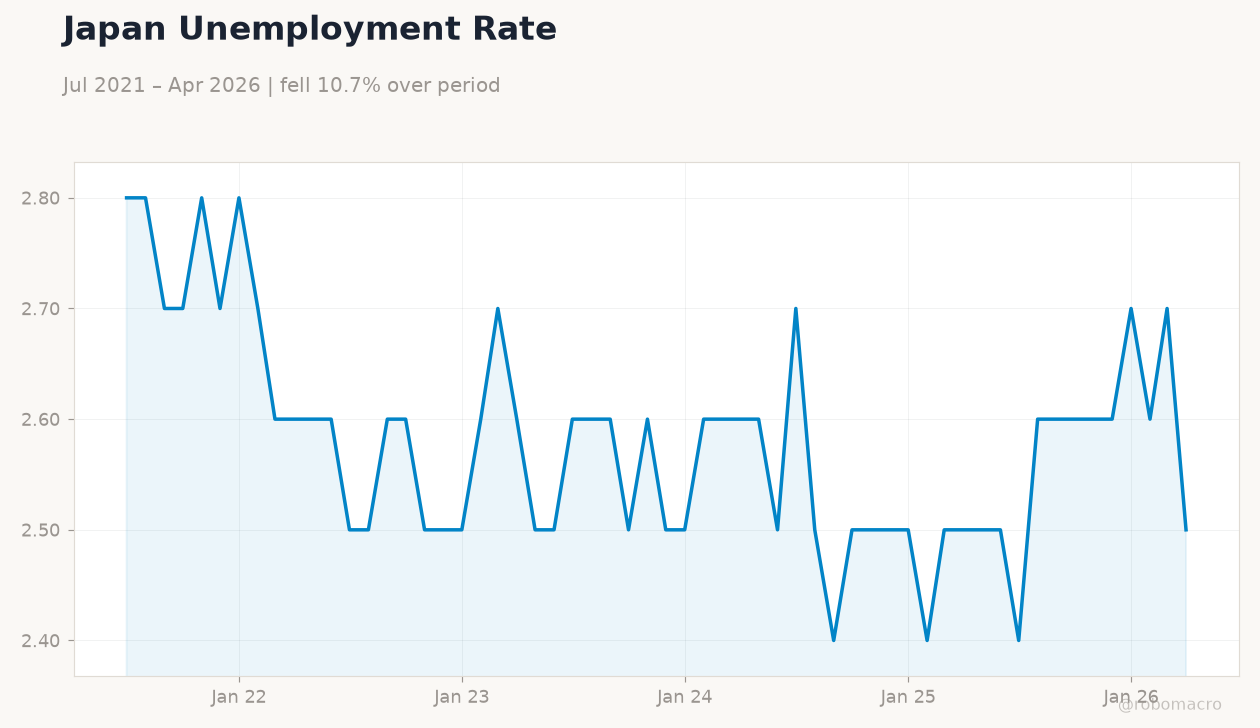

| Headline Unemployment Rate | 2.50 | 2.50 | 15:30 |

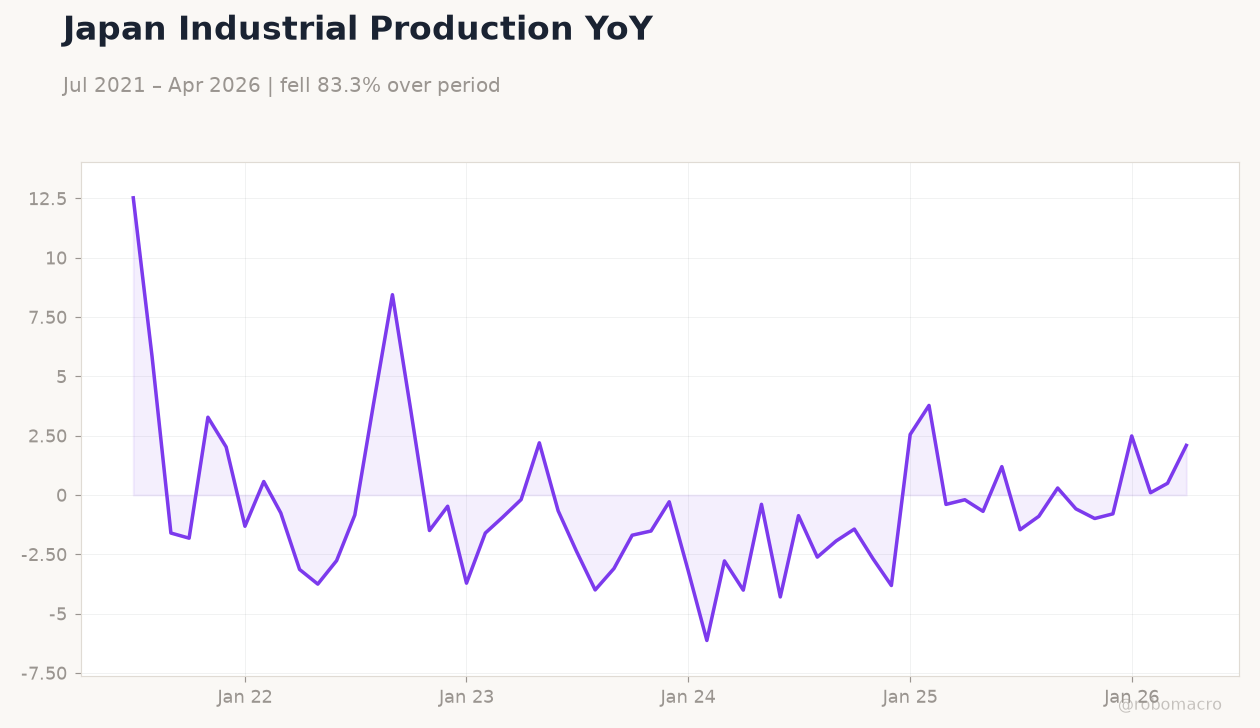

| Industrial Production Month-over-Month Preliminary | 0.50 | 1.10 | 15:50 |

| Tuesday (2026-06-30) | |||

| Housing Starts Year-over-Year | 11.40 | 31.80 | 21:00 |

| Tankan Large Manufacturers Index | 17 | 16 | 15:50 |

| Wednesday (2026-07-01) | |||

| Consumer Confidence Index | 33.60 | 34 | 21:00 |

- Yen falls to weakest level since 1986 as USD/JPY holds near 161.91 amid sustained dollar demand.

- Nikkei 225 drops 4.15% to 69,360.88 while 10-year JGB yields rise 5.37% to 2.65%.

- Markets await Tankan Large Manufacturers Index and fresh inflation signals to gauge BoJ normalisation pace.

Yesterday's Recap

Equity markets sold off sharply as the Nikkei 225 fell 4.15% to close at 69,360.88. The 10-year JGB yield climbed 5.37% to 2.65%, reflecting reduced safe-haven demand. USD/JPY edged 0.07% higher to 161.91, extending its multi-decade high.

EUR/JPY and GBP/JPY gained 0.62% and 0.63% respectively on cross flows. Brent crude rose 2.18% to $73.56 while gold declined 1.23% to $4,028.50. No major data prints occurred, leaving price action driven by overnight dollar strength and positioning ahead of week-end Tankan results.

Bitcoin added 1.28% to $60,296.62 in thin trading.

The Day Ahead

Today’s calendar features the May headline unemployment rate at 15:30 ET, expected to hold at 2.5%, alongside preliminary industrial production month-over-month at 15:50 ET, forecast to rise 1.1%. Tomorrow brings the high-impact Tankan Large Manufacturers Index at 15:50 ET, seen slipping to 16 from 17, and housing starts year-over-year data. These releases will shape views on corporate sentiment and housing momentum before the next policy meeting.

Retail sales and job-to-applicant figures due later this week add further colour on consumer demand. Markets will parse any Tankan downside for clues on whether BoJ tightening expectations need recalibration.

Other Economic Notes

Japan’s verified CPI prints remain anchored at the -0.50% year-over-year level recorded in mid-2021, underscoring the long path back to sustained target inflation. The BoJ policy rate sits at 0.73% following the May adjustment, providing limited room before further normalisation steps. Yen depreciation continues to lift import prices, reinforcing the case for gradual rate increases despite government calls for measured management.

Corporate output data from Toyota showed modest gains, supporting the view that underlying demand remains intact even as currency volatility rises.