Japan Macro Daily(Beta Mode)

Yen Weakens to 40-Year Lows Ahead of Tankan

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 71,841.06 | +3.42% |

| USD/JPY | 162.69 | +0.47% |

| EUR/JPY | 185.59 | +0.37% |

| GBP/JPY | 214.59 | +0.51% |

| Gold | 4,008.70 | -0.34% |

| Brent Crude | 73.44 | +0.40% |

| Bitcoin | 58,388.84 | -2.91% |

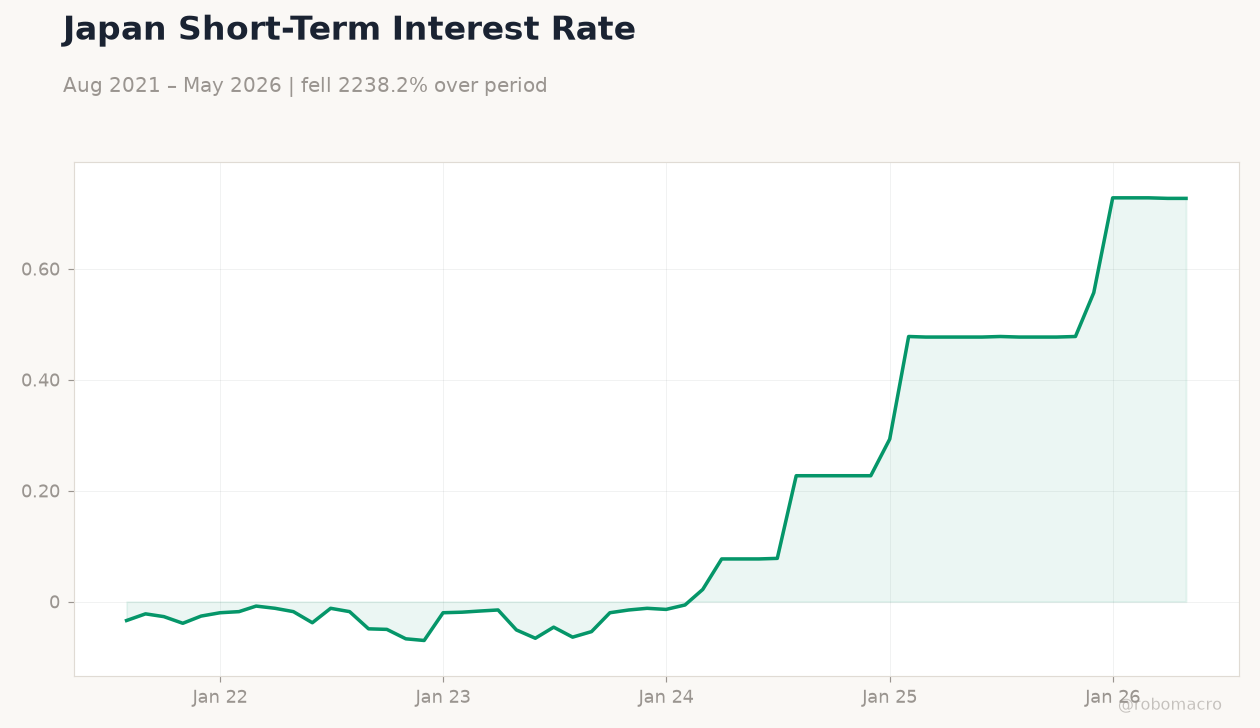

| Japan 2Y Govt Yield | 0.73% | +0.00% |

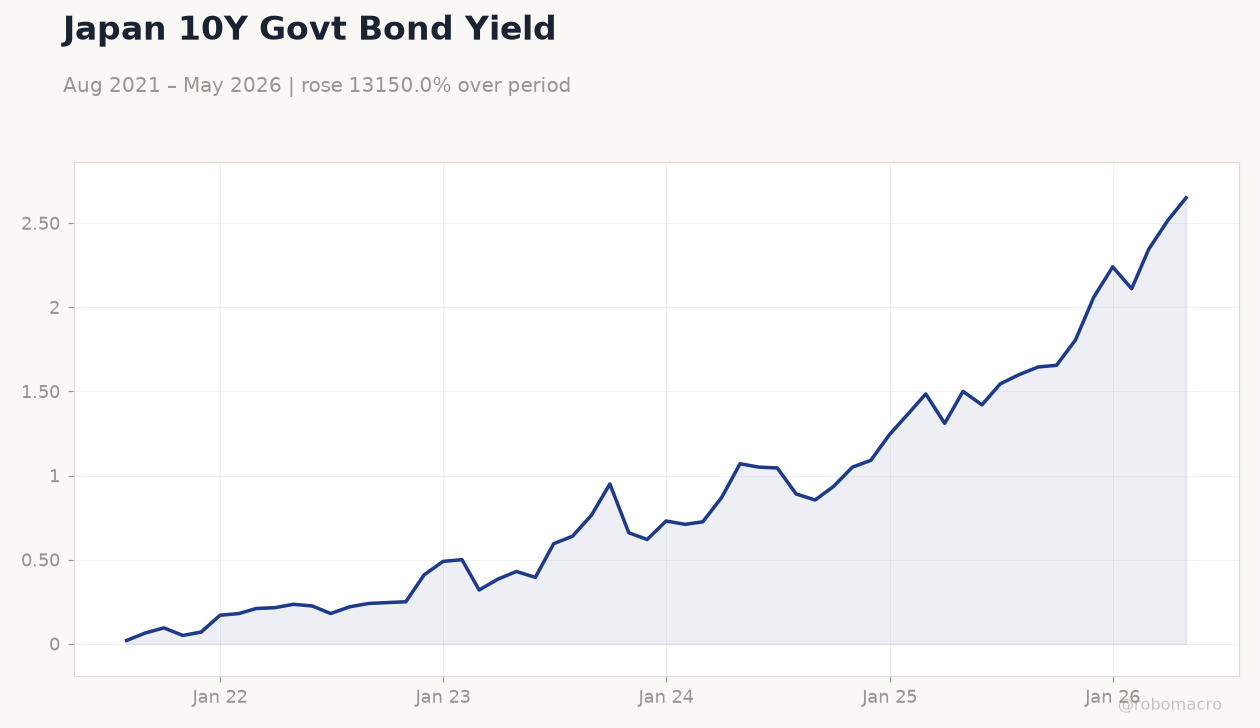

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

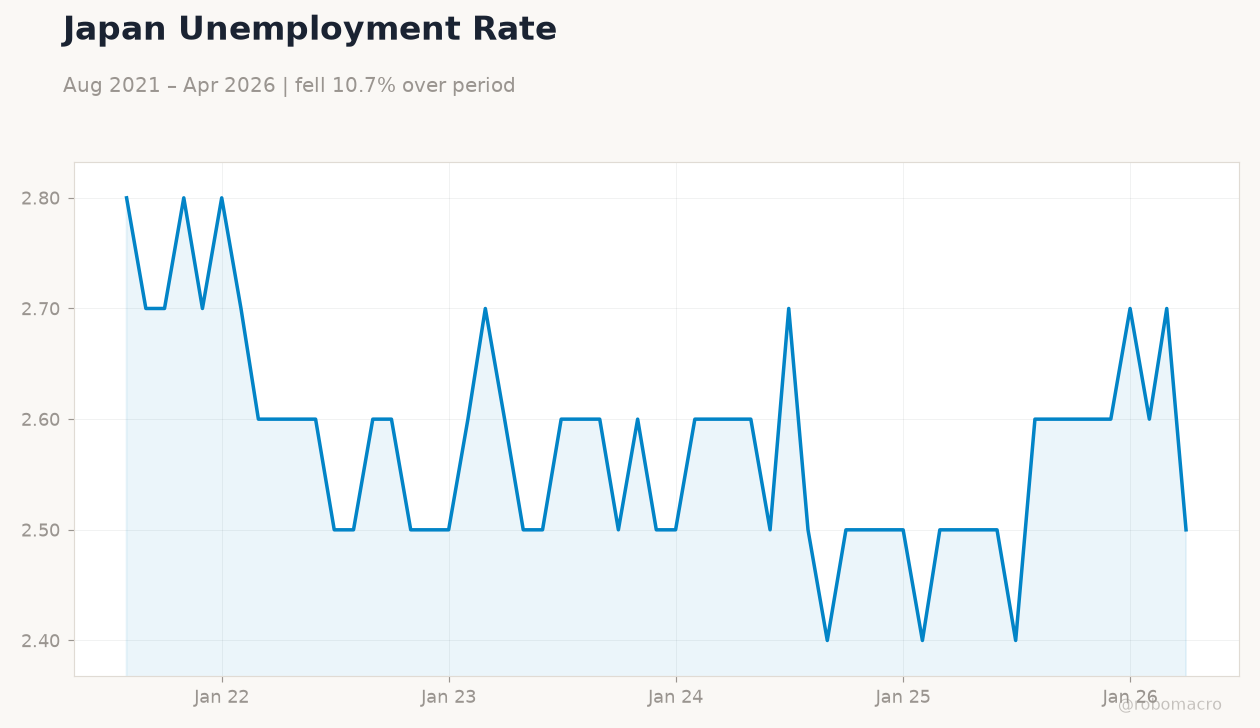

| Headline Unemployment Rate | 2.50 | 2.50 | 2.50 |

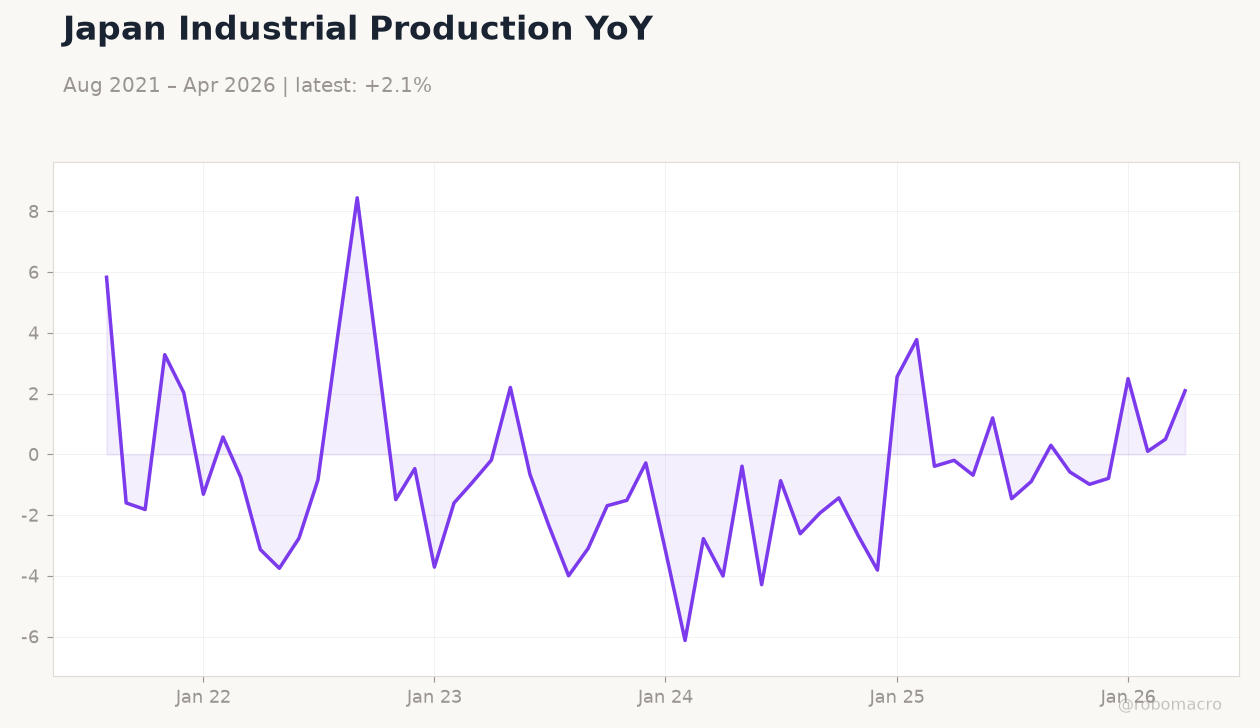

| Industrial Production Month-over-Month Preliminary | 0.50 | 1.10 | 0.50 |

| Housing Starts Year-over-Year | 11.40 | 31.80 | 33.90 |

Japan 10Y Govt Bond Yield | Type: macro_line | 10Y Yield %: 2.65 (2026-05-01) | Range: 0.02–2.65 | Trend(6pt): 0.02,0.245,0.62,1.37,2.515,2.65

Japan 10Y Govt Bond Yield | Type: macro_line | 10Y Yield %: 2.65 (2026-05-01) | Range: 0.02–2.65 | Trend(6pt): 0.02,0.245,0.62,1.37,2.515,2.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tankan Large Manufacturers Index | 17 | 16 | 15:50 |

| Wednesday (2026-07-01) | |||

| Consumer Confidence Index | 33.60 | 34 | 21:00 |

- Unemployment holds at 2.5% while industrial production misses forecasts.

- Nikkei surges 3.42% as yen weakens to 162.69 versus dollar.

- Markets price in limited BoJ tightening amid dovish signals.

Yesterday's Recap

Japan's headline unemployment rate remained unchanged at 2.5% in line with consensus. Industrial production rose just 0.5% month-over-month, missing the 1.1% expected and pointing to softer factory momentum. Housing starts beat forecasts sharply, climbing 33.9% year-over-year.

The Nikkei 225 rallied 3.42% to close at 71,841.06 while USD/JPY advanced 0.47% to 162.69. The 10-year JGB yield jumped 5.37% to 2.65% as the yen extended losses. EUR/JPY and GBP/JPY also gained ground on broad dollar strength.

Mixed data releases failed to alter the market's view of gradual BoJ normalisation.

The Day Ahead

The Tankan Large Manufacturers Index is due at 15:50 ET with consensus at 16, one point below the prior reading. Consumer Confidence is expected to rise to 34 from 33.6 later in the session. Both releases will feed directly into the BoJ's assessment of domestic demand and corporate plans.

No policy speakers are scheduled. Markets will focus on whether the Tankan confirms the recent improvement in business sentiment despite yen-driven cost pressures.

Other Economic Notes

Japan's economy continues to expand yet the yen trades at 40-year lows against the dollar, highlighting persistent policy divergence. The weak currency is reshaping export competitiveness and inbound investment flows. Plans for direct yen-rupee settlement with India aim to reduce reliance on the US dollar in bilateral trade.

Import costs remain elevated, keeping inflation risks tilted higher even as headline CPI prints stay subdued. Policymakers face a narrow path between supporting growth and managing currency volatility.

Global Macro News

US-Japan rate differentials continue to support the dollar and pressure the yen lower. Bitcoin fell 2.91% while gold slipped 0.34% on reduced haven demand. Brent crude rose 0.40% amid steady supply signals.

Broader equity gains reflected improved risk appetite after softer US data. The yen's historic weakness is prompting renewed discussion of possible intervention by Japanese authorities. <i>↓ p.2</i>